Overprint Varnish Market Size, Share, and Trends Analysis Report

CAGR :

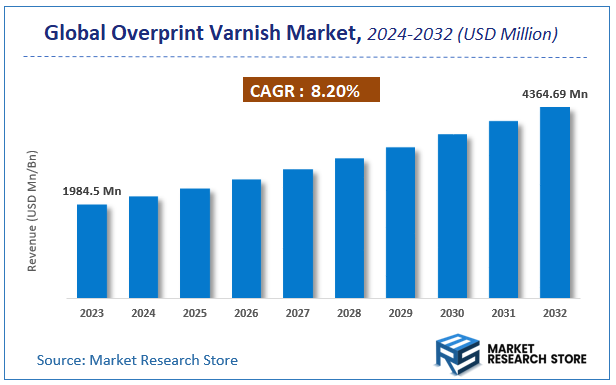

| Market Size 2023 (Base Year) | USD 1984.5 Million |

| Market Size 2032 (Forecast Year) | USD 4364.69 Million |

| CAGR | 8.2% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Overprint Varnish Market Insights

According to Market Research Store, the global overprint varnish market size was valued at around USD 1984.5 million in 2023 and is estimated to reach USD 4364.69 million by 2032, to register a CAGR of approximately 8.2% in terms of revenue during the forecast period 2024-2032.

The overprint varnish report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032

To Get more Insights, Request a Free Sample

Global Overprint Varnish Market: Overview

The Overprint Varnish market is experiencing steady growth, driven by increasing demand for high-quality packaging, printed materials, and label applications across industries such as food and beverage, pharmaceuticals, cosmetics, and consumer goods. Overprint varnishes are protective coatings applied to printed surfaces to enhance visual appeal, improve durability, and provide resistance against moisture, chemicals, and abrasion. These varnishes are available in different formulations, including water-based, solvent-based, and UV-curable types, catering to diverse printing requirements.

Market expansion is fueled by the rising adoption of premium packaging solutions and branding strategies that emphasize glossy, matte, and textured finishes to enhance product presentation. Additionally, increasing environmental concerns have led to a growing preference for eco-friendly, low-VOC (volatile organic compound) overprint varnishes, particularly in food packaging and pharmaceutical applications where regulatory compliance is essential. The shift toward digital printing and high-speed printing technologies is also contributing to market growth, as overprint varnishes play a crucial role in ensuring ink adhesion and print longevity.

Key Highlights

- The overprint varnish market is anticipated to grow at a CAGR of 8.2% during the forecast period.

- The global overprint varnish market was estimated to be worth approximately USD 1984.5 million in 2023 and is projected to reach a value of USD 4364.69 million by 2032.

- The growth of the overprint varnish market is being driven by the increasing demand for enhanced packaging aesthetics and improved product protection.

- Based on the material, the synthetic segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the food packaging segment is projected to swipe the largest market share.

- In terms of end use, the food & beverage segment is expected to dominate the market.

- Based on the functionality, the gloss segment is expected to dominate the market.

- Based on the technology, the flexographic printing segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Overprint Varnish Market: Dynamics

The overprint varnish market is a segment of the printing and packaging industry. Here's a breakdown of its dynamics:

Key Drivers

- Enhanced Print Aesthetics: Overprint varnishes enhance the visual appeal of printed materials by adding gloss, matte, or satin finishes. This is a key driver, as brand owners seek to make their packaging and marketing materials stand out.

- Protection of Print: Overprint varnishes protect printed surfaces from scuffing, scratching, abrasion, and fading, extending the lifespan and durability of printed products. This is crucial for packaging, labels, and other printed materials that experience handling.

- Improved Print Quality: Varnishes can improve the rub resistance of printed inks, preventing smudging and improving overall print quality, especially important for high-quality print projects.

- Special Effects and Textures: Specialized varnishes can create unique effects, such as soft-touch, textured, or glitter finishes, adding value and differentiation to printed products. This is a growing segment as brands look for unique packaging.

