Percutaneous Indwelling Central Catheter Market Size, Share, and Trends Analysis Report

CAGR :

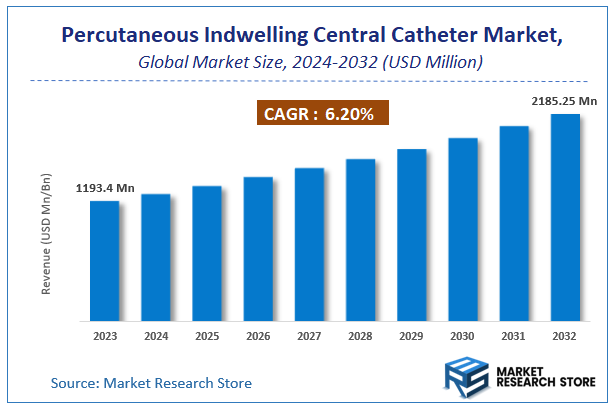

| Market Size 2023 (Base Year) | USD 1193.4 Million |

| Market Size 2032 (Forecast Year) | USD 2185.25 Million |

| CAGR | 6.2% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Percutaneous Indwelling Central Catheter Market Insights

According to Market Research Store, the global percutaneous indwelling central catheter market size was valued at around USD 1193.4 million in 2023 and is estimated to reach USD 2185.25 million by 2032, to register a CAGR of approximately 6.2% in terms of revenue during the forecast period 2024-2032.

The percutaneous indwelling central catheter report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Percutaneous Indwelling Central Catheter Market: Overview

The Percutaneous Indwelling Central Catheter market is experiencing steady growth, driven by the increasing prevalence of chronic diseases, rising demand for long-term intravenous therapies, and advancements in catheterization technology. Percutaneous indwelling central catheters (PICCs) are widely used in hospitals, outpatient clinics, and home healthcare settings for administering chemotherapy, parenteral nutrition, antibiotics, and other long-term medications. These catheters offer advantages such as reduced risk of infection, improved patient comfort, and ease of insertion compared to traditional central venous catheters.

Market expansion is fueled by the growing incidence of conditions requiring long-term vascular access, such as cancer, chronic kidney disease, and autoimmune disorders. Additionally, the increasing adoption of minimally invasive procedures and the rising preference for home-based treatments are driving demand for PICCs. Technological advancements, including antimicrobial coatings, ultrasound-guided insertion techniques, and pressure-resistant catheter materials, are further improving safety and efficacy.

Key Highlights

- The percutaneous indwelling central catheter market is anticipated to grow at a CAGR of 6.2% during the forecast period.

- The global percutaneous indwelling central catheter market was estimated to be worth approximately USD 1193.4 million in 2023 and is projected to reach a value of USD 2185.25 million by 2032.

- The growth of the percutaneous indwelling central catheter market is being driven by the increasing demand for long-term intravenous access, the rising prevalence of chronic diseases requiring prolonged treatment, and the growing preference for minimally invasive procedures.

- Based on the product, the conventional PICC segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the hospitals segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Percutaneous Indwelling Central Catheter Market: Dynamics

Key Drivers

- Increased Use of Long-Term Intravenous Therapies: The rising prevalence of chronic diseases requiring long-term intravenous therapies, such as cancer, infections, and nutritional deficiencies, is a primary driver. PICCs offer a convenient and reliable way to administer these therapies.

- Growing Geriatric Population: The aging population, often requiring prolonged intravenous treatments, contributes to the demand for PICCs.

- Preference for Outpatient and Home Care: The shift towards outpatient and home-based care models is driving the use of PICCs, as they allow patients to receive intravenous therapies outside of the hospital setting, improving patient comfort and reducing healthcare costs.

- Reduced Risk of Complications Compared to Other Central Lines: PICCs are associated with a lower risk of certain complications, such as pneumothorax, compared to other central venous catheters, making them a preferred choice in many clinical settings.

- Technological Advancements: Innovations in PICC design, materials, and insertion techniques are improving patient safety, comfort, and ease of use, further driving market growth.

Restraints

- Risk of Complications: Despite their advantages, PICCs are associated with potential complications, such as infections, thrombosis, and catheter dislodgement, which can limit their use in some patients.

- Cost: PICC insertion and maintenance can be costly, which can be a barrier for some patients and healthcare systems.

- Need for Skilled Personnel: PICC insertion and management require trained healthcare professionals, which can limit their availability in some settings.

