Paper Cigarette Packaging Market Size, Share, and Trends Analysis Report

CAGR :

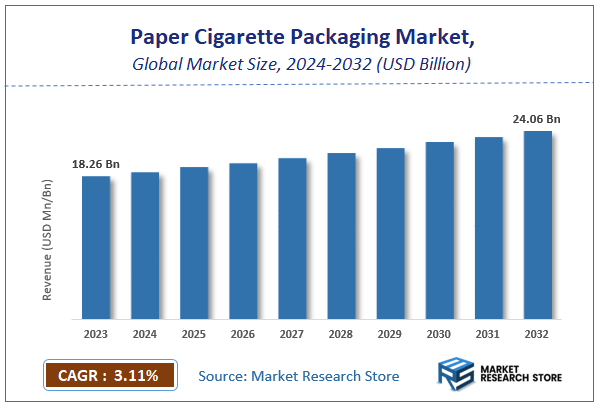

| Market Size 2023 (Base Year) | USD 18.26 Billion |

| Market Size 2032 (Forecast Year) | USD 24.06 Billion |

| CAGR | 3.11% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Paper Cigarette Packaging Market Insights

According to Market Research Store, the global paper cigarette packaging market size was valued at around USD 18.26 billion in 2023 and is estimated to reach USD 24.06 billion by 2032, to register a CAGR of approximately 3.11% in terms of revenue during the forecast period 2024-2032.

The paper cigarette packaging report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Paper Cigarette Packaging Market: Overview

Paper cigarette packaging refers to the use of paper-based materials—such as kraft paper, coated paperboard, and recycled paper—for wrapping and enclosing cigarettes. This packaging is primarily used to protect cigarettes from moisture and damage, offer brand identification through printed labels and logos, and comply with regulatory labeling standards. As the tobacco industry faces growing environmental and legislative pressures, paper packaging is increasingly replacing plastic and foil-based alternatives, making it a more sustainable and compliant option. Innovations such as anti-counterfeit features, moisture-resistant coatings, and biodegradable inks are also being incorporated into these paper-based packages to enhance functionality and appeal.

Key Highlights

- The paper cigarette packaging market is anticipated to grow at a CAGR of 3.11% during the forecast period.

- The global paper cigarette packaging market was estimated to be worth approximately USD 18.26 billion in 2023 and is projected to reach a value of USD 24.06 billion by 2032.

- The growth of the paper cigarette packaging market is being driven by increasing demand for eco-friendly solutions and stringent packaging regulations, such as plain packaging laws and graphic health warnings.

- Based on the material type, the kraft paper segment is growing at a high rate and is projected to dominate the market.

- On the basis of packaging type, the hard pack segment is projected to swipe the largest market share.

- In terms of printing type, the offset printing segment is expected to dominate the market.

- Based on the end-user, the tobacco manufacturers segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Paper Cigarette Packaging Market: Dynamics

Key Growth Drivers

- Rising Environmental Awareness: Increasing demand for eco-friendly alternatives to plastic has accelerated the shift toward recyclable and biodegradable paper-based cigarette packaging.

- Strict Regulatory Compliance: Governments globally are enforcing plain packaging laws and graphic health warnings, which favor standardized, cost-effective paper packaging.

- Premium Branding & Customization: High-quality paper allows advanced printing techniques, embossing, and tactile finishes that enhance shelf appeal and brand identity.

- Growth in Emerging Markets: Expanding tobacco consumption in Asia-Pacific, Latin America, and parts of Africa is boosting demand for low-cost and locally sourced paper packaging solutions.

Restraints

- Declining Smoking Rates: Increased health consciousness, anti-smoking campaigns, and high taxation in developed markets are causing a decline in traditional cigarette consumption.

- Volatility in Raw Material Prices: Fluctuating costs of paper pulp, chemicals, and transportation can impact profitability and cause supply chain instability.

- Regulatory Restrictions on Branding: While regulations drive demand for paper, they also restrict brand visibility—limiting the potential for customized or premium design features.

Opportunities

- Sustainable Packaging Innovations: The development of compostable, hemp-based, and FSC-certified paper opens new avenues for environmentally conscious cigarette packaging.

- Expansion into Next-Gen Tobacco Products: Growing markets for e-cigarettes, heated tobacco, and nicotine pouches create demand for adaptable paper packaging formats.

- Smart Packaging Features: Integration of QR codes, authentication tags, and interactive packaging adds value, especially in premium and export segments.

- E-commerce & Direct-to-Consumer Growth: Cigarette brands exploring online channels are adopting robust, attractive paper packaging that enhances unboxing experiences.

Challenges

- Counterfeit Risks: Paper-based packs are easier to replicate than some plastic or foil alternatives, posing a threat to brand integrity and consumer trust.

