Managed Mobility Services (MMS) Market Size, Share, and Trends Analysis Report

CAGR :

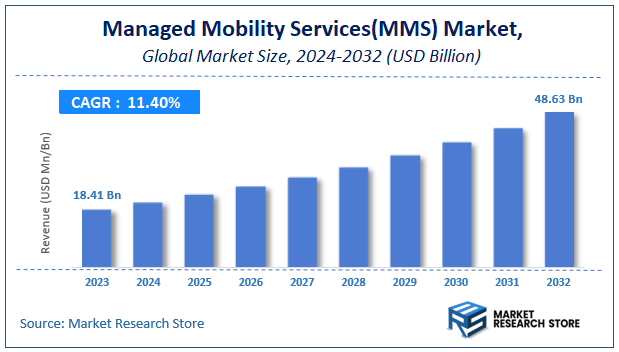

| Market Size 2023 (Base Year) | USD 18.41 Billion |

| Market Size 2032 (Forecast Year) | USD 48.63 Billion |

| CAGR | 11.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Managed Mobility Services(MMS) Market Insights

According to Market Research Store, the global managed mobility services (MMS) market size was valued at around USD 18.41 billion in 2023 and is estimated to reach USD 48.63 billion by 2032, to register a CAGR of approximately 11.4% in terms of revenue during the forecast period 2024-2032.

The managed mobility services (MMS) report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Managed Mobility Services (MMS) Market: Overview

Managed Mobility Services (MMS) refers to the comprehensive outsourcing of an enterprise's mobile device lifecycle, including procurement, deployment, management, security, and support. MMS providers help organizations streamline mobile operations, ensuring seamless connectivity, compliance, and cost efficiency. These services cover mobile device management (MDM), expense management, security solutions, app management, and end-user support, enabling businesses to enhance productivity while mitigating risks associated with mobility. As enterprises increasingly rely on mobile devices for workforce operations, MMS plays a crucial role in optimizing and securing mobile ecosystems.

Key Highlights

- The managed mobility services (MMS) market is anticipated to grow at a CAGR of 11.4% during the forecast period.

- The global managed mobility services (MMS) market was estimated to be worth approximately USD 18.41 billion in 2023 and is projected to reach a value of USD 48.63 billion by 2032.

- The growth of the managed mobility services (MMS) market is being driven by the increasing adoption of mobile devices and the rising need for secure enterprise mobility solutions.

- Based on the function, the mobile device management segment is growing at a high rate and is projected to dominate the market.

- Based on the deployment, the cloud deployment segment is expected to dominate the market.

- On the basis of end-user, the IT and telecom segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Managed Mobility Services (MMS) Market: Dynamics

Key Growth Drivers:

- Rise of Remote Work & BYOD: The surge in remote work and the adoption of Bring Your Own Device (BYOD) policies have increased the complexity of managing mobile devices and their security. MMS providers offer solutions to streamline these processes.

- Enhanced Security Needs: Cyber threats are constantly evolving, and mobile devices are increasingly targeted. MMS solutions provide robust security measures like data encryption, mobile threat defense, and remote wipe capabilities.

- Improved Employee Productivity & Collaboration: MMS can optimize device performance, ensure seamless access to company resources, and facilitate collaboration among employees, leading to increased productivity.

- Cost Optimization: By outsourcing device management, companies can reduce IT overhead costs, streamline procurement, and optimize device lifecycles.

Restraints:

- Data Security Concerns: Concerns about data breaches and the potential for sensitive corporate data leakage can hinder the adoption of BYOD and cloud-based solutions.

- Integration Challenges: Integrating MMS solutions with existing IT infrastructure and business processes can be complex and time-consuming.

- Cost of Implementation: Implementing and maintaining an MMS solution can involve significant upfront and ongoing costs, which may be a barrier for some organizations.

- Vendor Lock-in: Choosing a specific MMS provider can create vendor lock-in, making it difficult to switch to alternative solutions in the future.

Opportunities:

- Integration with AI & ML: Leveraging AI and machine learning for predictive analytics, threat detection, and automated device provisioning can enhance the effectiveness and efficiency of MMS solutions.

- 5G & IoT Integration: Integrating MMS with 5G networks and the Internet of Things (IoT) can unlock new possibilities for mobile device management and create new service offerings.

