Remote Control Wireless Module Market Size, Share, and Trends Analysis Report

CAGR :

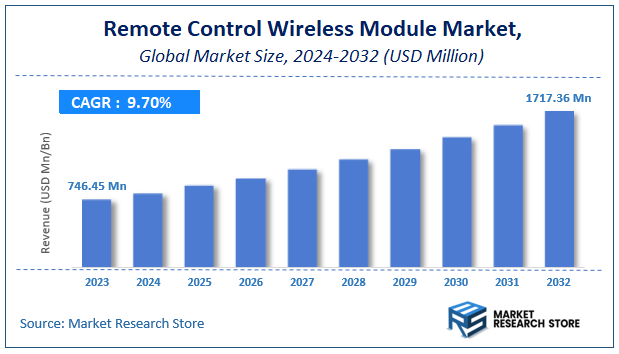

| Market Size 2023 (Base Year) | USD 746.45 Million |

| Market Size 2032 (Forecast Year) | USD 1717.36 Million |

| CAGR | 9.7% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Remote Control Wireless Module Market Insights

According to Market Research Store, the global remote control wireless module market size was valued at around USD 746.45 million in 2023 and is estimated to reach USD 1717.36 million by 2032, to register a CAGR of approximately 9.7% in terms of revenue during the forecast period 2024-2032.

The remote control wireless module report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Remote Control Wireless Module Market: Overview

A remote control wireless module is a compact electronic device that enables wireless communication between a remote control and an electronic system, typically using radio frequency (RF), Wi-Fi, Bluetooth, Zigbee, or other protocols. These modules are integrated into systems to facilitate remote operations such as turning devices on/off, adjusting settings, or triggering functions without direct physical contact. They are widely used in consumer electronics, smart home systems, industrial automation, medical devices, and automotive applications. Their functionality enhances convenience, flexibility, and automation in both personal and professional environments.

Key Highlights

- The remote control wireless module market is anticipated to grow at a CAGR of 9.7% during the forecast period.

- The global remote control wireless module market was estimated to be worth approximately USD 746.45 million in 2023 and is projected to reach a value of USD 1717.36 million by 2032.

- The growth of the remote control wireless module market is being driven by the increasing adoption of IoT devices, automation in industrial and home settings, and the rising demand for wireless connectivity across multiple sectors.

- Based on the technology, the Radio Frequency (RF) segment is growing at a high rate and is projected to dominate the market.

- On the basis of features, the multi-device control segment is projected to swipe the largest market share.

- In terms of power source, the battery-powered segment is expected to dominate the market.

- Based on the application, the consumer electronics segment is expected to dominate the market.

- In terms of end-user, the residential segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Remote Control Wireless Module Market: Dynamics

Key Growth Drivers:

- Increasing Adoption of Smart Home and IoT Devices: The rapid proliferation of smart home devices (lighting, thermostats, locks, etc.) and Internet of Things (IoT) applications necessitates wireless communication modules for remote control and data exchange, driving significant market growth.

- Growing Demand for Convenience and Automation: Consumers and industries increasingly seek convenience and automation in their daily lives and operations. Wireless remote control modules enable seamless control of various devices and systems from a distance, enhancing user experience and efficiency.

- Advancements in Wireless Communication Technologies: Ongoing advancements in wireless technologies like Bluetooth Low Energy (BLE), Wi-Fi, Zigbee, Z-Wave, and sub-GHz protocols offer a range of options for remote control applications, each with its own advantages in terms of range, power consumption, and data rate, thus expanding the market.

- Rising Demand in Automotive and Industrial Sectors: Wireless remote control modules are increasingly used in automotive applications (keyless entry, remote start, infotainment control) and industrial settings (remote machinery control, robotics, data acquisition), contributing to market expansion.

Restraints:

- Security Vulnerabilities and Interoperability Issues: Wireless communication can be susceptible to security breaches and hacking attempts. Ensuring robust security protocols and addressing interoperability challenges between different wireless standards and devices are crucial restraints.