- Patient Discomfort: Some patients may experience discomfort or pain during PICC insertion or while the catheter is in place.

Opportunities

- Development of Antimicrobial and Antithrombotic PICCs: Developing PICCs with antimicrobial or antithrombotic coatings can further reduce the risk of complications, expanding their applications.

- Focus on Home Care and Self-Administration: Developing PICCs designed for easier home care management and self-administration can improve patient convenience and reduce healthcare costs.

- Integration with Telehealth and Remote Monitoring: Integrating PICCs with telehealth platforms and remote monitoring technologies can improve patient care and allow for early detection of complications.

- Expanding Applications in Pediatric and Neonatal Care: Developing PICCs specifically designed for pediatric and neonatal patients can address the unique needs of these populations.

Challenges

- Minimizing Complication Rates: Continuously improving PICC design and insertion techniques to minimize the risk of complications is a key challenge.

- Improving Patient Comfort: Developing PICCs that are more comfortable and less prone to dislodgement can improve patient compliance and satisfaction.

- Standardizing Insertion and Maintenance Protocols: Standardizing PICC insertion and maintenance protocols across different healthcare settings can improve patient safety and reduce variability in care.

- Competing with Other Vascular Access Devices: The PICC market faces competition from other vascular access devices, such as central venous catheters and peripheral intravenous catheters, requiring manufacturers to demonstrate the unique advantages of PICCs.

Percutaneous Indwelling Central Catheter Market: Report Scope

This report thoroughly analyzes the Percutaneous Indwelling Central Catheter Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Percutaneous Indwelling Central Catheter Market |

| Market Size in 2023 | USD 1193.4 Million |

| Market Forecast in 2032 | USD 2185.25 Million |

| Growth Rate | CAGR of 6.2% |

| Number of Pages | 174 |

| Key Companies Covered | AngioDynamics, C. R. Bard, Teleflex Incorporated, B. Braun Melsungen, Medtronic, Vygon, Cook Medical, Argon Medical Devices, Medical Component, Theragenics Corporation |

| Segments Covered | By Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Percutaneous Indwelling Central Catheter Market: Segmentation Insights

The global percutaneous indwelling central catheter market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global percutaneous indwelling central catheter market is divided into conventional PICC, and power-injectable PICC.

The Conventional PICC segment dominates the percutaneous indwelling central catheter market due to its widespread use in long-term intravenous therapy, chemotherapy, and parenteral nutrition. These catheters offer a cost-effective and reliable solution for patients requiring extended vascular access, minimizing the need for repeated needle insertions. Hospitals and outpatient care settings frequently utilize conventional PICCs due to their proven efficacy, lower risk of infection compared to central venous catheters, and ease of placement by trained medical professionals. Additionally, advancements in catheter material and design, including antimicrobial coatings, have further enhanced their safety and longevity, making them the preferred choice in many clinical settings.

The Power-Injectable PICC segment is experiencing significant growth due to its ability to withstand high-pressure injections required for contrast-enhanced imaging procedures such as CT scans. These catheters provide dual functionality, allowing both routine intravenous therapy and rapid contrast media administration without requiring additional venous access. Their increasing adoption in hospitals, diagnostic centers, and emergency departments is driven by the need for efficient imaging diagnostics and improved patient comfort. Additionally, the rising prevalence of chronic diseases, such as cancer and cardiovascular disorders, which require frequent imaging and long-term intravenous therapy, is further propelling demand for power-injectable PICCs.

Segmentation Insights by Application

On the basis of application, the global percutaneous indwelling central catheter market is bifurcated into hospitals, and catheterization laboratories.

The Hospitals segment dominates the percutaneous indwelling central catheter market due to the high patient inflow requiring long-term intravenous therapy, chemotherapy, and parenteral nutrition. Hospitals serve as primary centers for catheter placement, particularly for patients with chronic illnesses, post-surgical recovery, and intensive care needs. The availability of trained healthcare professionals, advanced imaging techniques for catheter placement, and strict infection control protocols further contribute to the widespread use of PICCs in hospital settings. Additionally, the increasing prevalence of conditions such as cancer, cardiovascular diseases, and infectious diseases requiring prolonged IV treatments is driving demand for PICCs in hospitals.

