Retail Analytics Market Size, Share, and Trends Analysis Report

CAGR :

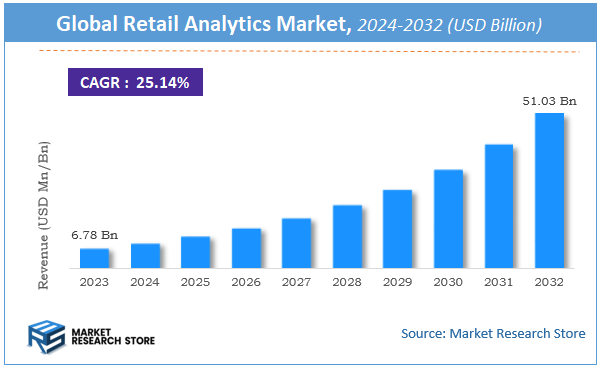

| Market Size 2023 (Base Year) | USD 6.78 Billion |

| Market Size 2032 (Forecast Year) | USD 51.03 Billion |

| CAGR | 25.14% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Retail Analytics Market Insights

According to Market Research Store, the global retail analytics market size was valued at around USD 6.78 billion in 2023 and is estimated to reach USD 51.03 billion by 2032, to register a CAGR of approximately 25.14% in terms of revenue during the forecast period 2024-2032.

The retail analytics report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Retail Analytics Market: Overview

Retail analytics refers to the process of collecting, analyzing, and interpreting data related to retail operations to improve decision-making and enhance overall business performance. It leverages technologies such as artificial intelligence (AI), machine learning (ML), big data, and predictive analytics to extract actionable insights from customer behavior, sales trends, inventory levels, pricing strategies, and marketing effectiveness. Retail analytics helps businesses understand consumer preferences, optimize inventory management, personalize shopping experiences, and increase profitability by making data-driven decisions across the supply chain and customer lifecycle.

Key Highlights

- The retail analytics market is anticipated to grow at a CAGR of 25.14% during the forecast period.

- The global retail analytics market was estimated to be worth approximately USD 6.78 billion in 2023 and is projected to reach a value of USD 51.03 billion by 2032.

- The growth of the retail analytics market is being driven by increasing adoption of digital technologies and the growing need for real-time insights in a highly competitive retail environment.

- Based on the business function, the marketing & customer analytics segment is growing at a high rate and is projected to dominate the market.

- On the basis of solution, the analytics tools segment is projected to swipe the largest market share.

- In terms of service, the consulting & system integration segment is expected to dominate the market.

- Based on the organization size, the large enterprises segment is expected to dominate the market.

- In terms of deployment model, the cloud segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Retail Analytics Market: Dynamics

Key Growth Drivers:

- Growing Demand for Data-Driven Decision Making: Retailers are increasingly using analytics to understand customer behavior, optimize inventory, and improve store performance.

- Expansion of Omnichannel Retailing: As businesses integrate online and offline platforms, analytics help track customer journeys across multiple touchpoints.

- Advancement in AI and Machine Learning Technologies: AI-powered analytics tools are enabling predictive insights and real-time decision-making in retail operations.

- Increased Adoption of Cloud-Based Solutions: Cloud platforms offer scalability and accessibility, making analytics more affordable and easier to implement for retailers of all sizes.

Restraints:

- High Initial Investment and Integration Costs: Setting up retail analytics systems can be expensive, especially for small and medium retailers.

- Data Privacy and Security Concerns: Handling vast amounts of consumer data brings challenges in complying with privacy regulations like GDPR and CCPA.

- Lack of Skilled Professionals: A shortage of data scientists and analytics experts may hinder effective implementation of analytics tools in retail businesses.

Opportunities:

- Growing Use of Real-Time Analytics: Real-time dashboards and insights help retailers react instantly to customer demands and market changes.

- Rise of Personalization and Customer Experience Enhancements: Analytics enables hyper-personalized offers and product recommendations, improving customer satisfaction and loyalty.

- Expansion in Emerging Economies: Rapid digitalization and increased smartphone penetration in developing countries present significant market growth potential.

Challenges:

- Data Silos Across Retail Channels: Integrating data from various platforms like POS, CRM, and e-commerce systems remains complex for many retailers.

- Rapidly Changing Consumer Preferences: Keeping analytics tools updated to reflect evolving customer behaviors requires constant innovation.