- Expansion into Emerging Markets: The growing adoption of mobile devices and the increasing digitalization of businesses in emerging markets present significant growth opportunities for MMS providers.

- Focus on Sustainability: Offering sustainable solutions, such as device lifecycle management programs, can enhance the environmental credentials of MMS providers and attract eco-conscious customers.

Challenges:

- Keeping Pace with Rapid Technological Change: The rapid evolution of mobile technologies, operating systems, and cyber threats requires MMS providers to constantly adapt and innovate their solutions.

- Maintaining Competitive Advantage: The MMS market is competitive, with numerous players vying for market share. Differentiating services and maintaining a competitive edge is crucial.

- Data Privacy and Compliance: Ensuring compliance with data privacy regulations (e.g., GDPR) and maintaining the confidentiality and security of customer data are critical challenges.

- Skilled Workforce: Attracting and retaining skilled professionals with expertise in mobile device management, cybersecurity, and cloud technologies is essential for the success of MMS providers.

Managed Mobility Services(MMS) Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Managed Mobility Services(MMS) Market |

| Market Size in 2023 | USD 18.41 Billion |

| Market Forecast in 2032 | USD 48.63 Billion |

| Growth Rate | CAGR of 11.4% |

| Number of Pages | 140 |

| Key Companies Covered | Deutsche Telekom AG (Germany) Maxis Bhd (Malaysia), IBM Corp. (U.S.), Vodafone Group PLC (U.K.), Singtel (Singapore), StarHub (Singapore), Wipro (India), Telefónica S.A. (Spain), PLDT (Philippines), Orange S.A (France), Fujitsu Ltd, AT&T Inc. (U.S.), Hewlett Packard Enterprise Co. (U.S.), Celcom Axiata (Malaysia), and Accenture (U.S.) |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Managed Mobility Services (MMS) Market: Segmentation Insights

The global managed mobility services (MMS) market is divided by function, deployment, end-user, and region.

Segmentation Insights by Function

Based on function, the global managed mobility services (MMS) market is divided into mobile device management, mobile application management, and mobile security.

In the Managed Mobility Services (MMS) market, Mobile Device Management (MDM) is the most dominant segment. MDM solutions provide comprehensive management of mobile devices, enabling organizations to control and monitor the use of devices across a workforce. It includes functions like device configuration, data security, app management, and remote troubleshooting, making it a fundamental solution for businesses looking to secure and optimize mobile devices. MDM's ability to enforce policies such as data encryption, password settings, and remote wipe capabilities makes it essential for organizations to protect sensitive information, which has driven its dominance in the MMS market.

The second most dominant segment is Mobile Security. As organizations increasingly rely on mobile devices for business operations, ensuring data security becomes crucial. Mobile Security encompasses a wide range of services, including threat detection, malware prevention, and secure network access. With rising concerns over cyber threats targeting mobile devices, businesses are investing heavily in mobile security solutions to safeguard sensitive data and maintain compliance with privacy regulations. This growing demand for security, combined with the rise of mobile-based attacks, positions mobile security as a key area of focus within MMS.

Finally, Mobile Application Management (MAM) holds the third position in terms of dominance within the MMS market. MAM refers to the management and securing of applications used on mobile devices, ensuring that only authorized apps are installed and that apps comply with security policies. MAM is particularly crucial in Bring Your Own Device (BYOD) environments, where employees use personal devices for work-related tasks. While important, it is often considered a supplementary service to MDM and Mobile Security, as MDM addresses broader device management needs and mobile security ensures the safety of the device and its data.

Segmentation Insights by Deployment

On the basis of deployment, the global managed mobility services (MMS) market is bifurcated into cloud and on-premise.

In the Managed Mobility Services (MMS) market, Cloud deployment is the most dominant segment. The cloud-based approach offers several advantages, including scalability, cost-effectiveness, and ease of remote management. With cloud deployment, organizations can leverage a centralized platform to manage mobile devices, applications, and security policies across various locations without the need for extensive on-site infrastructure. Cloud solutions also allow for faster updates and improvements, which is essential as mobile technology evolves. The flexibility of cloud deployment, combined with its ability to reduce overhead costs associated with maintaining on-premise hardware, has made it the preferred choice for many organizations.