- Stringent Compliance Requirements: Constantly evolving tobacco regulations across countries require frequent packaging updates, increasing operational costs and complexity.

- Recyclability vs. Functionality Trade-Off: Achieving the right balance between environmental friendliness and performance (e.g., moisture resistance) remains technically challenging.

- Limited Shelf Differentiation: Plain packaging laws make it difficult for brands to stand out on retail shelves, which may reduce consumer engagement and loyalty.

Paper Cigarette Packaging Market: Report Scope

This report thoroughly analyzes the Paper Cigarette Packaging Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Paper Cigarette Packaging Market |

| Market Size in 2023 | USD 18.26 Billion |

| Market Forecast in 2032 | USD 24.06 Billion |

| Growth Rate | CAGR of 3.11% |

| Number of Pages | 165 |

| Key Companies Covered | Japan Tobacco International, Sonoco Product Company, Bihlmaier Gmbh, Innovia Films, Philip Morris International, Mondi Group, Novelis, British American Tobacco, The International Paper Company, Reynolds American Corporation, WestRock, Smurfit Kappa Group PLC, Mayr-Melnhof Packaging International, ITC, and Amcor |

| Segments Covered | By Material Type, By Packaging Type, By Printing Type, By End-User, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Paper Cigarette Packaging Market: Segmentation Insights

The global paper cigarette packaging market is divided by material type, packaging type, printing type, end-user, and region.

Based on material type, the global paper cigarette packaging market is divided into kraft paper, white board, recycled paper, and others. Kraft paper emerges as the most dominant material segment. Known for its durability, eco-friendliness, and resistance to tearing, Kraft paper is widely used for cigarette packs, wrappers, and cartons—particularly in regions emphasizing sustainable and biodegradable packaging solutions. Its natural texture and compatibility with moisture-resistant coatings make it ideal for protecting tobacco products while aligning with environmental regulations and consumer demand for green packaging.

On the basis of packaging type, the global paper cigarette packaging market is bifurcated into hard pack, soft pack, and others. The Hard Pack segment dominates the paper cigarette packaging market. Hard packs, typically made from sturdy paperboard, offer superior protection against physical damage and moisture, ensuring better preservation of cigarettes during transportation and storage. They also allow for high-quality printing, embossing, and the application of anti-counterfeit features, making them the preferred choice for premium and mass-market cigarette brands alike. Their rigid structure supports shelf stability and consumer convenience, contributing significantly to brand appeal and market dominance.

Based on printing type, the global paper cigarette packaging market is divided into offset printing, flexographic printing, gravure printing, and others. Offset Printing stands out as the most dominant printing type. Valued for its exceptional print quality, precision, and cost-effectiveness in large-volume runs, offset printing is widely used for producing cigarette packs with vibrant colors, sharp graphics, and detailed branding. This method supports high-resolution imagery and complex health warnings required by regulatory standards, making it ideal for both premium and mass-market cigarette packaging across global markets.

In terms of end-user, the global paper cigarette packaging market is bifurcated into tobacco manufacturers, retailers, and others. Tobacco Manufacturers represent the most dominant end-user segment. These companies are the primary consumers of paper packaging as they handle large-scale cigarette production and require consistent, high-quality, and regulatory-compliant packaging solutions. With rising global demand for sustainable and cost-effective materials, tobacco manufacturers are increasingly investing in eco-friendly paper packaging that accommodates graphic warnings, brand identity, and moisture resistance. Their influence drives innovation and volume demand across the entire packaging supply chain.

Paper Cigarette Packaging Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific leads the paper cigarette packaging market, capturing just over a third of total revenue. Its dominance stems from enormous populations in China, India, Indonesia, and Japan, along with rising incomes and ongoing urbanization. The region is not only the largest consumer but also a major producer, with multinational players and local producers scaling up operations in countries like Vietnam and Indonesia to serve both domestic and export demand. Innovation abounds, with premium and heat‑resistant papers for heated products gaining traction alongside eco‑friendly materials like biotech and unbleached pulp.

North America ranks second, contributing around 30% of market revenue. This mature market is shaped by stringent regulations on health warnings, child-resistant packaging, and environmental mandates that push the shift to recyclable and biodegradable solutions. The growth here is driven by diversification beyond traditional cigarettes into vaping, heated tobacco, nicotine pouches, and premium cigars. Packaging innovation focuses on tamper-evident, moisture‑resistant formats and sustainable materials. Major tobacco companies and packaging firms maintain leading-edge infrastructure and strong compliance-driven demand.

Europe holds the third-largest share (about a quarter of the market), bolstered by strict tobacco regulations like the EU Tobacco Products Directive, high printing standards, and environmental directives such as bans on plastics. While traditional cigarette consumption declines, the region sustains robust demand through premiumized packaging and technological enhancements like anti‑counterfeit features and smart labelling. Manufacturers here focus heavily on recycled content, sustainable coatings, and biodegradable inks to meet sustainability goals while maintaining brand differentiation.

