Production Halls Market Size, Share, and Trends Analysis Report

CAGR :

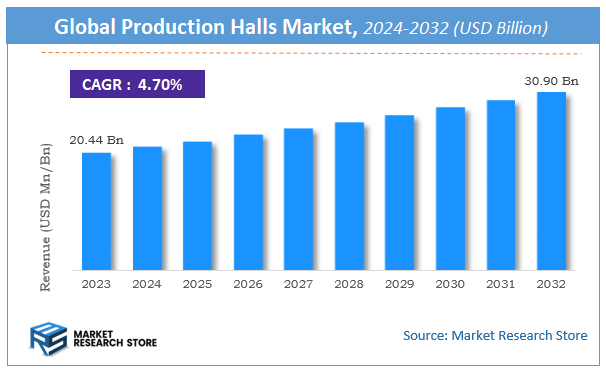

| Market Size 2023 (Base Year) | USD 20.44 Billion |

| Market Size 2032 (Forecast Year) | USD 30.90 Billion |

| CAGR | 4.7% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Production Halls Market Insights

According to Market Research Store, the global production halls market size was valued at around USD 20.44 billion in 2023 and is estimated to reach USD 30.90 billion by 2032, to register a CAGR of approximately 4.7% in terms of revenue during the forecast period 2024-2032.

The production halls report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Production Halls Market: Overview

Production halls are expansive, open-span buildings primarily designed to facilitate industrial manufacturing processes. These structures are essential for various sectors, including automotive, aerospace, food processing, and logistics, as they provide the necessary space for operations such as assembly, packaging, and storage. The demand for production halls is growing due to the increasing need for flexible and scalable manufacturing spaces. Key players in the market offer diverse solutions, ranging from pre-engineered metal buildings to modular structures that can be customized to meet specific requirements. As industries continue to evolve, production halls are also being designed to support advanced technologies like robotics, AI, and the Internet of Things (IoT), reflecting the shift towards more automated and data-driven manufacturing processes.

Key Highlights

- The production halls market is anticipated to grow at a CAGR of 4.7% during the forecast period.

- The global production halls market was estimated to be worth approximately USD 20.44 billion in 2023 and is projected to reach a value of USD 30.90 billion by 2032.

- The growth of the production halls market is being driven by increasing demand for automated and scalable manufacturing spaces, and the growth of sectors like automotive, aerospace, electronics, and pharmaceuticals.

- Based on the type of production hall, the manufacturing halls segment is growing at a high rate and is projected to dominate the market.

- On the basis of industry application, the aerospace & defense segment is projected to swipe the largest market share.

- In terms of size of production hall, the large (> 50,000 sq. ft.) segment is expected to dominate the market.

- Based on the construction type, the pre-engineered steel buildings segment is expected to dominate the market.

- In terms of level of automation, the fully automated segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Production Halls Market: Dynamics

Key Growth Drivers:

- Increasing Industrialization and Manufacturing Activities: As industries like automotive, electronics, and consumer goods expand, the demand for efficient production halls grows to accommodate larger manufacturing operations.

- Automation and Smart Factory Initiatives: The adoption of Industry 4.0 technologies, including automation, robotics, and IoT, is driving the need for modern production halls equipped with advanced systems to support these technologies.

- Rising Demand for Custom-Built Facilities: Companies are increasingly seeking production halls tailored to their specific needs, such as advanced climate control, specialized machinery, or efficient layout for mass production.

- Global Supply Chain Expansion: As global supply chains continue to grow, businesses are building larger, more flexible production halls to meet increasing demand for manufacturing and warehousing space.

- Cost-Effective and Scalable Solutions: The need for scalable production capabilities and cost-efficient manufacturing is prompting the construction of adaptable production halls that can be expanded as needed.

Restraints:

- High Capital Investment for Construction and Maintenance: The upfront costs associated with constructing large-scale production halls can be significant, limiting investments from smaller businesses or companies with constrained budgets.