- Power Consumption Limitations: For battery-powered remote control devices, minimizing power consumption of the wireless module is critical for extending battery life. This constraint can limit the choice of wireless technology and the complexity of functionalities.

- Range Limitations and Signal Interference: The effective communication range of wireless modules can be limited by the chosen technology and environmental factors like obstacles and electromagnetic interference. This can restrict the applicability in certain scenarios.

- Cost Sensitivity in Consumer Electronics: The remote control functionality is often integrated into mass-market consumer electronics where cost is a significant factor. This puts pressure on wireless module manufacturers to offer cost-effective solutions.

Opportunities:

- Development of Ultra-Low Power Wireless Technologies: The increasing demand for energy-efficient devices is driving the development of ultra-low power wireless communication modules, opening up new possibilities for battery-operated remote controls and IoT sensors with extended lifespans.

- Integration of Multiple Wireless Protocols: Modules that support multiple wireless protocols (e.g., Bluetooth and Wi-Fi) offer greater flexibility and interoperability, catering to a wider range of applications and ecosystems.

- Focus on Enhanced Security Features: Developing wireless modules with advanced security features like end-to-end encryption and secure authentication mechanisms is crucial for building trust and enabling wider adoption in security-sensitive applications.

- Miniaturization and System-on-Module (SoM) Integration: The trend towards smaller and more integrated electronic devices creates opportunities for highly miniaturized wireless modules and SoM solutions that simplify design and reduce the overall footprint.

- Growing Demand for Long-Range and Low-Power Wide Area Network (LPWAN) Technologies: LPWAN technologies like LoRaWAN and NB-IoT are gaining traction for long-range remote control and monitoring applications in smart cities, agriculture, and industrial IoT, creating new market opportunities for suitable wireless modules.

Challenges:

- Ensuring Reliable Communication in Diverse Environments: Wireless modules need to provide reliable communication in various and often challenging environments with potential interference, obstacles, and varying signal strengths.

- Managing Coexistence of Multiple Wireless Technologies: With the increasing number of wireless devices operating in the same frequency bands, managing coexistence and minimizing interference between different technologies (e.g., Wi-Fi, Bluetooth, Zigbee) is a growing challenge.

- Keeping Up with Evolving Wireless Standards: The landscape of wireless communication standards is constantly evolving. Module manufacturers need to continuously adapt their products to support the latest standards and ensure future compatibility.

- Simplifying Integration and Development for End-Users: Making it easier for developers and manufacturers to integrate wireless modules into their products through comprehensive documentation, development kits, and software support is crucial for wider adoption.

- Addressing Regulatory Compliance and Certification: Wireless modules need to comply with various regional and international regulatory requirements and undergo certification processes, which can be time-consuming and costly.

- Maintaining Cost Competitiveness While Adding Features: Balancing the need to offer advanced features and high performance with the price sensitivity of many applications remains a significant challenge for wireless module manufacturers.

Remote Control Wireless Module Market: Report Scope

This report thoroughly analyzes the Remote Control Wireless Module Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Remote Control Wireless Module Market |

| Market Size in 2023 | USD 746.45 Million |

| Market Forecast in 2032 | USD 1717.36 Million |

| Growth Rate | CAGR of 9.7% |

| Number of Pages | 177 |

| Key Companies Covered | Sierra Wireless, Gemalto (Thales Group), Quectel, Telit, Huawei, Sunsea Group, LG Innotek, U-blox, Fibocom wireless Inc., Neoway |

| Segments Covered | By Technology, By Features, By Power Source, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Remote Control Wireless Module Market: Segmentation Insights

The global remote control wireless module market is divided by technology, features, power source, application, end-user, and region.

Segmentation Insights by Technology

Based on technology, the global remote control wireless module market is divided into radio frequency (RF), infrared (IR), bluetooth, wi-fi, and zigbee.