- Regulatory Compliance Complexity: Navigating international laws and compliance regulations across regions is a persistent operational challenge.

Retail Analytics Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Retail Analytics Market |

| Market Size in 2023 | USD 6.78 Billion |

| Market Forecast in 2032 | USD 51.03 Billion |

| Growth Rate | CAGR of 25.14% |

| Number of Pages | 170 |

| Key Companies Covered | International Business Machines Corporation (IBM), Information Builders, SAS Institute, Inc., Oracle Corporation, Tableau Software, Inc., SAP SE, Microsoft Corporation, Adobe Systems Incorporated, Microstrategy Incorporated, Qlik Technologies, Inc., Manthan, Bridgei2i, Teradata, HCL, Fujitsu, Domo, Google, FLIR Systems, Capillary, RetailNext, and WNS, among others |

| Segments Covered | By Business Function, By Solution, By Service, By Organization Size, By Deployment Type, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Retail Analytics Market: Segmentation Insights

The global retail analytics market is divided by business function, solution, service, organization size, deployment model, and region.

Based on business function, the global retail analytics market is divided into supply chain analytics, merchandizing & in-store analytics, marketing & customer analytics, and strategy & planning. Marketing & customer analytics is the most dominant business function segment, as retailers increasingly rely on data-driven insights to understand consumer behavior, personalize shopping experiences, and optimize marketing campaigns. This segment enables businesses to analyze customer preferences, buying patterns, loyalty trends, and real-time engagement metrics across both online and offline channels. The growing emphasis on delivering targeted promotions, enhancing customer retention, and improving ROI from marketing investments makes this function the top priority for retail analytics adoption. Merchandizing & in-store analytics ranks as the second most significant segment. This function helps retailers make informed decisions about product assortment, shelf placement, pricing, and inventory allocation within physical stores. It also enables the use of technologies like heat maps and footfall tracking to evaluate in-store customer behavior, optimize store layouts, and enhance conversion rates. As brick-and-mortar retailers strive to compete with e-commerce by improving the in-store experience, demand for these analytics tools continues to grow steadily.

On the basis of solution, the global retail analytics market is bifurcated into reporting & visualization tools, analytics tools, data management software, and mobile applications. Analytics tools are the most dominant solution segment, as they provide the core capability for processing and interpreting large volumes of data to generate actionable insights. These tools include predictive analytics, customer behavior modeling, pricing optimization, and trend forecasting, which enable retailers to make data-driven decisions across marketing, inventory, operations, and customer engagement. Their ability to deliver real-time insights and support strategic initiatives makes them central to most retail analytics implementations. Reporting & visualization tools are the second most widely adopted solution, essential for converting complex data into clear, visual formats that support quick understanding and decision-making. These tools help retail managers and executives track key performance indicators (KPIs), monitor store performance, and analyze sales trends through dashboards and charts.

Based on service, the global retail analytics market is divided into support & maintenance service, and consulting & system integration. Consulting & system integration services are the most dominant service segment, as businesses increasingly seek expert guidance to implement, customize, and integrate advanced analytics solutions into their existing retail ecosystems. These services help retailers define data strategies, ensure seamless integration across multiple platforms (such as POS, CRM, and ERP), and tailor analytics tools to meet specific business goals. The complexity of analytics deployment, combined with the need for industry-specific expertise, makes consulting and system integration critical for successful implementation. Support & maintenance services form the second segment, ensuring the smooth functioning, regular updates, and troubleshooting of deployed analytics systems. These services are vital for maintaining system performance, managing software upgrades, addressing technical issues, and providing ongoing user training.

On the basis of organization size, the global retail analytics market is bifurcated into small & medium-sized enterprises (SMEs), and large enterprises. Large enterprises dominate the organization size segmentation due to their higher budget allocation, advanced digital infrastructure, and complex retail operations that demand sophisticated analytics solutions. These organizations typically operate across multiple channels and regions, requiring in-depth insights into customer behavior, supply chain efficiency, and performance metrics. With greater access to resources, large enterprises are early adopters of technologies like AI, predictive analytics, and real-time data visualization to drive strategic decisions and maintain competitive advantage. Small & medium-sized enterprises (SMEs) represent a growing segment, driven by the increasing availability of affordable, cloud-based retail analytics solutions. SMEs are increasingly recognizing the value of data-driven insights to enhance customer engagement, optimize inventory, and compete with larger players. Although adoption is relatively lower compared to large enterprises, the flexibility, scalability, and cost-effectiveness of modern analytics tools are making it easier for SMEs to integrate them into their operations, contributing to steady market growth in this segment.