- Regulatory and Environmental Constraints: Zoning laws, building codes, and environmental regulations can impose limitations on where and how production halls can be built, creating challenges for expansion.

- Space Limitations in Urban Areas: In densely populated urban centers, there is limited availability of space to construct new production halls, which can hinder expansion and lead to higher land acquisition costs.

- Longer Timeframes for Construction and Setup: The time required to build and equip production halls can delay operations, leading to potential revenue loss and operational inefficiency during the transition.

Opportunities:

- Adoption of Green Building Practices and Sustainability Trends: The push toward environmentally friendly and energy-efficient production halls presents opportunities for construction companies to provide sustainable solutions that reduce operating costs and appeal to eco-conscious companies.

- Expanding Manufacturing in Developing Economies: As manufacturing continues to grow in emerging markets, especially in regions like Asia-Pacific, Africa, and Latin America, there is an increasing demand for new production halls tailored to local needs.

- Integration of AI, Robotics, and Automation: The integration of advanced technologies like AI, machine learning, and robotics into production processes provides opportunities for businesses to modernize their facilities and enhance operational efficiency.

- Customization and Modular Construction: Offering customizable and modular production hall solutions allows companies to build flexible and scalable facilities that meet specific manufacturing needs and can evolve as businesses grow.

Challenges:

- Increased Competition in the Construction Sector: As the demand for production halls grows, there is an increasing number of construction companies entering the market, leading to heightened competition and price pressure.

- Supply Chain Disruptions in Construction Materials: Global supply chain issues, such as shortages in steel or other critical construction materials, can delay construction timelines and increase costs for building production halls.

- Technological Complexity and Integration Issues: Integrating new technologies such as automation, robotics, and smart factory systems into production halls can be complex and require skilled professionals, leading to potential delays and higher costs.

- Labor Shortages and Skills Gaps: A lack of skilled labor in the construction and manufacturing sectors can hinder the timely completion of production halls and impact the ability to maintain and operate advanced facilities effectively.

Production Halls Market: Report Scope

This report thoroughly analyzes the Production Halls Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Production Halls Market |

| Market Size in 2023 | USD 20.44 Billion |

| Market Forecast in 2032 | USD 30.90 Billion |

| Growth Rate | CAGR of 4.7% |

| Number of Pages | 178 |

| Key Companies Covered | Astron Buildings, Frisomat, Borga, Althoff, Ocmer, Commercecon, SEA, GAJ-STAL, FEMONT OPAVA, Schwarzmann, Best-Hall |

| Segments Covered | By Type of Production Hall, By Industry Application, By Size of Production Hall, By Construction Type, By Level of Automation, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Production Halls Market: Segmentation Insights

The global production halls market is divided by type of production hall, industry application, size of production hall, construction type, level of automation, and region.

Segmentation Insights by Type of Production Hall

Based on type of production hall, the global production halls market is divided into manufacturing halls, assembly halls, distribution halls, and research & development halls.

In the production halls market, the most dominant segment is Manufacturing Halls. These halls are the backbone of industrial production, as they house the primary operations where raw materials are transformed into finished goods. Manufacturing halls are typically designed with large spaces to accommodate heavy machinery, production lines, and automated systems, which make them crucial for mass production in industries such as automotive, electronics, and consumer goods. The need for large-scale production, efficient workflows, and supply chain integration makes manufacturing halls the leading segment in the production halls market.

Next, Assembly Halls rank as the second-most dominant segment. Assembly halls are used for the final stages of production, where individual components or subassemblies are brought together to create the finished product. These halls are essential in industries like electronics, automotive, and aerospace, where precise assembly processes are critical. The growth of industries focusing on complex, high-tech products has fueled the demand for assembly halls. As companies push for faster time-to-market and greater customization, assembly halls play a vital role in ensuring efficient and accurate assembly processes.

