Passenger Vehicle Propeller Shaft Market Size, Share, and Trends Analysis Report

CAGR :

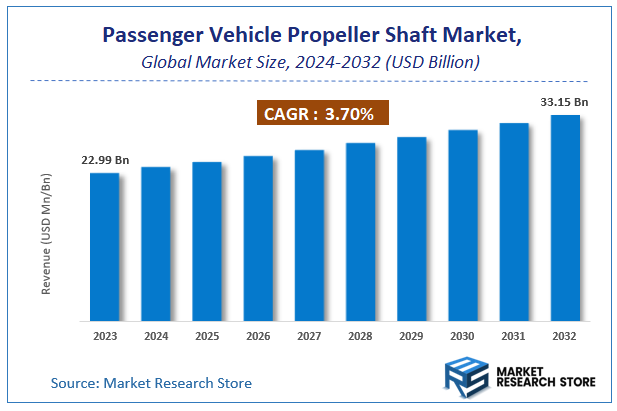

| Market Size 2023 (Base Year) | USD 22.99 Billion |

| Market Size 2032 (Forecast Year) | USD 33.15 Billion |

| CAGR | 3.7% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Passenger Vehicle Propeller Shaft Market Insights

According to Market Research Store, the global passenger vehicle propeller shaft market size was valued at around USD 22.99 billion in 2023 and is estimated to reach USD 33.15 billion by 2032, to register a CAGR of approximately 3.7% in terms of revenue during the forecast period 2024-2032.

The passenger vehicle propeller shaft report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Passenger Vehicle Propeller Shaft Market: Overview

The Passenger Vehicle Propeller Shaft market is witnessing steady growth, driven by increasing vehicle production, rising demand for all-wheel-drive (AWD) and four-wheel-drive (4WD) systems, and advancements in lightweight and high-strength materials. A propeller shaft, also known as a driveshaft, is a crucial component in rear-wheel-drive (RWD), AWD, and 4WD vehicles, transmitting torque from the engine and transmission to the wheels. These shafts are commonly made from steel, aluminum, or carbon fiber composites, balancing durability, weight reduction, and performance efficiency.

Market expansion is fueled by the growing popularity of SUVs and crossovers, which typically require robust drivetrain systems, including advanced propeller shafts for enhanced power distribution and off-road capabilities. Additionally, the increasing adoption of electric vehicles (EVs) with multi-motor AWD configurations is driving demand for lightweight and high-efficiency propeller shafts to optimize vehicle performance. Advances in materials and manufacturing techniques, such as hollow shaft designs and composite materials, are improving strength while reducing overall vehicle weight, contributing to better fuel efficiency and reduced emissions.

Key Highlights

- The passenger vehicle propeller shaft market is anticipated to grow at a CAGR of 3.7% during the forecast period.

- The global passenger vehicle propeller shaft market was estimated to be worth approximately USD 22.99 billion in 2023 and is projected to reach a value of USD 33.15 billion by 2032.

- The growth of the passenger vehicle propeller shaft market is being driven by the increasing production and sales of passenger vehicles, particularly SUVs and light trucks, which often utilize propeller shafts for all-wheel or four-wheel drive systems.

- Based on the product, the passenger cars segment is growing at a high rate and is projected to dominate the market.

- On the basis of axle, the driven axles segment is projected to swipe the largest market share.

- In terms of propulsion, the internal combustion engine vehicles segment is expected to dominate the market.

- Based on the material, the steel segment is expected to dominate the market.

- Based on the application, the front axle segment is expected to dominate the market.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Passenger Vehicle Propeller Shaft Market: Dynamics

Key Drivers

- Increasing Vehicle Production: Global growth in passenger car production directly fuels the demand for propeller shafts, as they are essential components in rear-wheel-drive and all-wheel-drive vehicles.

- Rising Demand for SUVs and Light Trucks: The increasing popularity of SUVs and light trucks, which often utilize propeller shafts for power transmission to the rear axle, is a significant driver.

- Technological Advancements: Innovations in propeller shaft design and materials, such as lightweight materials (aluminum, composites) and improved vibration damping, are driving market growth.

- Growing Focus on Vehicle Performance and Handling: Propeller shafts play a crucial role in vehicle performance and handling, particularly in all-wheel-drive vehicles. Demand for improved performance contributes to market growth.

Restraints

- Shift Towards Front-Wheel Drive Vehicles: The increasing popularity of front-wheel-drive vehicles, which do not require propeller shafts, can pose a long-term challenge to the market.

