Power Generation, Transmission and Control Market Size, Share, and Trends Analysis Report

CAGR :

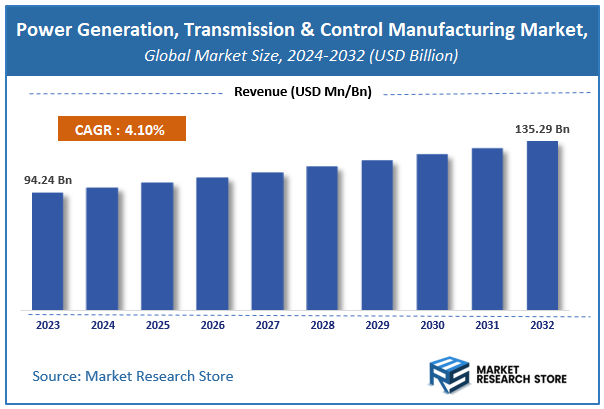

| Market Size 2023 (Base Year) | USD 94.24 Billion |

| Market Size 2032 (Forecast Year) | USD 135.29 Billion |

| CAGR | 4.1% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Power Generation, Transmission And Control Manufacturing Market Insights

According to Market Research Store, the global power generation, transmission and control manufacturing market size was valued at around USD 94.24 billion in 2023 and is estimated to reach USD 135.29 billion by 2032, to register a CAGR of approximately 4.1% in terms of revenue during the forecast period 2024-2032.

The power generation, transmission and control manufacturing report provide a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Power Generation, Transmission and Control Manufacturing Market: Overview

Power generation, transmission, and control manufacturing refers to the industrial production of equipment and systems that are essential for generating electricity, transmitting it over distances, and controlling its distribution and use. This includes the manufacturing of turbines, generators, transformers, switchgear, and control systems that regulate electricity flow across grids and within industrial, commercial, and residential applications. The sector plays a critical role in enabling energy infrastructure by supporting the operation of power plants, renewable energy installations, and smart grids. It is integral to global efforts toward energy security, efficiency, and sustainability.

Key Highlights

- The power generation, transmission and control manufacturing market is anticipated to grow at a CAGR of 4.1% during the forecast period.

- The global power generation, transmission and control manufacturing market was estimated to be worth approximately USD 94.24 billion in 2023 and is projected to reach a value of USD 135.29 billion by 2032.

- The growth of the power generation, transmission and control manufacturing market is being driven by the increasing demand for electricity due to urbanization, industrialization, and the digital economy.

- Based on the component type, the motors segment is growing at a high rate and is projected to dominate the market.

- On the basis of transmission type, the mechanical transmission segment is projected to swipe the largest market share.

- In terms of application, the industrial machinery segment is expected to dominate the market.

- Based on the end use, the manufacturing segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Power Generation, Transmission and Control Manufacturing Market: Dynamics

Key Growth Drivers:

- Rising Global Electricity Demand: Increasing population, urbanization, and industrialization worldwide are driving a continuous surge in electricity consumption, necessitating expansion and modernization of power infrastructure.

- Transition to Renewable Energy Sources: The global shift towards cleaner energy sources like solar, wind, and hydro power requires significant investments in new generation facilities and grid infrastructure to integrate these variable resources.

- Aging Power Infrastructure in Developed Nations: Many developed countries have aging power generation and transmission infrastructure that needs to be replaced or upgraded to ensure reliability and efficiency.

- Government Investments and Policies: Supportive government policies, incentives, and regulations promoting renewable energy, grid modernization, and energy security are driving investments in this sector.

- Technological Advancements: Innovations in power generation technologies (e.g., advanced turbines, nuclear reactors), transmission systems (e.g., HVDC, FACTS), and control systems (e.g., smart grids, digital substations) are fueling market growth.

Restraints:

- High Capital Costs and Long Project Lead Times: Power infrastructure projects, especially for generation and transmission, involve substantial upfront investments and can have lengthy planning, permitting, and construction timelines.

- Environmental Regulations and Permitting Challenges: Stringent environmental regulations and the often complex and time-consuming permitting processes can delay or hinder the development of new power infrastructure projects.

- Intermittency of Renewable Energy Sources: The variable nature of solar and wind power generation poses challenges for grid stability and requires investments in energy storage and advanced grid management solutions.

- Grid Security and Cybersecurity Concerns: The increasing digitalization of power grids makes them more vulnerable to cyberattacks, necessitating significant investments in cybersecurity measures.