Distribution Halls come third in dominance. These facilities are designed to store and distribute finished goods to various locations, either directly to consumers or to wholesalers and retailers. Distribution halls are pivotal in logistics and supply chain operations. While not as integral to the production process as manufacturing or assembly halls, their importance in the global trade and e-commerce boom has driven their growth, especially with the increasing reliance on fast, efficient delivery systems. The demand for distribution centers has surged in industries such as retail, e-commerce, and food distribution.

Lastly, Research & Development (R&D) Halls are the least dominant segment in the market. These halls are used for the development of new products, processes, or innovations. While crucial for industries such as pharmaceuticals, technology, and aerospace, R&D halls represent a smaller portion of the overall production hall market. This is primarily because their function is more specialized, and they are used in industries that prioritize innovation and product testing over mass production. However, as industries continue to focus on technological advancements and innovation, the need for R&D facilities is expected to grow, albeit at a slower pace compared to manufacturing and assembly halls.

Segmentation Insights by Industry Application

On the basis of industry application, the global production halls market is bifurcated into aerospace & defense, automotive, electronics, food & beverage, textiles, and pharmaceuticals.

In the production halls market, Aerospace & Defense is the most dominant industry application. The aerospace and defense sector relies heavily on highly specialized production facilities, which often include manufacturing and assembly halls, to meet the stringent demands of producing advanced components, such as aircraft parts, defense systems, and spacecraft. These facilities require precision, quality control, and the ability to handle high-value, complex components. The growth in defense spending and the increasing demand for commercial aircraft are significant drivers of the demand for production halls in this industry.

Automotive follows closely behind as the second-most dominant sector. The automotive industry requires large-scale manufacturing halls for the production of vehicles and components, along with assembly halls for final vehicle assembly. As the demand for electric vehicles (EVs) and smart automotive systems increases, the automotive industry continues to invest in state-of-the-art production halls to support the manufacturing and assembly of next-generation vehicles. The automotive sector’s need for high efficiency, automation, and large-scale operations solidifies its position as one of the leading users of production halls.

Next in dominance is the Electronics industry, which is also a major user of production halls, particularly for the manufacturing of electronic devices and components such as semiconductors, circuit boards, and consumer electronics. The growth in demand for smartphones, wearables, and other consumer electronics, as well as the need for sophisticated manufacturing processes, makes the electronics industry a key application for production halls. These halls support high-tech manufacturing lines that ensure precision and efficiency, especially in industries where technology changes rapidly.

The Food & Beverage industry is another significant application for production halls, though it ranks lower than the previous industries. Food and beverage manufacturing often requires specialized production halls for the processing, packaging, and distribution of products. These facilities need to meet stringent food safety and regulatory standards, which make them specialized in design and function. The growing demand for processed food products, along with increased focus on efficiency and automation in the food industry, contributes to the rising demand for production halls.

Textiles is a moderate player in the production halls market. Textile manufacturing requires production halls for fabric production, dyeing, and garment assembly. While this industry has traditionally been labor-intensive, modern textile production has increasingly shifted toward automation and large-scale operations, driving demand for production halls. However, its growth is somewhat slower than that of the aerospace, automotive, and electronics sectors, as the textile industry faces challenges related to price competition and globalization.

Lastly, Pharmaceuticals is the least dominant industry in the production halls market. While the pharmaceutical industry is essential, it is a more specialized sector that requires production halls focused on the manufacture of medicines, vaccines, and other health products. These facilities must comply with strict regulations and standards, often requiring clean rooms, advanced automation, and precision equipment. Although the pharmaceutical industry is expected to grow, particularly with the ongoing advancements in biotechnology and personalized medicine, it still represents a smaller portion of the production halls market compared to aerospace & defense, automotive, and electronics.

Segmentation Insights by Size of Production Hall

Based on size of production hall, the global production halls market is divided into small (< 10,000 sq. ft.), medium (10,000 - 50,000 sq. ft.), and large (> 50,000 sq. ft.).