- Food and Pharmaceutical Packaging: Overprint varnishes used in food and pharmaceutical packaging comply with regulations and provide a protective layer, preventing ink migration and ensuring product safety.

Restraints

- Cost Factor: Applying overprint varnish adds to the overall cost of printing, which can be a concern for price-sensitive applications.

- Complexity of Application: Applying varnishes requires specialized equipment and expertise, which can add complexity to the printing process.

- Environmental Concerns: Some varnishes contain volatile organic compounds (VOCs), raising environmental concerns. This is driving a shift toward more environmentally friendly options.

- Compatibility Issues: Choosing the right varnish for specific inks and substrates is crucial. Incompatibility can lead to problems like ink bleeding or poor adhesion.

Opportunities

- Development of Sustainable Varnishes: Research and development of eco-friendly varnishes with low VOCs, bio-based materials, and recyclability are creating opportunities for growth. This is a significant trend.

- Innovation in Special Effects: Developing new and innovative varnish technologies to create unique tactile and visual effects can add value and differentiation.

- Digital Printing and Varnishing: The growth of digital printing and the development of digital varnishing technologies offer new possibilities for customized and on-demand varnishing.

- Expanding Applications: Exploring new applications for overprint varnishes, such as in flexible packaging, labels, and industrial printing, can drive market growth.

Challenges

- Meeting Stringent Regulatory Requirements: Complying with evolving environmental regulations related to VOC emissions and food contact materials is a key challenge.

- Balancing Performance and Sustainability: Balancing the performance requirements of overprint varnishes with the growing need for sustainable solutions is a challenge.

- Staying Competitive: Remaining competitive in a dynamic market with increasing competition from other surface finishing technologies.

- Educating the Market: Educating printers and brand owners about the benefits and different types of overprint varnishes is essential for market growth.

Overprint Varnish Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Overprint Varnish Market |

| Market Size in 2023 | USD 1984.5 Million |

| Market Forecast in 2032 | USD 4364.69 Million |

| Growth Rate | CAGR of 8.2% |

| Number of Pages | 140 |

| Key Companies Covered | Van Son Ink Corporation, Altana, Zeller+Gmelin Group, Michelma, Toyo Ink, CHT/BEZEMA, Huber Group, Eston Chimica, Anwin Technology Co., Ltd, American Offset Printing Ink, As Inc. Co. Ltd., BRANCHER, Superior Printing Inks, JPT Corporation, Imperial Ink Private Limited |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Overprint Varnish Market: Segmentation Insights

The global overprint varnish market is divided by material, application, end use, functionality, technology, and region.

Segmentation Insights by Material

Based on material, the global overprint varnish market is divided into synthetic, water based, UV coated, and solvent based.

The Synthetic segment dominates the Overprint Varnish Market due to its widespread use in high-quality printing applications, offering enhanced gloss, durability, and resistance to moisture and chemicals. Synthetic varnishes are preferred in industries such as packaging, publishing, and commercial printing, where superior finish and long-lasting protection are required. Their versatility and compatibility with various substrates further contribute to their dominance in the market.

The Water-Based segment is gaining traction due to increasing environmental concerns and regulatory restrictions on solvent-based coatings. These varnishes are preferred for their low VOC emissions, making them a sustainable choice for eco-friendly packaging and labeling applications. Water-based varnishes provide good protection and print clarity while being safer for both manufacturers and end-users, contributing to their growing adoption.

The UV-Coated segment is experiencing significant growth due to its excellent abrasion resistance, fast curing time, and superior gloss finish. UV varnishes are widely used in high-end packaging, labels, and promotional materials that require a premium appearance and long-lasting protection. The demand for UV coatings is rising, particularly in sectors like luxury packaging and magazine printing, where aesthetic appeal is a key factor.