- Economic Uncertainty and Financing Constraints: Economic downturns and uncertainties in financial markets can impact investment decisions and the availability of financing for large-scale power infrastructure projects.

Opportunities:

- Development of Smart Grid Technologies: The modernization of power grids with smart grid technologies, including advanced metering infrastructure, digital substations, and grid automation systems, offers significant growth opportunities for manufacturers.

- Expansion of Energy Storage Solutions: The increasing need to integrate intermittent renewable energy sources is driving demand for various energy storage technologies (e.g., batteries, pumped hydro) and their associated manufacturing.

- Growth in Distributed Generation and Microgrids: The rise of distributed generation (e.g., rooftop solar, on-site power plants) and microgrids creates opportunities for manufacturers of smaller-scale power generation and control equipment.

- Focus on Energy Efficiency and Grid Modernization: Investments in upgrading existing grids with more efficient equipment and advanced transmission technologies (like HVDC) present significant market opportunities.

- Decarbonization and Carbon Capture Technologies: The growing emphasis on reducing carbon emissions is driving research, development, and deployment of carbon capture and storage technologies, creating new manufacturing opportunities.

Challenges:

- Integrating Renewable Energy Sources into the Grid: Managing the variability and intermittency of renewable energy and ensuring grid stability requires significant technological and infrastructure upgrades.

- Ensuring Grid Reliability and Resilience: Maintaining a reliable and resilient power supply in the face of increasing demand, extreme weather events, and cyber threats is a constant challenge.

- Managing the Transition from Fossil Fuels: The shift away from traditional fossil fuel-based power generation requires careful planning, investment in new technologies, and management of stranded assets.

- Addressing Public Acceptance and NIMBYism: Public opposition to new power infrastructure projects (e.g., transmission lines, wind farms) can create significant challenges for development.

- Keeping Pace with Rapid Technological Advancements: The power sector is undergoing rapid technological change, requiring manufacturers to continuously innovate and adapt their products and services.

Power Generation, Transmission And Control Manufacturing Market: Report Scope

This report thoroughly analyzes the Power Generation, Transmission And Control Manufacturing Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Power Generation, Transmission And Control Manufacturing Market |

| Market Size in 2023 | USD 94.24 Billion |

| Market Forecast in 2032 | USD 135.29 Billion |

| Growth Rate | CAGR of 4.1% |

| Number of Pages | 175 |

| Key Companies Covered | Mitsubishi Electric, CurtissWright, Yaskawa Electric, Siemens, Bosch Rexroth, Moog, Platinum Equity, Rockwell Automation, Schneider Electric, Honeywell, ABB, 3M, Baldor Electric, Parker Hannifin, General Electric, Eaton |

| Segments Covered | By Component Type, By Transmission Type, By Application, By End Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Power Generation, Transmission and Control Manufacturing Market: Segmentation Insights

The global power generation, transmission and control manufacturing market is divided by component type, transmission type, application, end use, and region.

Segmentation Insights by Component Type

Based on component type, the global power generation, transmission and control manufacturing market is divided into gearbox, motor, hydraulic systems, pneumatic systems, and sensors.

In the power generation, transmission, and control manufacturing market, motors represent the most dominant component type. Motors are fundamental to virtually every industrial and energy system, converting electrical energy into mechanical motion to drive equipment and machinery. Their widespread use across industries such as manufacturing, utilities, HVAC systems, and renewable energy—particularly in wind turbines and hydroelectric systems—cements their leading position. Technological advancements in electric motors, such as higher efficiency models and integration with smart control systems, have further enhanced their appeal.

Gearboxes follow closely as the next major segment. Gearboxes are critical for adjusting the speed and torque between mechanical systems, particularly in wind turbines, industrial automation, and heavy machinery. The demand for gear-driven solutions remains strong in applications that require precision and power management, contributing to their substantial market share.

Hydraulic systems are the third most significant component. These systems use pressurized fluids to transmit power, offering high force and control in applications like construction equipment, aerospace, and industrial machinery. Though often heavier and more maintenance-intensive than electric alternatives, hydraulic systems remain indispensable in scenarios requiring robust and reliable power transmission.

Pneumatic systems come next. These systems, which use compressed air for mechanical motion, are favored for their simplicity, cleanliness, and low cost, especially in industries such as packaging, food processing, and material handling. However, their relatively lower force output compared to hydraulic systems limits their application to lighter-duty operations, resulting in a smaller market share.