In the production halls market, the largest segment is Large Production Halls (> 50,000 sq. ft.). These spaces are essential for industries requiring high-volume, large-scale production processes, such as aerospace, automotive, and electronics. Large production halls accommodate heavy machinery, assembly lines, and automated systems that allow for mass production. These facilities are also required in industries that produce bulky or complex products, where space is critical for the efficient flow of materials and products. The demand for larger production halls continues to rise as industries seek to increase manufacturing capacity and optimize operational efficiency.

Medium Production Halls (10,000 - 50,000 sq. ft.) come next in dominance. These production halls are typically used by industries that need substantial space for production but not on the same massive scale as those requiring large halls. Sectors such as food and beverage, textiles, and some electronics manufacturing commonly utilize medium-sized production halls. These halls offer enough space to house specialized equipment and processes without the vast footprint of larger facilities. The increasing trend toward automation and more efficient use of space in production processes helps drive the demand for medium-sized halls, particularly in sectors that require flexibility and moderate output volumes.

The Small Production Halls (< 10,000 sq. ft.) represent the smallest segment of the market. These spaces are often used for more specialized, low-volume production runs or small businesses that focus on niche products. Small production halls are commonly found in industries such as small-scale electronics manufacturing, specialized pharmaceuticals, and custom products in sectors like textiles. While they are essential for specific, specialized applications, the overall demand for small production halls is comparatively lower due to the industry’s increasing preference for larger, more efficient facilities capable of handling high-volume production. However, they remain important in industries focused on innovation, prototyping, and limited production runs.

Segmentation Insights by Construction Type

On the basis of construction type, the global production halls market is bifurcated into pre-engineered steel buildings, concrete structures, and modular buildings.

In the production halls market, Pre-engineered Steel Buildings are the most dominant segment in terms of construction type. These structures are widely used due to their cost-effectiveness, speed of construction, and flexibility. Pre-engineered steel buildings are highly customizable and can accommodate various types of production processes, from light manufacturing to heavy industrial use. Their durability and ability to withstand harsh environmental conditions make them particularly popular in industries such as automotive, aerospace, and electronics. The growing trend of modular construction and the demand for quick setups for expanding production facilities contribute to the dominance of pre-engineered steel buildings in the market.

Concrete Structures are the second-most dominant construction type for production halls. Concrete is a robust, fire-resistant material that is ideal for large, heavy-duty production facilities requiring enhanced structural integrity. These buildings are commonly used in industries like food and beverage, pharmaceuticals, and manufacturing, where high-strength, permanent buildings are essential. Concrete structures can support heavy machinery, offer better thermal mass, and provide enhanced safety in terms of fire protection and durability. The increased demand for long-term, low-maintenance facilities contributes to the growth of concrete production halls, particularly in industries with stringent regulatory requirements, such as pharmaceuticals and food processing.

Lastly, Modular Buildings are the least dominant but growing in popularity. These are prefabricated structures that can be easily assembled and disassembled, making them ideal for companies looking for flexible, scalable solutions. Modular buildings are commonly used in industries where short-term or temporary production facilities are needed, such as in research and development, pilot projects, or in areas where production volumes fluctuate. The modular nature of these buildings also makes them useful in settings where expansion is expected, as they can be easily reconfigured or extended. However, despite their growing appeal, modular buildings still represent a smaller portion of the market compared to pre-engineered steel buildings and concrete structures due to their more limited use for large-scale, long-term production operations.

Segmentation Insights by Level of Automation

On the basis of level of automation, the global production halls market is bifurcated into fully automated and semi-automated, manual.

In the production halls market, the Fully Automated segment is the most dominant when it comes to the level of automation. Fully automated production halls are designed with high-tech machinery, robots, and computer systems that handle the majority of manufacturing tasks with minimal human intervention. These facilities are prevalent in industries like automotive, electronics, and aerospace, where high precision, consistency, and scalability are crucial. The growing need for efficiency, cost reduction, and the ability to produce high volumes quickly drives the adoption of fully automated production halls. The advancement of technologies such as Artificial Intelligence (AI), Internet of Things (IoT), and robotics has made fully automated production halls increasingly affordable and reliable, further enhancing their dominance in the market.