Latin America represents approximately 5% of the global paper cigarette packaging market. Its tobacco packaging sector reflects a balance between cost-sensitive mass-market cigarettes and growing interest in premium cigars and smokeless products. Regional drivers include regulatory modernization, fluctuating economies (e.g., Brazil, Argentina), and expanding rural distribution networks. Packaging choice favors affordability—like heavier papers and moisture-resistant coatings—while certain markets explore biodegradable and mid-quality paperboards to elevate brand perception.

Middle East & Africa also comprises about 5% of total revenue, characterized by gradual but steady consumption growth in nations such as South Africa, Nigeria, and UAE. Market expansion is fueled by urbanization, a youthful demographic, and rising per-capita tobacco use. Regulatory frameworks are at varying stages, but the push for health warnings and sustainability is gaining momentum. Producers here increasingly source materials locally or from value-priced hubs in Morocco and South Asia, while premium segments adopt features like moisture control, embossing, and childproof seals.

Paper Cigarette Packaging Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the paper cigarette packaging market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global paper cigarette packaging market include:

- Japan Tobacco International

- Sonoco Product Company

- Bihlmaier Gmbh

- Innovia Films

- Philip Morris International

- Mondi Group

- Novelis

- British American Tobacco

- The International Paper Company

- Reynolds American Corporation

- WestRock

- Smurfit Kappa Group PLC

- Mayr-Melnhof Packaging International

- ITC

- Amcor

The global paper cigarette packaging market is segmented as follows:

By Material Type

- Kraft Paper

- White Board

- Recycled Paper

- Others

By Packaging Type

- Hard Pack

- Soft Pack

- Others

By Printing Type

- Offset Printing

- Flexographic Printing

- Gravure Printing

- Others

By End-User

- Tobacco Manufacturers

- Retailers

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1 Executive Summary

- 1.1. Introduction of Paper Cigarette Packaging

- 1.2. Global Paper Cigarette Packaging Market, 2020 & 2026 (USD Million)

- 1.3. Global Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 1.4. Global Paper Cigarette Packaging Market Absulute Revenue Opportunity, 2016 – 2026 (USD Million)

- 1.5. Global Paper Cigarette Packaging Market Incremental Revenue Opportunity, 2020 – 2026 (USD Million)

- Chapter 2 Paper Cigarette Packaging Market – Type Analysis

- 2.1. Global Paper Cigarette Packaging Market – Type Overview

- 2.2. Global Paper Cigarette Packaging Market Share, by Type, 2020 & 2026 (USD Million)

- 2.3. Flexible Packaging

- 2.3.1. Global Flexible Packaging Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 2.4. Hard Packaging

- 2.4.1. Global Hard Packaging Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- Chapter 3 Paper Cigarette Packaging Market – Application Analysis

- 3.1. Global Paper Cigarette Packaging Market – Application Overview

- 3.2. Global Paper Cigarette Packaging Market Share, by Application, 2020 & 2026 (USD Million)

- 3.3. Smoking Tobacco

- 3.3.1. Global Smoking Tobacco Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 3.4. Smokeless Tobacco

- 3.4.1. Global Smokeless Tobacco Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 3.5. Raw Tobacco

- 3.5.1. Global Raw Tobacco Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- Chapter 4 Paper Cigarette Packaging Market – Regional Analysis

- 4.1. Global Paper Cigarette Packaging Market Regional Overview

- 4.2. Global Paper Cigarette Packaging Market Share, by Region, 2020 & 2026 (USD Million)

- 4.3. North America

- 4.3.1. North America Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.3.1.1. North America Paper Cigarette Packaging Market, by Country, 2016 - 2026 (USD Million)

- 4.3.2. North America Paper Cigarette Packaging Market, by Type, 2016 – 2026

- 4.3.2.1. North America Paper Cigarette Packaging Market, by Type, 2016 – 2026 (USD Million)

- 4.3.3. North America Paper Cigarette Packaging Market, by Application, 2016 – 2026

- 4.3.3.1. North America Paper Cigarette Packaging Market, by Application, 2016 – 2026 (USD Million)

- 4.3.4. U.S.

- 4.3.4.1. U.S. Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.3.5. Canada

- 4.3.5.1. Canada Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.3.1. North America Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4. Europe

- 4.4.1. Europe Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.1.1. Europe Paper Cigarette Packaging Market, by Country, 2016 - 2026 (USD Million)

- 4.4.2. Europe Paper Cigarette Packaging Market, by Type, 2016 – 2026

- 4.4.2.1. Europe Paper Cigarette Packaging Market, by Type, 2016 – 2026 (USD Million)

- 4.4.3. Europe Paper Cigarette Packaging Market, by Application, 2016 – 2026

- 4.4.3.1. Europe Paper Cigarette Packaging Market, by Application, 2016 – 2026 (USD Million)

- 4.4.4. Germany

- 4.4.4.1. Germany Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.5. France

- 4.4.5.1. France Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.6. U.K.