In the remote control wireless module market, the Radio Frequency (RF) segment emerges as the most dominant technology due to its broad adoption across a wide range of consumer electronics, home automation devices, and industrial applications. RF-based modules are favored for their ability to function through walls and at relatively long distances without the need for direct line-of-sight, making them ideal for television remotes, garage door openers, and various IoT-enabled appliances. Their low cost, robust performance, and widespread compatibility further bolster their market share.

Following RF, Infrared (IR) technology holds a significant share, primarily due to its longstanding use in traditional remote control devices such as televisions, DVD players, and air conditioning units. IR modules are simple, low-power, and cost-effective, but their need for line-of-sight and limited range restricts their application compared to RF.

Next in line is Bluetooth technology, which is increasingly being integrated into smart home systems, wearable devices, and mobile-controlled appliances. Bluetooth offers a good balance between range, power consumption, and ease of connectivity, particularly with smartphones and tablets. The emergence of Bluetooth Low Energy (BLE) has also enhanced its suitability for battery-operated devices, although it still lags behind RF and IR in terms of legacy system integration.

Wi-Fi based remote control modules are gaining momentum due to the growth of smart home ecosystems and the proliferation of Wi-Fi-enabled devices. These modules provide high data transmission rates and internet connectivity, enabling control from virtually anywhere. However, higher power consumption and more complex integration processes make Wi-Fi modules less ideal for simpler or battery-powered remote control applications.

At the lower end of the dominance spectrum is Zigbee, a mesh-networking protocol that is particularly suited for low-power, low-data-rate applications in smart homes and industrial automation. While Zigbee offers excellent scalability and energy efficiency, its market penetration is more niche, mainly limited to specific smart home brands and devices requiring networked communication, which constrains its broader adoption.

Segmentation Insights by Features

On the basis of features, the global remote control wireless module market is bifurcated into programmable, customizable, multi-device control, voice control, and mobile app integration.

In the remote control wireless module market by features, Multi-Device Control stands out as the most dominant segment. This feature has become a staple in modern remote control systems, especially with the rise of smart homes and interconnected devices. Consumers increasingly demand the convenience of controlling multiple appliances—such as TVs, sound systems, air conditioners, and lighting—using a single remote or interface. This capability reduces clutter and enhances user experience, making it highly attractive for both residential and commercial applications.

Closely following is the Programmable segment. Programmable remote control modules allow users to configure specific functions, sequences, or macros tailored to their needs. This feature is particularly valued in universal remotes and automation setups, where users want to streamline complex tasks (e.g., turning on the TV, adjusting the lights, and powering the sound system with one button). Its flexibility and personalization appeal make it widely adopted across tech-savvy consumer groups.

Next is Mobile App Integration, which has seen a surge due to the proliferation of smartphones and the growing preference for remote operation via apps. This feature allows users to control devices through their mobile phones or tablets, providing convenience, portability, and often access to advanced settings. It is particularly popular in smart home systems, although its dependence on smartphone ecosystems and apps may limit universal adoption.

Voice Control is gaining popularity as smart assistants like Amazon Alexa, Google Assistant, and Apple Siri become more embedded in daily life. This feature offers hands-free convenience and is especially helpful for accessibility purposes. However, its reliance on voice recognition accuracy and internet connectivity slightly hinders its dominance compared to more universally functional features like Multi-Device Control or Programmable settings.

At the lower end of the adoption curve is the Customizable feature. While customization—such as assigning buttons, altering layouts, or modifying skins—offers user-friendly benefits, it is often considered a secondary or value-added feature rather than a core necessity. As a result, it is more common in premium or enthusiast-grade products, limiting its reach in the mainstream consumer market.

Segmentation Insights by Power Source

Based on power source, the global remote control wireless module market is divided into battery-powered, rechargeable, and wired.