- Electric Vehicle (EV) Adoption: Electric vehicles, especially those with all-wheel drive, often utilize different powertrain configurations that may not require traditional propeller shafts, impacting the market in the long run.

- Cost of Materials and Manufacturing: High-quality propeller shafts, especially those made from advanced materials, can be expensive to produce, which can be a barrier for some vehicle manufacturers.

- Maintenance Requirements: Propeller shafts require periodic maintenance, including lubrication and inspection, which can be a recurring cost for vehicle owners.

Opportunities

- Development of Lightweight and High-Strength Propeller Shafts: Focus on developing lighter propeller shafts made from materials like aluminum, composites, or advanced steel alloys to improve fuel efficiency and vehicle performance.

- Integration of Smart Technologies: Integrating sensors and smart technologies into propeller shafts to monitor vibration, balance, and other performance parameters can enhance reliability and predictive maintenance.

- Focus on Emerging Markets: Expanding into emerging markets with growing vehicle ownership and increasing demand for all-wheel-drive vehicles presents significant growth opportunities.

- Aftermarket Sales and Services: The aftermarket for propeller shaft replacements and repairs offers a steady revenue stream for manufacturers and service providers.

Challenges

- Ensuring Quality and Reliability: Maintaining consistent quality and reliability of propeller shafts is crucial, as they are critical components for vehicle safety and performance.

- Meeting Stringent Performance Standards: Propeller shafts must meet stringent performance standards related to balance, vibration, noise, and durability.

- Staying Competitive: The propeller shaft market is competitive, requiring manufacturers to continuously innovate and offer cost-effective solutions.

- Managing Supply Chain Disruptions: Global supply chain disruptions can impact the availability of raw materials and components needed for propeller shaft manufacturing.

Passenger Vehicle Propeller Shaft Market: Report Scope

This report thoroughly analyzes the Passenger Vehicle Propeller Shaft Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Passenger Vehicle Propeller Shaft Market |

| Market Size in 2023 | USD 22.99 Billion |

| Market Forecast in 2032 | USD 33.15 Billion |

| Growth Rate | CAGR of 3.7% |

| Number of Pages | 187 |

| Key Companies Covered | GKN, NTN, SDS, Dana, Nexteer, Hyundai-Wia, IFA Rotorion, Meritor, AAM, Neapco, JTEKT, Yuandong, Wanxiang |

| Segments Covered | By Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Passenger Vehicle Propeller Shaft Market: Segmentation Insights

The global passenger vehicle propeller shaft market is divided by product, axle, propulsion, material, application, and region.

Segmentation Insights by Product

Based on product, the global passenger vehicle propeller shaft market is divided into passenger cars, light commercial vehicles, and heavy commercial vehicles.

The Passenger Cars segment dominates the Passenger Vehicle Propeller Shaft Market due to the high global production and sales of passenger vehicles. Increasing consumer demand for fuel-efficient and lightweight propeller shafts, along with advancements in materials such as carbon fiber and aluminum, is driving growth in this segment. Additionally, the rise in all-wheel-drive (AWD) and four-wheel-drive (4WD) configurations, particularly in SUVs and crossovers, has further boosted the adoption of advanced propeller shafts. Automakers are increasingly focusing on optimizing drivetrain efficiency and reducing vehicle weight, making lightweight and high-strength propeller shafts a critical component in modern passenger cars.

The Light Commercial Vehicles (LCVs) segment holds a significant share due to the rising demand for cargo vans, pickup trucks, and utility vehicles in urban logistics and e-commerce transportation. LCVs require durable and high-performance propeller shafts to handle frequent load variations and longer operational hours. Growth in small and medium enterprises (SMEs), last-mile delivery services, and infrastructure projects further supports the expansion of this segment.

The Heavy Commercial Vehicles (HCVs) segment, while smaller in volume compared to passenger cars and LCVs, plays a crucial role in industrial and logistics applications. These vehicles require robust and high-torque-capable propeller shafts to ensure durability under heavy loads. The increasing adoption of long-haul trucks, construction equipment, and mining vehicles is contributing to steady demand in this segment. Additionally, advancements in drivetrain technology and the integration of hybrid and electric powertrains in heavy commercial vehicles are influencing propeller shaft innovation.

Segmentation Insights by Axle

On the basis of application, the global passenger vehicle propeller shaft market is bifurcated into driven axles, and non-driven axles.