On-premise deployment, while less dominant, remains an important segment for businesses that have strict data privacy and regulatory compliance requirements. Some organizations prefer on-premise solutions to maintain full control over their infrastructure and data, especially when handling sensitive information or operating in industries with stringent security standards. On-premise deployments can offer more customization and integration with existing IT systems, but they often come with higher upfront costs, maintenance requirements, and limitations in scalability compared to cloud-based solutions. Despite these challenges, on-premise deployment continues to serve industries where data security and compliance are critical, such as government or healthcare sectors.

Segmentation Insights by End-user

On the basis of end-user, the global managed mobility services (MMS) market is bifurcated into IT and telecom, BFSI, healthcare, manufacturing, retail, and education.

In the Managed Mobility Services (MMS) market, the IT and Telecom sector is the most dominant end-user. This industry is at the forefront of adopting mobile technologies and managing mobile devices, applications, and security. IT and Telecom companies often have large workforces, and effective mobility management is essential for optimizing productivity, ensuring security, and supporting remote work environments. These organizations need scalable solutions to manage mobile devices and integrate them with various enterprise systems, making MMS a critical part of their operations.

Following IT and Telecom, BFSI (Banking, Financial Services, and Insurance) is another significant end-user segment. The BFSI sector is heavily reliant on mobile technologies for operations such as customer interactions, online transactions, and mobile banking apps. Security and compliance are top priorities in this sector, driving the demand for robust MMS solutions to ensure data protection, regulatory adherence, and secure mobile access to sensitive financial information. The increasing reliance on mobile apps and devices in banking services further fuels the growth of MMS in this sector.

The Healthcare sector also plays a crucial role in driving demand for MMS, particularly with the increased use of mobile devices for patient management, telemedicine, and healthcare applications. Healthcare organizations require solutions to ensure the security of patient data while supporting mobile access to medical records, diagnostic tools, and communication systems. Compliance with regulations like HIPAA (Health Insurance Portability and Accountability Act) makes mobile security and device management in healthcare settings a critical necessity, contributing to MMS's growing adoption in the industry.

Manufacturing is another important sector where MMS is gaining traction, driven by the adoption of mobile technologies for inventory management, supply chain tracking, and real-time communication. Mobile devices are increasingly used to improve operational efficiency and productivity on the factory floor. As manufacturers embrace Industry 4.0 technologies, mobility management becomes crucial for ensuring seamless connectivity and protecting industrial data. However, compared to IT and Telecom or BFSI, the manufacturing sector's use of MMS is still growing as the industry continues to embrace digital transformation.

Retail is also a key end-user, especially as more retailers adopt mobile point-of-sale (POS) systems, e-commerce platforms, and mobile applications for customer engagement. Retailers are turning to MMS solutions to secure mobile transactions, manage inventory, and enhance customer experiences. With the increasing use of mobile devices for both employees and customers, the need for effective mobility management has risen. While retail adoption is robust, it tends to be more concentrated in specific areas like payment security and customer-facing mobile solutions.

Lastly, the Education sector is an emerging end-user for MMS, as schools and universities increasingly use mobile devices for learning, administration, and communication. With the rise of e-learning platforms and mobile-based educational tools, educational institutions need to secure and manage devices, apps, and data access for both students and faculty. While still less prominent than sectors like IT and Telecom or BFSI, the growing trend of digital learning and remote education is driving an increased demand for MMS solutions in education.

Managed Mobility Services (MMS) Market: Regional Insights

- North America is expected to dominates the global market

North America stands as the leading region in the managed mobility services market, driven by substantial demand from large enterprises across sectors such as banking, retail, healthcare, and manufacturing. The presence of numerous pioneers in advanced digital solutions, particularly in the United States, has significantly boosted the adoption of managed mobility services to securely manage and support an increasingly mobile workforce. High smartphone penetration and robust internet infrastructure further establish North America as a mature market, with major vendors operating scalable delivery centers to effectively meet regional demand.

Asia Pacific has emerged as the fastest-growing market for managed mobility services, propelled by rapid digital transformation initiatives aimed at enhancing productivity amid expanding regional economies. Countries like China and India present compelling opportunities due to burgeoning industries, rapid urbanization, and increased investment in advanced technologies. The availability of skilled talent and competitive pricing from local vendors have made the region an attractive outsourcing hub, encouraging further expansion of managed services providers to capitalize on this growth.