Sensors constitute the smallest segment among the component types. Despite their essential role in modernizing and optimizing power systems—enabling predictive maintenance, real-time monitoring, and automation—sensors are typically lower in cost and used in smaller volumes compared to motors or gearboxes. Nonetheless, their importance is rising rapidly with the shift toward smart manufacturing and Industry 4.0 initiatives.

Segmentation Insights by Transmission Type

On the basis of transmission type, the global power generation, transmission and control manufacturing market is bifurcated into mechanical transmission, electrical transmission, hydraulic transmission, and pneumatic transmission.

In the power generation, transmission, and control manufacturing market, mechanical transmission stands as the most dominant transmission type. It involves the use of gears, shafts, clutches, and belts to transmit motion and force, offering robust and reliable performance in various heavy-duty applications. Mechanical transmission is favored in industries such as automotive, construction, and manufacturing due to its efficiency in torque conversion and the ability to operate under harsh conditions with relatively low maintenance when properly designed.

Electrical transmission follows as the second most dominant segment. It involves the transfer of power through electrical systems, often using motors, generators, and power converters. This type is increasingly favored in energy-efficient and environmentally friendly applications, including electric vehicles and renewable energy systems. The shift toward electrification and the growing popularity of smart grids and automation are fueling the expansion of electrical transmission systems across multiple sectors.

Hydraulic transmission comes next in significance. This method transmits power using pressurized fluid, delivering high force and precision control. It is widely used in applications requiring significant power density and precise motion control, such as in aerospace, heavy machinery, and marine systems. However, its complexity, maintenance needs, and environmental concerns related to fluid leakage can limit its broader adoption.

Pneumatic transmission is the least dominant among the transmission types. It utilizes compressed air to transfer power and is primarily used in light-duty applications that prioritize speed and cleanliness over force—such as food processing, packaging, and small-scale automation. Despite its simplicity and safety benefits, its lower energy efficiency and limited force output restrict its use in more demanding industrial scenarios.

Segmentation Insights by Application

Based on application, the global power generation, transmission and control manufacturing market is divided into industrial machinery, automotive, aerospace, marine, and agriculture.

In the power generation, transmission, and control manufacturing market, industrial machinery represents the most dominant application segment. This dominance is driven by the widespread use of mechanical, electrical, hydraulic, and pneumatic systems in manufacturing processes, automation equipment, robotics, and heavy machinery. The need for high-performance components that ensure operational efficiency, productivity, and reliability makes this segment a key consumer of power transmission and control technologies across sectors like mining, construction, and production lines.

Automotive is the second leading application segment. Vehicles rely heavily on transmission and control systems for movement, power distribution, and performance optimization. From electric motors and gearboxes to sensor-based control units and braking systems, these components are essential for both traditional internal combustion engines and the growing fleet of electric vehicles. Innovations in electric drivetrains and autonomous vehicle technologies continue to boost demand in this sector.

Aerospace follows as the next major application area. Though smaller in volume compared to industrial and automotive sectors, aerospace demands high-precision, high-performance transmission systems that can operate under extreme conditions. Components such as hydraulic actuators, lightweight gear systems, and advanced control units are critical in aircraft operations, contributing significantly to the market due to their high value and performance requirements.

Marine applications rank next, utilizing robust transmission and control systems for propulsion, steering, and onboard power management. These systems must withstand corrosive environments and offer long-term reliability, making them essential in both commercial and defense maritime vessels. Although niche, the marine sector commands substantial investment in specialized equipment.

Agriculture is the least dominant application segment in this market. While tractors, harvesters, and irrigation systems depend on hydraulic and mechanical transmission components, the overall market size is smaller due to lower volume and spending compared to industrial or automotive sectors. However, the trend toward smart farming and mechanization in developing regions is gradually expanding its role in the market.

Segmentation Insights by End Use

On the basis of end use, the global power generation, transmission and control manufacturing market is bifurcated into manufacturing, construction, energy, transportation, and mining.

In the power generation, transmission, and control manufacturing market, manufacturing is the most dominant end-use segment. This sector relies heavily on precise and efficient power transmission systems to operate assembly lines, robotic systems, conveyors, and automated machinery. The drive for operational efficiency, process automation, and production scalability across diverse manufacturing industries—ranging from electronics to heavy equipment—fuels consistent demand for motors, gearboxes, sensors, and control systems.

Construction is the second most significant end-use segment. Power transmission and control systems are central to the performance of heavy construction equipment such as cranes, excavators, bulldozers, and loaders. These machines require robust hydraulic and mechanical transmission systems to handle rigorous tasks and harsh environments. With ongoing infrastructure development worldwide, especially in emerging markets, the demand in this segment remains strong.