In terms of deployment model, the global retail analytics market is bifurcated into cloud and on-premises. Cloud-based deployment is the most dominant model, driven by its flexibility, scalability, and cost-efficiency. Cloud solutions allow retailers to access analytics platforms from anywhere, enabling real-time data processing, quicker updates, and seamless integration with various digital touchpoints such as e-commerce platforms, mobile apps, and social media. Additionally, cloud deployment reduces the need for significant upfront infrastructure investments, making it a preferred choice for both large enterprises and SMEs. The growing trend toward digital transformation and remote operations has further accelerated the adoption of cloud-based retail analytics. On-premises deployment, while less dominant, is still relevant for retailers with strict data security requirements or those operating in regions with limited cloud infrastructure. This model gives businesses full control over their data and analytics systems, which is particularly important for organizations dealing with sensitive customer information or regulatory compliance. However, the higher cost of hardware, maintenance, and IT staff makes it less attractive compared to the cloud, especially for smaller retailers.

Retail Analytics Market: Regional Insights

- North America is expected to dominates the global market

The most dominant region in the global retail analytics market is North America, driven by advanced digital infrastructure, early adoption of big data and AI technologies, and a highly competitive retail landscape. Retailers in the U.S. and Canada are leveraging analytics to enhance customer experience, optimize inventory, personalize marketing, and streamline operations across physical and digital platforms. The strong presence of leading analytics providers and high investment in retail technology further solidify the region’s leadership in the global market.

Europe holds the second-largest share in the retail analytics market, supported by widespread digital transformation and a strong emphasis on data privacy and compliance. Retailers in countries such as the UK, Germany, and France are increasingly integrating analytics solutions to improve supply chain efficiency, enhance customer engagement, and support sustainability initiatives. The region’s mature retail sector and proactive approach to technological innovation contribute to its continued growth.

Asia Pacific is experiencing the fastest growth in the retail analytics market, fueled by the rapid expansion of e-commerce, rising internet penetration, and increasing adoption of digital payment systems. Countries like China, India, and Japan are leading the region’s transformation, as retailers focus on data-driven insights to cater to a vast and diverse consumer base. Government initiatives promoting digitalization and smart retail practices are also accelerating the adoption of analytics solutions.

Latin America is emerging as a growing market, with countries such as Brazil, Mexico, and Argentina witnessing increased adoption of retail analytics to improve operational efficiency and customer satisfaction. While the region is still in the developing phase compared to others, rising competition in the retail sector and the growth of online shopping are pushing businesses to invest in advanced analytics tools.

Middle East and Africa represent the smallest share of the retail analytics market. However, the region is gradually adopting analytics solutions, particularly in Gulf countries and South Africa, where investments in smart cities, modern retail formats, and digital infrastructure are growing. Although still at an early stage, the market holds potential as retailers seek to modernize and deliver more personalized shopping experiences.

Retail Analytics Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the retail analytics market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global retail analytics market include:

- International Business Machines Corporation (IBM)

- Information Builders

- SAS Institute Inc.

- Oracle Corporation

- Tableau Software Inc.

- SAP SE

- Microsoft Corporation

- Adobe Systems Incorporated

- Microstrategy Incorporated

- Qlik Technologies Inc.

- Manthan

- Bridgei2i

- Teradata

- HCL

- Fujitsu

- Domo

- FLIR Systems

- Capillary

- RetailNext

- WNS

The global retail analytics market is segmented as follows:

By Business Function

- Supply Chain Analytics

- Merchandizing and In-Store Analytics

- Marketing and Customer Analytics

- Strategy and Planning

By Solution

- Reporting and Visualization Tools

- Analytics Tools

- Data Management Software

- Mobile Applications

By Service

- Support and Maintenance Service

- Consulting

- System Integration

By Organization Size

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

By Deployment Model

- Cloud

- On-Premises

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1.Preface

- 1.1.Report Description

- 1.1.Report Scope

- Chapter 2.Research Methodulogy

- 2.1.Research Methodulogy

- 2.2.Secondary Research

- 2.3.Primary Research

- 2.4.Models

- 2.4.1.Company Share Analysis Model

- 2.4.2.Revenue Based Modeling

- 2.5.Research Limitations

- Chapter 3.Executive Summary

- 3.1.Global Retail Analytics Market, 2016 – 2026 (USD Million)