The Solvent-Based segment remains relevant in industrial and commercial applications where high durability and chemical resistance are required. These varnishes provide excellent adhesion and protection against moisture, heat, and mechanical wear. However, stringent environmental regulations and the shift toward greener alternatives are gradually limiting their growth in favor of water-based and UV-coated options.

Segmentation Insights by Application

On the basis of application, the global overprint varnish market is bifurcated into food packaging, non-food packaging, labeling solutions, and folding cartons.

The Food Packaging segment dominates the Overprint Varnish Market due to the growing demand for protective coatings that ensure product safety, enhance shelf appeal, and comply with food safety regulations. Overprint varnishes in this segment provide barrier properties against moisture, grease, and contamination while maintaining print clarity and durability. The rise in packaged and processed food consumption is driving the demand for food-safe varnishes, particularly water-based and UV-coated variants that meet stringent regulatory standards.

The Non-Food Packaging segment holds a significant share of the market, catering to industries such as cosmetics, pharmaceuticals, electronics, and personal care. Overprint varnishes in this segment enhance packaging aesthetics, provide scuff resistance, and protect printed materials from wear and tear. High-end packaging solutions, particularly in luxury goods and personal care products, are increasingly utilizing UV-coated varnishes for their premium glossy finish and durability.

The Labeling Solutions segment is experiencing rapid growth due to the expanding demand for high-quality labels in industries such as beverages, pharmaceuticals, and retail. Overprint varnishes enhance the durability and visual appeal of labels while providing protection against smudging, fading, and environmental exposure. UV-coated and synthetic varnishes are widely used in this segment to achieve a glossy, high-definition finish that improves brand visibility and consumer appeal.

The Folding Cartons segment is gaining traction as the demand for sustainable and visually appealing packaging solutions increases. Overprint varnishes in this segment offer added strength, gloss, and protection to printed carton surfaces, ensuring resistance to handling and storage conditions. Water-based and solvent-based varnishes are commonly used in this segment to balance performance and cost-effectiveness while maintaining eco-friendly packaging standards.

Segmentation Insights by End Use Industry

On the basis of end use industry, the global overprint varnish market is bifurcated into food & beverage, pharmaceuticals, personal care & cosmetics, and consumer goods.

The Food & Beverage segment dominates the Overprint Varnish Market, driven by the increasing demand for high-quality, protective, and visually appealing packaging. Overprint varnishes enhance the durability of printed food packaging by providing resistance to moisture, grease, and handling wear. Water-based and UV-coated varnishes are particularly popular in this segment due to their compliance with food safety regulations and their ability to maintain print integrity while ensuring consumer safety. The growing consumption of packaged food and beverages further fuels the demand for overprint varnishes in this segment.

The Pharmaceuticals segment holds a significant share in the market, as overprint varnishes play a crucial role in protecting drug packaging from external factors such as humidity, friction, and contamination. These varnishes help maintain the readability of critical information, including dosage instructions and expiration dates, while ensuring compliance with regulatory requirements. The preference for solvent-based and UV-coated varnishes is high in this segment due to their superior durability and resistance to environmental exposure.

The Personal Care & Cosmetics segment is witnessing steady growth as brands focus on premium packaging solutions to enhance product appeal. Overprint varnishes provide a glossy, matte, or textured finish that adds sophistication to cosmetic packaging while protecting labels from smudging and fading. UV-coated varnishes are widely used in this segment to achieve high-definition printing with enhanced durability, especially for luxury and high-end cosmetic brands.

The Consumer Goods segment benefits from the widespread use of overprint varnishes in packaging for electronics, household items, and other retail products. These varnishes improve the visual aesthetics and longevity of printed surfaces, making them more resistant to scratches, chemicals, and external wear. Water-based and synthetic varnishes are commonly used in this segment due to their balance of cost-effectiveness, environmental compliance, and performance.

Segmentation Insights by Functionality

On the basis of functionality, the global overprint varnish market is bifurcated into gloss, matte, satin, and anti-scratch overprint vaish.