The Driven Axles segment dominates the Passenger Vehicle Propeller Shaft Market due to its critical role in transmitting power from the engine to the wheels, ensuring efficient vehicle movement. Driven axles are essential in both front-wheel-drive (FWD) and rear-wheel-drive (RWD) configurations, as well as in all-wheel-drive (AWD) and four-wheel-drive (4WD) vehicles, which are increasingly popular in SUVs and performance-oriented passenger cars. The growing demand for fuel efficiency and enhanced drivetrain performance has led to advancements in lightweight materials such as aluminum and carbon fiber for driven axle propeller shafts, further driving market growth. Additionally, the rise in electric and hybrid vehicles, which require specialized drive axles, is expected to boost demand in this segment.

The Non-Driven Axles segment holds a significant share, primarily in vehicles with FWD configurations where the rear axle does not receive power. These axles play a crucial role in load distribution, stability, and vehicle handling. Increasing adoption of lightweight chassis components and improvements in axle design are enhancing the efficiency and performance of non-driven axles. While this segment does not directly contribute to power transmission, the ongoing development of independent rear suspension systems and adaptive chassis technologies continues to influence the market for non-driven axles.

Segmentation Insights by Propulsion

On the basis of propulsion, the global passenger vehicle propeller shaft market is bifurcated into internal combustion engine vehicles, electric vehicles, and hybrid vehicles.

The Internal Combustion Engine (ICE) Vehicles segment dominates the Passenger Vehicle Propeller Shaft Market due to the widespread use of traditional gasoline and diesel-powered vehicles globally. Propeller shafts in ICE vehicles are crucial for transmitting power from the engine to the wheels, particularly in rear-wheel-drive (RWD), all-wheel-drive (AWD), and four-wheel-drive (4WD) configurations. The demand for lightweight and high-strength materials, such as carbon fiber and aluminum, is driving innovations in propeller shaft technology to improve fuel efficiency and reduce emissions. Despite the rise of electric mobility, the strong presence of ICE vehicles, especially in developing markets, continues to sustain the demand for propeller shafts.

The Hybrid Vehicles segment is growing steadily, driven by the increasing adoption of fuel-efficient and low-emission technologies. Hybrid vehicles, particularly plug-in hybrid electric vehicles (PHEVs), use propeller shafts in configurations that incorporate both internal combustion engines and electric powertrains. Automakers are focusing on optimizing hybrid drivetrain components, including lightweight and high-performance propeller shafts, to enhance vehicle efficiency and driving dynamics. The rising global push for electrification, along with stringent emission regulations, is expected to further boost the adoption of propeller shafts in hybrid vehicles.

The Electric Vehicles (EVs) segment is witnessing rapid growth, driven by the global shift towards sustainable transportation and advancements in battery technology. While many EVs use direct-drive systems without traditional propeller shafts, certain all-wheel-drive and high-performance electric models still incorporate advanced propeller shafts to improve power distribution and handling. Innovations in shaft materials and designs are emerging to meet the unique requirements of EV drivetrains, including weight reduction and enhanced efficiency. The expanding EV market, supported by government incentives and infrastructure development, is expected to create new opportunities for specialized propeller shaft applications.

Segmentation Insights by Material

On the basis of material, the global passenger vehicle propeller shaft market is bifurcated into steel, aluminum, and carbon fiber.

The Steel segment dominates the Passenger Vehicle Propeller Shaft Market due to its high strength, durability, and cost-effectiveness. Steel propeller shafts are widely used in internal combustion engine (ICE) vehicles, particularly in heavy-duty applications that require high torque transmission. Their ability to withstand stress and impact makes them the preferred choice for traditional rear-wheel-drive (RWD) and all-wheel-drive (AWD) configurations. However, steel shafts are relatively heavier, which can impact fuel efficiency. Automakers are increasingly focusing on advanced steel alloys to enhance strength while reducing weight, aligning with fuel efficiency and emission reduction goals.

The Aluminum segment is gaining traction as automakers seek lightweight alternatives to improve vehicle efficiency. Aluminum propeller shafts offer a significant weight reduction compared to steel, leading to improved fuel economy and reduced emissions. Additionally, aluminum provides better corrosion resistance, making it suitable for vehicles exposed to harsh environments. While aluminum shafts are more expensive than steel counterparts, their advantages in weight savings and performance enhancement are driving their adoption, particularly in hybrid vehicles and performance-oriented passenger cars.

The Carbon Fiber segment is witnessing rapid growth, driven by the demand for high-performance and premium vehicles. Carbon fiber propeller shafts offer superior strength-to-weight ratio, exceptional durability, and vibration dampening properties, enhancing vehicle performance and driving comfort. Their lightweight nature contributes to improved acceleration and handling, making them ideal for sports cars and electric vehicles (EVs). However, the high production cost of carbon fiber limits its widespread adoption. As manufacturing techniques advance and costs decrease, carbon fiber propeller shafts are expected to see increased usage, especially in the luxury and high-performance vehicle segments.