- 3.2.Global Retail Analytics Market: Snapshot

- Chapter 4.Retail Analytics Market – Industry Analysis

- 4.1.Introduction

- 4.2.Market Drivers

- 4.2.1.Driving Factor 1 Analysis

- 4.2.2.Driving Factor 2 Analysis:

- 4.3.Market Restraints

- 4.3.1.Restraining Factor Analysis

- 4.4.Market Opportunities

- 4.4.1.Market Opportunity & Use-case Anaysis

- 4.4.2.Use – Cases for Retail Analytics

- 4.5.Porter’s Five Forces Analysis

- 4.6.COVID 19 Impact Analysis

- 4.6.1.1.Impact on Product Development and Technulogy Adoption

- 4.6.1.2.Gap Analysis

- Chapter 5.Investment Proposition Analysis

- 5.1.Global Retail Analytics Market Attractiveness, By Business Function

- 5.2.Global Retail Analytics Market Attractiveness, By Sulution

- 5.3.Global Retail Analytics Market Attractiveness, By Service

- 5.4.Global Retail Analytics Market Attractiveness, By Organization Size

- 5.5.Global Retail Analytics Market Attractiveness, By Deployment Model

- 5.6.Global Retail Analytics Market Attractiveness, By Region

- Chapter 6.Competitive Landscape

- 6.1.Company Market Share Analysis - 2019

- 6.1.1.Global Retail Analytics Market: Company Market Share, 2019

- 6.2.Strategic Developments

- 6.1.Company Market Share Analysis - 2019

- Chapter 7.Retail Analytics Market – Business Function Segment Analysis

- 7.1.Global Retail Analytics Market Overview: by Business Function

- 7.1.1.Global Retail Analytics Market Revenue Share, by Business Function, 2019 & 2026

- 7.2.Global Retail Analytics Market Analysis/Overview – By Business Function

- 7.2.1.Marketing and Customer Analytics – Overview/Analysis

- 7.2.2.Supply Chain Analytics – Overview/Analysis

- 7.2.3.Merchandizing and In-Store Analytics – Overview/Analysis

- 7.2.4.Strategy and Planning – Overview/Analysis

- 7.3.Marketing and Customer Analytics

- 7.3.1.Global Retail Analytics Market for Marketing and Customer Analytics, Revenue (USD Million) 2016 - 2026

- 7.4.Supply Chain Analytics

- 7.4.1.Global Retail Analytics Market for Supply Chain Analytics, Revenue (USD Million) 2016 - 2026

- 7.5.Merchandizing and In-Store Analytics

- 7.5.1.Global Retail Analytics Market for Merchandizing and In-Store Analytics, Revenue (USD Million) 2016 - 2026

- 7.6.Strategy and Planning

- 7.6.1.Global Retail Analytics Market for Strategy and Planning, Revenue (USD Million) 2016 - 2026

- 7.1.Global Retail Analytics Market Overview: by Business Function

- Chapter 8.Retail Analytics Market – Sulution Segment Analysis

- 8.1.Global Retail Analytics Market Overview: by Sulution

- 8.1.1.Global Retail Analytics Market Revenue Share, by Sulution, 2019 & 2026

- 8.2.Global Retail Analytics Market Analysis/Overview – By Sulution

- 8.2.1.Analytics Touls – Overview/Analysis

- 8.2.2.Reporting And Visualization Touls – Overview/Analysis

- 8.2.3.Data Management Software – Overview/Analysis

- 8.2.4.Mobile Applications – Overview/Analysis

- 8.3.Analytics Touls

- 8.3.1.Global Retail Analytics Market for Analytics Touls, Revenue (USD Million) 2016 - 2026

- 8.4.Reporting And Visualization Touls

- 8.4.1.Global Retail Analytics Market for Reporting And Visualization Touls, Revenue (USD Million) 2016 - 2026

- 8.5.Data Management Software

- 8.5.1.Global Retail Analytics Market for Data Management Software, Revenue (USD Million) 2016 - 2026

- 8.6.Mobile Applications

- 8.6.1.Global Retail Analytics Market for Mobile Applications, Revenue (USD Million) 2016 - 2026