The Gloss segment dominates the Overprint Varnish Market, driven by its widespread use in enhancing the visual appeal of packaging and printed materials. Glossy overprint varnishes provide a high-shine, reflective finish that makes colors appear more vibrant and attractive. This functionality is particularly popular in food and beverage packaging, labeling solutions, and personal care products, where brand differentiation and premium aesthetics are essential. The demand for UV-coated gloss varnishes is growing due to their superior durability, resistance to smudging, and ability to maintain a fresh, high-quality look over time.

The Matte segment holds a significant share in the market, offering a non-reflective, sophisticated finish that enhances readability and provides a soft-touch effect. Matte overprint varnishes are preferred in pharmaceutical packaging, luxury cosmetics, and premium branding materials where subtle elegance is prioritized over high-gloss shine. These varnishes reduce glare, making printed information easier to read, which is particularly useful for product labels and instructional packaging.

The Satin segment is gaining traction as it offers a balance between gloss and matte finishes, providing a soft sheen without excessive reflection. Satin overprint varnishes are widely used in high-end personal care packaging, book covers, and specialty printing applications where a refined look is desired without the extreme shine of gloss or the flat effect of matte. The increasing demand for premium packaging solutions across industries is contributing to the steady growth of this segment.

The Anti-Scratch Overprint Varnish segment is experiencing rising demand, particularly in applications where durability and surface protection are critical. This functionality is highly valued in pharmaceutical packaging, electronic goods, and high-end printed materials that require resistance to abrasions, scuffs, and handling wear. Anti-scratch varnishes extend the lifespan of printed materials and improve product integrity, making them a preferred choice for long-lasting packaging solutions.

Segmentation Insights by Technology

On the basis of technology, the global overprint varnish market is bifurcated into flexographic printing, gravure printing, lithographic printing, and digital printing.

The Flexographic Printing segment dominates the Overprint Varnish Market due to its versatility, high-speed production capabilities, and cost-effectiveness in large-scale printing. Flexographic printing is widely used in food packaging, labeling solutions, and flexible packaging applications where overprint varnishes are essential for protection and aesthetic enhancement. Water-based and UV-coated varnishes are commonly applied in this segment, providing excellent adhesion, durability, and compliance with food safety regulations. The growing demand for sustainable and eco-friendly packaging solutions is further driving the adoption of flexographic printing with overprint varnishes.

The Gravure Printing segment holds a significant share in the market, particularly in high-volume printing applications requiring superior image quality and consistency. Gravure printing is commonly used for premium food packaging, pharmaceuticals, and high-end cosmetic products where overprint varnishes enhance durability and visual appeal. Solvent-based and UV-cured varnishes are popular in this segment due to their excellent resistance to wear, smudging, and environmental exposure. The high initial setup cost of gravure printing limits its use to large-scale production runs, but its ability to deliver high-quality, long-lasting prints makes it a preferred choice for luxury and high-end packaging.

The Lithographic Printing segment is steadily growing, primarily in commercial printing, cartons, and specialty packaging applications. Overprint varnishes in this segment provide added protection against moisture, fading, and handling damage while enhancing the print’s overall aesthetic. Lithographic printing is commonly used for rigid packaging, promotional materials, and high-end labels, where gloss, matte, or satin varnishes help achieve premium finishes. The increasing demand for sophisticated packaging in industries such as consumer goods, cosmetics, and electronics is fueling the adoption of lithographic printing with overprint varnishes.

The Digital Printing segment is witnessing rapid growth, driven by advancements in on-demand printing, personalization, and short-run production. Digital printing is widely used for customized packaging, variable data printing, and specialty labels, where overprint varnishes enhance durability, color vibrancy, and print longevity. UV-cured and water-based varnishes are frequently used in this segment, ensuring protection against scratches, smudging, and environmental factors. The rise of e-commerce, personalized packaging trends, and digital label printing is significantly boosting the demand for overprint varnishes in digital printing applications.