Semi-Automated production halls come next in dominance. These facilities combine both manual labor and automated systems to perform various tasks. Semi-automation is commonly used in industries that require flexibility, such as food and beverage manufacturing, textiles, and certain electronics manufacturing. These production halls offer a balance between automation and human involvement, enabling operators to control key processes while automated systems assist with repetitive, time-consuming tasks. Semi-automated production halls are beneficial for companies that need customization, smaller production runs, or are in the process of gradually transitioning to full automation. This level of automation provides a cost-effective solution for industries that do not yet need or cannot afford the full automation of their processes.

The Manual segment is the least dominant in the market, though still relevant in certain sectors. Manual production halls rely primarily on human labor for the majority of tasks, with minimal use of machinery. These types of production halls are typically used in smaller-scale operations, artisanal manufacturing, or specialized industries such as custom goods, repair shops, and small-scale electronics production. Manual operations are more common in industries where craftsmanship, attention to detail, or low-volume production is essential. However, as industries increasingly prioritize efficiency and scalability, the manual production hall segment continues to decline, particularly in large-scale, high-demand manufacturing environments.

Production Halls Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the production halls market, owing to its advanced manufacturing capabilities, high demand for automation, and technological innovation. The United States plays a key role, particularly in industries such as automotive, aerospace, and electronics, which require cutting-edge production facilities. The region's strong economic foundation and continuous investment in industrial expansion ensure it maintains a leadership position.

Europe follows closely, with major contributors like Germany, France, and the United Kingdom. The region’s well-established industrial base, coupled with a strong focus on sustainability and green technologies, propels the demand for modern and efficient production halls. The automotive, machinery, and food processing sectors are some of the primary drivers for industrial growth in Europe.

Asia Pacific is experiencing rapid market growth, primarily driven by the industrialization of countries such as China, India, and Southeast Asian nations. The region’s demand for production halls is largely fueled by electronics, textiles, and consumer goods manufacturing. As industrial infrastructure improves, Asia Pacific is expected to grow significantly, becoming a key player in the global market.

Latin America shows steady progress in the production halls market, led by countries like Brazil and Mexico. The automotive, food processing, and textiles industries are the main drivers of demand, though the region faces challenges such as economic instability and infrastructure constraints. Nonetheless, its growing industrial base presents significant opportunities for expansion.

Middle East is emerging as a growing market for production halls, with countries like Saudi Arabia and the UAE making strides in diversifying their economies. Investments in manufacturing sectors like chemicals, construction materials, and consumer goods are boosting demand for modern production facilities. This region’s continued push for economic diversification away from oil dependence contributes to its growth in the industrial sector.

Africa remains a relatively small market but holds potential for future growth. South Africa and Nigeria are among the leaders in industrial activities, with key sectors including food processing, textiles, and building materials. However, challenges such as limited infrastructure and economic instability can hinder growth, making the region’s industrial expansion more gradual compared to others.

Production Halls Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the production halls market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global production halls market include:

- Astron Buildings

- Frisomat

- Borga

- Althoff

- Ocmer

- Commercecon

- SEA

- GAJ-STAL

- FEMONT OPAVA

- Schwarzmann

- Best-Hall

The global production halls market is segmented as follows:

By Type of Production Hall

- Manufacturing Halls

- Assembly Halls

- Distribution Halls

- Research and Development Halls

By Industry Application

- Aerospace and Defense

- Automotive

- Electronics

- Food and Beverage

- Textiles

- Pharmaceuticals

By Size of Production Hall

- Small (< 10,000 sq. ft.)

- Medium (10,000 – 50,000 sq. ft.)

- Large (> 50000 sq. ft.)

By Construction Type

- Pre-engineered Steel Buildings

- Concrete Structures

- Modular Buildings

By Level of Automation

- Fully Automated

- Semi-Automated

- Manual

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Production Halls

Request Sample

Production Halls