Energy ranks third, with critical applications in both conventional and renewable power generation. From turbines and generators to control systems in wind, hydro, and solar plants, the sector depends on efficient power transmission and monitoring equipment. As global energy systems evolve toward decarbonization and smarter grids, there's growing investment in high-efficiency electric transmission and control technologies within this segment.

Transportation follows, encompassing railway systems, electric buses, and other public or commercial transport networks. Power transmission and control systems are vital for drive trains, braking systems, and operational control in these vehicles. While this segment is not as large as manufacturing or construction, it is growing steadily, particularly with the shift toward electric and smart transport solutions.

Mining is the least dominant end-use segment, though it requires rugged and powerful transmission systems for drills, conveyors, crushers, and underground vehicles. The need for high torque, durability, and reliability under extreme conditions keeps this segment relevant, but it is limited by the cyclical nature of the mining industry and the relatively smaller scale compared to broader industrial use.

Power Generation, Transmission and Control Manufacturing Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific is the most dominant region in the power generation, transmission, and control manufacturing market. This dominance is fueled by rapid industrialization, urban expansion, and surging energy consumption across major countries such as China, India, and Southeast Asian nations. Governments are heavily investing in upgrading and expanding power infrastructure, particularly in renewable energy and smart grid technologies. China leads with massive capacity in wind and solar energy, while India continues to expand its transmission network to support rising electricity demand. The region's strong manufacturing base and policy support further reinforce its leadership in the global market.

North America follows as a key market, driven by ongoing upgrades to aging energy infrastructure and strong regulatory focus on modernizing the power grid. The United States and Canada are embracing smart grid technology, automation, and renewable energy integration to enhance efficiency and reliability. A shift toward decarbonization and improved energy management also supports the demand for advanced power generation and control systems. Despite occasional budget constraints, the market continues to grow due to technology-driven modernization and infrastructure replacement initiatives.

Europe represents a significant regional market, strongly supported by its ambitious climate targets and investments in clean energy transition. Countries across Western and Northern Europe are modernizing grid infrastructure and focusing on decentralized energy systems, with high adoption of digital technologies and automation. The European Union’s push toward carbon neutrality encourages continued innovation and efficiency in power transmission and control manufacturing. However, disparities in progress among countries due to economic and policy differences create a mixed growth landscape.

Latin America is witnessing gradual development in power generation, transmission and control manufacturing market, supported by economic growth, urbanization, and a rising need to improve power reliability. Brazil and Argentina are making efforts to upgrade and expand their electrical networks, particularly in underserved regions. While the region faces challenges such as inconsistent policy frameworks, economic instability, and logistical hurdles, increasing investment in renewable energy and grid modernization is unlocking new growth opportunities.

Middle East and Africa are at an earlier stage of market development but show considerable potential due to growing energy needs and infrastructure development. Countries in the Middle East are pursuing strategic energy reforms, with increased investment in renewable energy and modern grid technologies. In Africa, electrification efforts and power system upgrades are gradually improving access and efficiency. Although economic and political challenges exist, the region’s focus on energy diversification and sustainability paves the way for long-term market growth.

Power Generation, Transmission and Control Manufacturing Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the power generation, transmission and control manufacturing market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global power generation, transmission and control manufacturing market include:

- Mitsubishi Electric

- CurtissWright

- Yaskawa Electric

- Siemens

- Bosch Rexroth

- Moog

- Platinum Equity

- Rockwell Automation

- Schneider Electric

- Honeywell

- ABB

- 3M

- Baldor Electric

- Parker Hannifin

- General Electric

- Eaton

The global power generation, transmission and control manufacturing market is segmented as follows:

By Component Type

- Gearbox

- Motor

- Hydraulic Systems

- Pneumatic Systems

- Sensors

By Transmission Type

- Mechanical Transmission

- Electrical Transmission

- Hydraulic Transmission

- Pneumatic Transmission

By Application

- Industrial Machinery

- Automotive

- Aerospace

- Marine

- Agriculture

By End Use

- Manufacturing

- Construction

- Energy

- Transportation

- Mining

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

What will be the CAGR of the global Power Generation, Transmission And Control Manufacturing market?

Table Of Content

Inquiry For Buying

Power Generation, Transmission and Control Manufacturing

Request Sample

Power Generation, Transmission and Control Manufacturing