Overprint Varnish Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the Overprint Varnish Market, supported by strong demand from the packaging, publishing, and commercial printing sectors. The United States leads the market due to the growing need for high-quality, durable, and visually appealing printed materials in the food and beverage, pharmaceutical, and consumer goods industries. The increasing adoption of UV-cured and water-based overprint varnishes, driven by strict environmental regulations and sustainability initiatives, is further fueling market growth. Canada is also witnessing steady demand, particularly in the premium packaging and advertising sectors, where high-gloss and matte varnishes are widely used to enhance visual appeal and product differentiation.

Europe is another key market, driven by stringent environmental regulations, increasing demand for sustainable printing solutions, and strong growth in the luxury packaging industry. Germany, France, and the UK are major contributors. Germany, a leader in printing and packaging technologies, is witnessing rising adoption of eco-friendly overprint varnishes, particularly in the food and pharmaceutical sectors. France’s strong cosmetics and luxury goods industries are fueling demand for premium overprint coatings that enhance branding and packaging aesthetics. The UK is also seeing growth, with increased use of high-performance varnishes in commercial printing and e-commerce packaging to improve durability and print longevity.

Asia Pacific is the fastest-growing region in the Overprint Varnish Market, fueled by rapid expansion in the packaging, publishing, and commercial printing industries. China, India, Japan, and South Korea are major markets. China’s booming e-commerce sector and strong manufacturing base are driving demand for high-quality printed packaging materials, increasing the use of gloss, matte, and UV-cured overprint varnishes. India’s expanding print and packaging industry, supported by growing demand for flexible and rigid packaging solutions, is also boosting market growth. Japan, known for its high-quality printing technology, is experiencing rising adoption of specialty overprint varnishes in premium packaging and commercial printing applications. South Korea is seeing increasing demand for sustainable and low-VOC varnishes, particularly in electronics packaging and high-end product labeling.

Latin America is experiencing moderate growth, with Brazil and Mexico leading the market. The demand for overprint varnishes in the region is primarily driven by the growing packaging and advertising industries. Brazil’s strong food and beverage packaging sector is fueling demand for protective and decorative overprint coatings that enhance shelf appeal and durability. Mexico’s expanding printing industry, particularly in labels and flexible packaging, is also contributing to market growth. However, economic fluctuations and raw material price volatility may pose challenges to widespread adoption in some Latin American countries.

The Middle East & Africa is witnessing steady growth, particularly in the UAE, Saudi Arabia, and South Africa. The increasing demand for high-quality printed packaging in the luxury goods, cosmetics, and food industries is driving market expansion. The UAE’s strong retail and hospitality industries are fueling demand for premium overprint varnishes used in advertising and branding applications. Saudi Arabia’s growing industrial and commercial packaging sectors are also adopting high-performance varnishes for better print protection and longevity. In Africa, the rising demand for packaged consumer goods and increasing investments in the printing sector are supporting market growth, though challenges such as limited access to advanced printing technologies may hinder faster adoption.

Overprint Varnish Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the overprint varnish market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global overprint varnish market include:

- Altana

- American Offset Printing Ink

- Anwin Technology Co. LTD.

- As Inc. Co. Ltd.

- BRANCHER

- CHT/BEZEMA

- Eston Chimica

- Huber Group

- Imperial Ink Private Limited

- JPT Corporation Ltd

- Michelma

- Superior Printing Inks

- Toyo Ink

- Van Son Ink Corporation

- Zeller+Gmelin Group

The global overprint varnish market is segmented as follows:

By Material

- Synthetic

- Water Based

- UV Coated

- Solvent Based

By Application

- Food Packaging

- Non-food Packaging

- Labeling Solutions

- Folding Cartons

By End Use Industry

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Consumer Goods

By Functionality

- Gloss

- Matte

- Satin

- Anti-scratch

By Technology

- Flexographic Printing

- Gravure Printing

- Lithographic Printing

- Digital Printing

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Overprint Varnish

Request Sample

Overprint Varnish