- 8.1.Global Retail Analytics Market Overview: by Sulution

- Chapter 9.Retail Analytics Market – Service Segment Analysis

- 9.1.Global Retail Analytics Market Overview: by Service

- 9.1.1.Global Retail Analytics Market Revenue Share, by Service, 2019 & 2026

- 9.2.Global Retail Analytics Market Analysis/Overview – By Service

- 9.2.1.Consulting and System Integration – Overview/Analysis

- 9.2.2.Support and Maintenance Service – Overview/Analysis

- 9.3.Consulting and System Integration

- 9.3.1.Global Retail Analytics Market for Consulting and System Integration , Revenue (USD Million) 2016 - 2026

- 9.4.Support and Maintenance Service

- 9.4.1.Global Retail Analytics Market for Support and Maintenance Service , Revenue (USD Million) 2016 - 2026

- 9.1.Global Retail Analytics Market Overview: by Service

- Chapter 10.Retail Analytics Market – Organization Size Segment Analysis

- 10.1.Global Retail Analytics Market Overview: by Organization Size

- 10.1.1.Global Retail Analytics Market Revenue Share, by Organization Size, 2019 & 2026

- 10.2.Global Retail Analytics Market Analysis/Overview – By Organization Size

- 10.2.1.Small and Medium-sized Enterprises (SMEs) – Overview/Analysis

- 10.2.2.Large Enterprises – Overview/Analysis

- 10.3.Small and Medium-sized Enterprises (SMEs)

- 10.3.1.Global Retail Analytics Market for Small and Medium-sized Enterprises (SMEs) , Revenue (USD Million) 2016 - 2026

- 10.4.Large Enterprises

- 10.4.1.Global Retail Analytics Market for Large Enterprises, Revenue (USD Million) 2016 - 2026

- 10.1.Global Retail Analytics Market Overview: by Organization Size

- Chapter 11.Retail Analytics Market – Deployment Model Segment Analysis

- 11.1.Global Retail Analytics Market Overview: by Deployment Model

- 11.1.1.Global Retail Analytics Market Revenue Share, by Deployment Model, 2019 & 2026

- 11.2.Global Retail Analytics Market Analysis/Overview – By Deployment Model

- 11.2.1.On-Premises – Overview/Analysis

- 11.2.2.Cloud – Overview/Analysis

- 11.3.On-Premises

- 11.3.1.Global Retail Analytics Market for On-Premises, Revenue (USD Million) 2016 - 2026

- 11.4.Cloud

- 11.4.1.Global Retail Analytics Market for Cloud, Revenue (USD Million) 2016 - 2026

- 11.1.Global Retail Analytics Market Overview: by Deployment Model

- Chapter 12.Retail Analytics Market – Regional Analysis

- 12.1.Global Retail Analytics Market: Regional Overview

- 12.1.1.Global Retail Analytics Market Revenue Share, by Region, 2019 & 2026

- 12.1.2.Global Retail Analytics Market Revenue, by Region, 2016 – 2026 (USD Million)

- 12.2.North America

- 12.2.1.North America Retail Analytics Market Revenue, 2016 - 2026 (USD Million)

- 12.2.2.North America Retail Analytics Market Revenue, by Country, 2016 – 2026 (USD Million)

- 12.2.3.North America Retail Analytics Market Revenue, by Business Function, 2016 – 2026

- 12.2.4.North America Retail Analytics Market Revenue, by Sulution, 2016 – 2026

- 12.2.5.North America Retail Analytics Market Revenue, by Service, 2016 – 2026

- 12.2.6.North America Retail Analytics Market Revenue, by Organization Size, 2016 – 2026

- 12.2.7.North America Retail Analytics Market Revenue, by Deployment Model, 2016 – 2026

- 12.2.8. U.S.

- 12.2.9.Canada

- 12.3.Europe

- 12.3.1.Europe Retail Analytics Market Revenue, 2016 - 2026 (USD Million)

- 12.3.2.Europe Retail Analytics Market Revenue, by Country, 2016 – 2026 (USD Million)

- 12.3.3.Europe Retail Analytics Market Revenue, by Business Function, 2016 – 2026

- 12.3.4.Europe Retail Analytics Market Revenue, by Sulution, 2016 – 2026

- 12.3.5.Europe Retail Analytics Market Revenue, by Service, 2016 – 2026

- 12.3.6.Europe Retail Analytics Market Revenue, by Organization Size, 2016 – 2026

- 12.3.7.Europe Retail Analytics Market Revenue, by Deployment Model, 2016 – 2026

- 12.3.8.Germany

- 12.3.9.France

- 12.3.10. U.K.