Europe represents a significant market for managed mobility services, with countries such as Germany, the United Kingdom, and France leading in mobile technology adoption. Organizations in this region are increasingly investing in secure and efficient mobile solutions to support their workforce and drive productivity. Managed mobility services providers offer a wide range of services, including mobile device management, security solutions, and application management, catering to the diverse needs of European enterprises.

The Middle East and Africa region are experiencing rapid growth in the managed mobility services market, driven by increasing digitalization and mobile adoption in countries like the UAE, Saudi Arabia, and South Africa. Organizations are seeking managed mobility services to enhance their mobile operations, improve security, and streamline applications. The region offers significant growth opportunities for providers focusing on delivering innovative and reliable solutions to meet the diverse needs of businesses.

Latin America is also emerging as a key market for managed mobility services, with countries like Brazil and Argentina undergoing significant digital transformation. Organizations in this region are adopting managed mobility services to streamline mobile operations, address security concerns, and manage mobile devices efficiently. As more companies recognize the importance of effective mobile solutions, the demand for managed mobility services in Latin America is poised for significant growth.

Recent Developments:

-

In February 2023, Telefónica SA (Spain) and Skydweller Aero Inc. (US) partnered to develop solar-powered aircraft for expanding cellular coverage and affordable broadband in underserved regions. The collaboration aims to improve connectivity in remote areas, benefiting both defense and commercial sectors through innovative technology.

- In July 2021, Wipro Limited and Celonis partnered to offer process mining services under Wipro’s Managed Services Solutions (MMS). The collaboration focuses on improving mobile device usage analytics to identify optimization and cost-saving opportunities, helping clients achieve operational efficiencies in mobile device management.

- In February 2021, Verizon Communications Inc. and Deloitte partnered to combine Deloitte’s consulting expertise with Verizon’s Managed Mobility Services (MMS). The collaboration aims to address specific business needs, offering integrated consulting and mobility solutions to help clients achieve their goals and expand their operations.

Managed Mobility Services (MMS) Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the managed mobility services (MMS) market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global managed mobility services (MMS) market include:

- Airwatch

- Digital Management

- HP Development

- Deutsche Telekom AG

- StarHub

- Wipro Ltd.

- Telefónica S.A.

- PLDT

- Orange S.A

- Fujitsu Ltd

- AT&T Inc.

- Maxis Bhd

- IBM Corporation

- Vodafone Group PLC

- Singtel

- Hewlett Packard Enterprise Co.

- Celcom Axiata

- Accenture Plc

The global managed mobility services (MMS) market is segmented as follows:

By Function

- Mobile Device Management

- Mobile Application Management

- Mobile Security

- Other

By Deployment

- Cloud

- On-premise

By End-user

- IT and Telecom

- BFSI

- Healthcare

- Manufacturing

- Retail

- Education

- Other

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global managed mobility services (MMS) market size was projected at approximately US$ 18.41 billion in 2023. Projections indicate that the market is expected to reach around US$ 48.63 billion in revenue by 2032.

The global managed mobility services (MMS) market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 11.4% during the forecast period from 2024 to 2032.

North America is expected to dominate the global managed mobility services (MMS) market.

The key factors driving the global Managed Mobility Services (MMS) market include the growing demand for cost-efficient mobile device management, increased adoption of BYOD (Bring Your Own Device) policies, and the need for enhanced security and operational efficiency in managing mobile devices and applications.

Who are the leading players functioning in the global managed mobility services (MMS) market growth?

Some of the prominent players operating in the global managed mobility services (MMS) market are; Airwatch, Digital Management, HP Development, Deutsche Telekom AG, StarHub, Wipro Ltd., Telefónica S.A., PLDT, Orange S.A, Fujitsu Ltd, AT&T Inc., Maxis Bhd, IBM Corporation, Vodafone Group PLC, Singtel, Hewlett Packard Enterprise Co., Celcom Axiata, Accenture Plc, and others.

Table Of Content

Inquiry For Buying

Managed Mobility Services (MMS)

Request Sample

Managed Mobility Services (MMS)