The Catheterization Laboratories segment is also growing steadily, as these specialized medical facilities focus on the insertion and management of vascular access devices, including PICCs. Catheterization labs are particularly utilized for patients requiring precise catheter placement using fluoroscopic guidance, ensuring optimal positioning and reducing complications. The rise in minimally invasive procedures and advancements in catheter placement techniques are further supporting the growth of this segment. However, hospitals continue to hold the largest market share due to their comprehensive patient care infrastructure and ability to handle complex medical conditions requiring PICC insertion.

Percutaneous Indwelling Central Catheter Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the Percutaneous Indwelling Central Catheter Market due to the high prevalence of chronic diseases such as cancer, kidney disorders, and cardiovascular conditions. The United States is the largest contributor, with a well-established healthcare infrastructure and strong adoption of PICC lines in hospitals, ambulatory care centers, and home care settings. The increasing preference for peripherally inserted central catheters in oncology patients undergoing chemotherapy, along with advancements in antimicrobial-coated catheters to reduce infections, is driving market growth. Canada is also witnessing rising demand for PICCs, supported by an aging population and increasing hospital admissions requiring long-term IV therapies. The presence of key market players, ongoing clinical research, and reimbursement policies further enhance market expansion in North America.

Europe is another key market, supported by an increasing geriatric population, rising incidence of chronic illnesses, and government initiatives to improve healthcare services. Germany, the UK, and France are the major contributors. Germany, with its strong medical device industry, is experiencing high demand for PICCs in intensive care units (ICUs) and oncology wards. The UK’s National Health Service (NHS) is promoting the use of percutaneous catheters for long-term IV access, contributing to market growth. France is witnessing increased adoption of antimicrobial and biofilm-resistant catheters to reduce catheter-related bloodstream infections (CRBSIs), enhancing safety in clinical settings. The European Union’s stringent regulations for medical devices and growing investments in catheter technology development are further supporting market expansion.

Asia Pacific is the fastest-growing region in the Percutaneous Indwelling Central Catheter Market, driven by rising healthcare expenditures, increasing prevalence of chronic diseases, and expanding medical infrastructure. China, Japan, India, and South Korea are major markets. China’s rapidly growing healthcare sector and increasing number of cancer patients undergoing chemotherapy are fueling demand for PICC lines. Japan and South Korea, with their advanced medical technologies, are experiencing a rise in the adoption of innovative catheter materials that enhance patient comfort and reduce infection risks. India, with its large population and increasing access to advanced medical treatments, is witnessing growing demand for PICCs in hospitals and home healthcare settings. Government initiatives to improve critical care services and rising awareness about infection control in medical procedures are further supporting market growth in Asia Pacific.

Latin America is experiencing moderate growth, with Brazil and Mexico leading the market. The demand for PICCs is increasing due to the rising burden of chronic diseases, improving healthcare access, and growing adoption of home-based healthcare services. Brazil’s healthcare sector is seeing a surge in catheter usage for long-term IV treatments in cancer and dialysis patients. Mexico’s expanding private healthcare sector is also contributing to market growth, with hospitals and outpatient clinics increasingly incorporating percutaneous catheters in treatment protocols. However, economic challenges and limited availability of advanced catheterization technologies may hinder faster market expansion in some Latin American countries.

The Middle East & Africa is witnessing steady market expansion, particularly in the UAE, Saudi Arabia, and South Africa. The growing prevalence of cancer, increasing demand for critical care services, and rising healthcare investments are driving demand for PICC lines in the region. Saudi Arabia’s Vision 2030 healthcare initiatives and increasing government efforts to modernize medical infrastructure are contributing to market growth. The UAE is also seeing rising adoption of advanced catheterization techniques in hospitals and specialized oncology centers. However, limited affordability and access to high-end catheter technologies in some African nations may pose challenges to market expansion.

Percutaneous Indwelling Central Catheter Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the percutaneous indwelling central catheter market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global percutaneous indwelling central catheter market include:

- AngioDynamics

- Argon Medical Devices

- B. Braun Melsungen

- C. R. Bard

- Cook Medical

- Medical Component

- Medtronic

- Teleflex Incorporated

- Theragenics Corporation

- Vygon

The global percutaneous indwelling central catheter market is segmented as follows:

By Product

- Conventional PICC

- Power-Injectable PICC

By Application

- Hospitals

- Catheterization Laboratories

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

What are the significant factors driving the global Percutaneous Indwelling Central Catheter market?

Table Of Content

Inquiry For Buying

Percutaneous Indwelling Central Catheter

Request Sample

Percutaneous Indwelling Central Catheter