In the remote control wireless module market by power source, Battery-Powered modules hold the dominant position. These modules are widely used across consumer electronics due to their simplicity, portability, and low power requirements. Devices like TV remotes, air conditioner remotes, and many smart home accessories rely on standard disposable batteries (such as AA or AAA) for convenience and cost-effectiveness. The ease of replacement and broad compatibility have made battery-powered modules the default choice for decades.

Rechargeable remote control modules follow as a growing segment, driven by environmental concerns and user preference for long-term cost savings. These modules typically use lithium-ion or lithium-polymer batteries and are commonly found in high-end universal remotes, gaming controllers, and some smart home hubs. They reduce battery waste and can be charged via USB or docking stations, which enhances user convenience. However, their higher upfront cost and limited availability in low-end products slightly temper their widespread adoption.

Wired modules represent the least dominant segment. While offering continuous power and zero maintenance related to charging or replacing batteries, their use is largely restricted to specialized industrial, commercial, or legacy systems. The lack of mobility and the inconvenience of physical connections make wired modules unsuitable for most consumer applications, particularly in the age of wireless convenience.

Segmentation Insights by Application

On the basis of application, the global remote control wireless module market is bifurcated into consumer electronics, automotive, industrial automation, healthcare, and security systems.

In the remote control wireless module market by application, Consumer Electronics is the most dominant segment, driven by the widespread use of wireless remotes in televisions, audio systems, air conditioners, and smart home devices. The sheer volume of consumer electronics sold globally, combined with the growing adoption of smart and interconnected devices, makes this segment the largest user of wireless modules. Convenience, affordability, and continual innovation in user interfaces—such as voice control and mobile integration—fuel demand in this category.

Next is the Automotive sector, which is rapidly integrating wireless modules for keyless entry systems, infotainment controls, remote engine start, and smart locking systems. As vehicles become increasingly connected and software-defined, the demand for wireless control technologies in both OEM and aftermarket products continues to rise. The push toward electric vehicles and autonomous driving has further accelerated the integration of advanced remote control modules.

Industrial Automation follows closely, as wireless modules are being adopted in factory settings for machine control, robotics, and process monitoring. These modules enable safer and more flexible control of industrial equipment, especially in hazardous or hard-to-reach environments. The growing trend of Industry 4.0 and IoT-driven manufacturing boosts the demand for robust and reliable wireless control systems.

The Healthcare sector, while smaller, is steadily growing in its use of wireless modules. Remote controls are integrated into patient monitoring systems, smart beds, diagnostic devices, and assistive technologies. With increasing demand for home-based care, telemedicine, and mobility aids, the need for secure, responsive wireless modules is expected to grow in medical applications.

Security Systems represent the least dominant, but still essential, segment. Wireless modules are used in remote surveillance cameras, access control systems, alarm controls, and smart locks. Although this segment is growing with the adoption of smart home security solutions, it is still comparatively smaller in scale than consumer electronics or automotive, partly due to the specialized nature and high-security requirements of these systems.

Segmentation Insights by End-User

On the basis of end-user, the global remote control wireless module market is bifurcated into residential, commercial, industrial, government, and healthcare providers.

In the remote control wireless module market by end-user, the Residential segment is the most dominant. This dominance is primarily driven by the widespread use of wireless remote controls in everyday household devices such as TVs, air conditioners, home automation systems, and smart lighting. The rising popularity of smart homes, powered by voice assistants and app-based controls, has significantly increased demand for wireless modules that offer seamless control and integration. Convenience, affordability, and the growing consumer focus on connected living continue to boost this segment.

Following residential use is the Commercial segment, which includes offices, retail spaces, hospitality, and entertainment venues. In these settings, wireless modules are commonly used for controlling lighting, AV systems, HVAC, security systems, and customer experience technologies like digital signage. The commercial sector values energy efficiency, user comfort, and centralized control, which wireless technologies support efficiently.