- 12.3.11.Italy

- 12.3.12.Spain

- 12.3.13.Rest of Europe

- 12.4.Asia Pacific

- 12.4.1.Asia Pacific Retail Analytics Market Revenue, 2016 - 2026 (USD Million)

- 12.4.2.Asia Pacific Retail Analytics Market Revenue, by Country, 2016 – 2026 (USD Million)

- 12.4.3.Asia Pacific Retail Analytics Market Revenue, by Business Function, 2016 – 2026

- 12.4.4.Asia Pacific Retail Analytics Market Revenue, by Sulution, 2016 – 2026

- 12.4.5.Asia Pacific Retail Analytics Market Revenue, by Service, 2016 – 2026

- 12.4.6.Asia Pacific Retail Analytics Market Revenue, by Organization Size, 2016 – 2026

- 12.4.7.Asia Pacific Retail Analytics Market Revenue, by Deployment Model, 2016 – 2026

- 12.4.8.China

- 12.4.9.Japan

- 12.4.10.India

- 12.4.11.South Korea

- 12.4.12.South-East Asia

- 12.4.13.Rest of Asia Pacific

- 12.5.Latin America

- 12.5.1.Latin America Retail Analytics Market Revenue, 2016 - 2026 (USD Million)

- 12.5.2.Latin America Retail Analytics Market Revenue, by Country, 2016 – 2026 (USD Million)

- 12.5.3.Latin America Retail Analytics Market Revenue, by Business Function, 2016 – 2026

- 12.5.4.Latin America Retail Analytics Market Revenue, by Sulution, 2016 – 2026

- 12.5.5.Latin America Retail Analytics Market Revenue, by Service, 2016 – 2026

- 12.5.6.Latin America Retail Analytics Market Revenue, by Organization Size, 2016 – 2026

- 12.5.7.Latin America Retail Analytics Market Revenue, by Deployment Model, 2016 – 2026

- 12.5.8.Brazil

- 12.5.9.Mexico

- 12.5.10.Rest of Latin America

- 12.6.The Middle-East and Africa

- 12.6.1.The Middle-East and Africa Retail Analytics Market Revenue, 2016 - 2026 (USD Million)

- 12.6.2.The Middle-East and Africa Retail Analytics Market Revenue, by Country, 2016 – 2026 (USD Million)

- 12.6.3.The Middle-East and Africa Retail Analytics Market Revenue, by Business Function, 2016 – 2026

- 12.6.4.The Middle-East and Africa Retail Analytics Market Revenue, by Sulution, 2016 – 2026

- 12.6.5.The Middle-East and Africa Retail Analytics Market Revenue, by Service, 2016 – 2026

- 12.6.6.The Middle-East and Africa Retail Analytics Market Revenue, by Organization Size, 2016 – 2026

- 12.6.7.The Middle-East and Africa Retail Analytics Market Revenue, by Deployment Model, 2016 – 2026

- 12.6.8.GCC Countries

- 12.6.9.South Africa

- 12.6.10.Rest of Middle-East Africa

- 12.1.Global Retail Analytics Market: Regional Overview

- Chapter 13.Company Profiles

- 13.1.International Business Machines Corporation (IBM)

- 13.1.1.Company Overview

- 13.1.2.Financial Overview

- 13.1.3.Product Portfulio

- 13.1.4.Business Strategy

- 13.1.5.Recent Developments

- 13.2.SAS Institute, Inc.

- 13.3.Information Builders

- 13.4.Tableau Software, Inc.

- 13.5.Oracle Corporation

- 13.6.Microsoft Corporation

- 13.7.SAP SE

- 13.8.Adobe Systems Incorporated

- 13.9.Microstrategy Incorporated

- 13.1.Qlik Technulogies, Inc.

- 13.11.Manthan

- 13.12.Bridgei2i

- 13.13.Teradata

- 13.14.HCL

- 13.15.Fujitsu

- 13.16.Domo

- 13.17.Google

- 13.18.FLIR Systems

- 13.19.Capillary

- 13.2.RetailNext

- 13.21.WNS

- 13.1.International Business Machines Corporation (IBM)

Inquiry For Buying

Retail Analytics

Request Sample

Retail Analytics