Segmentation Insights by Application

On the basis of application, the global passenger vehicle propeller shaft market is bifurcated into front axle, rear axle, and propeller shaft.

The Front Axle segment dominates the Passenger Vehicle Propeller Shaft Market, primarily in front-wheel-drive (FWD) vehicles where the engine power is transmitted directly to the front wheels. Front axles play a crucial role in steering and load-bearing, requiring robust and durable propeller shafts to ensure stability and efficiency. With the increasing adoption of compact and fuel-efficient vehicles, the demand for front axle propeller shafts remains strong, particularly in urban and economy car segments. Automakers continue to innovate by integrating lightweight materials such as aluminum and advanced steel alloys to enhance vehicle performance and efficiency.

The Rear Axle segment is significant in rear-wheel-drive (RWD) and all-wheel-drive (AWD) vehicles, where the propeller shaft transfers power from the engine to the rear wheels. This configuration is common in SUVs, trucks, and performance vehicles that require higher torque and better traction. Rear axle propeller shafts are typically constructed from high-strength steel or aluminum to withstand heavy loads and harsh driving conditions. As consumer demand for SUVs and off-road vehicles continues to rise, the rear axle segment is expected to witness steady growth.

The Propeller Shaft segment plays a vital role in power transmission between the front and rear axles, particularly in AWD and four-wheel-drive (4WD) vehicles. Propeller shafts ensure seamless torque distribution, improving traction and vehicle stability in challenging terrains. Automakers are increasingly focusing on lightweight materials such as carbon fiber to enhance performance, reduce vibrations, and improve fuel efficiency. With the growing demand for electric and hybrid vehicles that incorporate advanced drivetrain technologies, the propeller shaft segment is expected to evolve with innovative material compositions and design enhancements.

Passenger Vehicle Propeller Shaft Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

The Asia-Pacific (APAC) region dominates the global passenger vehicle propeller shaft market, driven by robust automotive production, increasing vehicle demand, and expanding manufacturing hubs in countries like China, India, Japan, and South Korea. According to recent industry reports, APAC attributed to the strong presence of leading automakers and rising investments in electric and hybrid vehicles. China, the largest automotive market, significantly contributes due to high passenger car sales and government initiatives promoting lightweight and fuel-efficient drivetrain components. North America and Europe follow, with steady growth propelled by advancements in all-wheel-drive (AWD) systems and stringent emission norms favoring lightweight propeller shafts. However, APAC's dominance is expected to strengthen further, supported by rapid urbanization and increasing disposable incomes.

North America holds a significant share in the passenger vehicle propeller shaft market, driven by high demand for SUVs, pickup trucks, and electric vehicles. The U.S. dominates due to strong automotive production and technological advancements in lightweight composite shafts. Strict fuel efficiency regulations are pushing manufacturers toward advanced materials like carbon fiber.

Europe is a key market, with Germany, France, and Italy leading due to premium vehicle production and stringent emission norms. The shift toward electric and hybrid vehicles is increasing demand for high-performance propeller shafts.

Passenger Vehicle Propeller Shaft Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the passenger vehicle propeller shaft market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global passenger vehicle propeller shaft market include:

- AAM

- American Axle Manufacturing

- Amtek Auto Ltd

- Camshafts International

- Dana

- Dana Incorporated

- GKN

- GKN Driveline (A Division of GKN)

- Hangzhou Aobo Technology

- Hayes Lemmerz International

- Hyundai-Wia

- IFA Rotorion

- Ikeda Bussan

- JTEKT

- Meritor

- Neapco

- Nexteer

- NTN

- SDS

- Tata AutoComp

- Transamerican Auto Parts

- Tuscan Driveline (Part of Tuscan Engineering)

- Wanxiang

- Yokohama Drive System (A Division of Yokohama Rubber Company)

- Yuandong

The global passenger vehicle propeller shaft market is segmented as follows:

By Product

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Axle

- Driven Axles

- Non-Driven Axles

By Propulsion

- Internal Combustion Engine Vehicles

- Electric Vehicles

- Hybrid Vehicles

By Material

- Steel

- Aluminum

- Carbon Fiber

By Application

- Front Axle

- Rear Axle

- Propeller Shaft

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Passenger Vehicle Propeller Shaft

Request Sample

Passenger Vehicle Propeller Shaft