The Industrial segment ranks next, driven by the need for remote control in automation, machinery operation, and equipment diagnostics. Wireless modules help improve workplace safety, reduce downtime, and enable flexible system configurations in manufacturing plants and warehouses. While industrial applications are more niche and require robust, interference-resistant systems, they often demand higher reliability and performance than consumer-grade products.

Government usage of wireless remote modules, though smaller in scale, plays a crucial role in defense systems, public infrastructure management, and secure communication networks. Applications may include remote surveillance, traffic control systems, and emergency response equipment. However, strict security protocols and longer procurement cycles often limit rapid expansion in this sector.

Finally, Healthcare Providers represent the least dominant end-user segment but are gradually integrating wireless modules in hospital beds, patient monitoring systems, and assistive devices. With the increasing demand for remote care and the shift toward patient-centric healthcare, this segment is expected to grow steadily. However, stringent regulatory requirements and the critical nature of healthcare environments slow widespread adoption compared to residential or commercial sectors.

Remote Control Wireless Module Market: Regional Insights

- North America is expected to dominates the global market

The North America region is the most dominant in the remote control wireless module market. This dominance is primarily due to the high level of automation across key industries such as manufacturing, automotive, and construction. The presence of numerous leading technology firms and system integrators contributes to rapid innovation and deployment of wireless remote control solutions. Additionally, there is strong demand for advanced industrial safety systems and real-time operational control, further supported by widespread adoption of IoT and smart manufacturing frameworks. The United States plays a pivotal role in driving this growth, thanks to its robust industrial infrastructure and high investment in automation technologies.

Europe holds the second-largest market share, driven by its highly developed industrial sectors and strict regulatory requirements for safety and efficiency. Countries like Germany, the UK, and France are major contributors due to their leadership in industrial engineering and sustainable infrastructure. These nations are proactively integrating wireless remote modules into logistics, energy, and smart factory environments. The region’s commitment to digitization and energy efficiency continues to foster steady demand for wireless control systems in both industrial and commercial applications.

Asia Pacific is a fast-growing market, propelled by rapid industrialization and increasing investments in automation, particularly in countries such as China, Japan, South Korea, and India. Expanding urban populations and government initiatives to build smart cities have led to higher adoption of wireless remote control modules. The deployment of 5G networks and a surge in electronics manufacturing further fuel the region’s market expansion. Although not the largest, APAC is considered the most dynamic due to its high growth potential and increasing technological capability.

Latin America is an emerging market where growth is being supported by developments in agriculture, construction, and public infrastructure. Countries like Brazil and Mexico are gradually incorporating wireless control technologies to improve operational efficiency in heavy industries. Despite economic and political challenges, the region is witnessing increased interest in industrial automation, which is expected to drive demand for wireless modules over time.

Middle East and Africa is currently the least dominant region but is showing signs of gradual growth. Urban development projects, especially in the Gulf countries, are creating opportunities for smart infrastructure and remote industrial operations. The oil and gas sector is a significant adopter of wireless remote control systems due to the need for safe, efficient equipment handling. Though adoption remains limited compared to other regions, the growing emphasis on digitization and automation is likely to spur future market expansion.

Remote Control Wireless Module Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the remote control wireless module market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global remote control wireless module market include:

- Sierra Wireless

- Gemalto (Thales Group)

- Quectel

- Telit

- Huawei

- Sunsea Group

- LG Innotek

- U-blox

- Fibocom wireless Inc.

- Neoway

The global remote control wireless module market is segmented as follows:

By Technology

- Radio Frequency (RF)

- Infrared (IR)

- Bluetooth

- Wi-Fi

- Zigbee

By Features

- Programmable

- Customizable

- Multi-Device Control

- Voice Control

- Mobile App Integration

By Power Source

- Battery-Powered

- Rechargeable

- Wired

By Application

- Consumer Electronics

- Automotive

- Industrial Automation

- Healthcare

- Security Systems

By End-User

- Residential

- Commercial

- Industrial

- Government

- Healthcare Providers

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Remote Control Wireless Module

Request Sample

Remote Control Wireless Module