- 4.4.6.1. U.K. Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.7. Italy

- 4.4.7.1. Italy Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.8. Spain

- 4.4.8.1. Spain Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.9. Rest of Europe

- 4.4.9.1. Rest of Europe Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.4.1. Europe Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5. Asia Pacific

- 4.5.1. Asia Pacific Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.1.1. Asia Pacific Paper Cigarette Packaging Market, by Country, 2016 - 2026 (USD Million)

- 4.5.2. Asia Pacific Paper Cigarette Packaging Market, by Type, 2016 – 2026

- 4.5.2.1. Asia Pacific Paper Cigarette Packaging Market, by Type, 2016 – 2026 (USD Million)

- 4.5.3. Asia Pacific Paper Cigarette Packaging Market, by Application, 2016 – 2026

- 4.5.3.1. Asia Pacific Paper Cigarette Packaging Market, by Application, 2016 – 2026 (USD Million)

- 4.5.4. China

- 4.5.4.1. China Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.5. Japan

- 4.5.5.1. Japan Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.6. India

- 4.5.6.1. India Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.7. South Korea

- 4.5.7.1. South Korea Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.8. South-East Asia

- 4.5.8.1. South-East Asia Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.9. Rest of Asia Pacific

- 4.5.9.1. Rest of Asia Pacific Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.5.1. Asia Pacific Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.6. Latin America

- 4.6.1. Latin America Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.6.1.1. Latin America Paper Cigarette Packaging Market, by Country, 2016 - 2026 (USD Million)

- 4.6.2. Latin America Paper Cigarette Packaging Market, by Type, 2016 – 2026

- 4.6.2.1. Latin America Paper Cigarette Packaging Market, by Type, 2016 – 2026 (USD Million)

- 4.6.3. Latin America Paper Cigarette Packaging Market, by Application, 2016 – 2026

- 4.6.3.1. Latin America Paper Cigarette Packaging Market, by Application, 2016 – 2026 (USD Million)

- 4.6.4. Brazil

- 4.6.4.1. Brazil Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.6.5. Mexico

- 4.6.5.1. Mexico Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.6.6. Rest of Latin America

- 4.6.6.1. Rest of Latin America Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.6.1. Latin America Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.7. The Middle-East and Africa

- 4.7.1. The Middle-East and Africa Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.7.1.1. The Middle-East and Africa Paper Cigarette Packaging Market, by Country, 2016 - 2026 (USD Million)

- 4.7.2. The Middle-East and Africa Paper Cigarette Packaging Market, by Type, 2016 – 2026

- 4.7.2.1. The Middle-East and Africa Paper Cigarette Packaging Market, by Type, 2016 – 2026 (USD Million)

- 4.7.3. The Middle-East and Africa Paper Cigarette Packaging Market, by Application, 2016 – 2026

- 4.7.3.1. The Middle-East and Africa Paper Cigarette Packaging Market, by Application, 2016 – 2026 (USD Million)

- 4.7.4. GCC Countries

- 4.7.4.1. GCC Countries Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.7.5. South Africa

- 4.7.5.1. South Africa Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.7.6. Rest of Middle-East Africa

- 4.7.6.1. Rest of Middle-East Africa Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- 4.7.1. The Middle-East and Africa Paper Cigarette Packaging Market, 2016 – 2026 (USD Million)

- Chapter 5 Paper Cigarette Packaging Market – Competitive Landscape

- 5.1. Competitor Market Share – Revenue

- 5.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players

- 5.3. Strategic Developments

- 5.3.1. Acquisitions and Mergers

- 5.3.2. New Products

- 5.3.3. Research & Development Activities

- Chapter 6 Company Profiles

- 6.1. Japan Tobacco International

- 6.1.1. Company Overview

- 6.1.2. Product/Service Portfulio

- 6.1.3. Japan Tobacco International Sales, Revenue, and Gross Margin

- 6.1.4. Japan Tobacco International Revenue and Growth Rate

- 6.1.5. Japan Tobacco International Market Share

- 6.1.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.2. Sonoco Product Company

- 6.2.1. Company Overview

- 6.2.2. Product/Service Portfulio

- 6.2.3. Sonoco Product Company Sales, Revenue, and Gross Margin

- 6.2.4. Sonoco Product Company Revenue and Growth Rate

- 6.2.5. Sonoco Product Company Market Share

- 6.2.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.3. Bihlmaier Gmbh

- 6.3.1. Company Overview

- 6.3.2. Product/Service Portfulio

- 6.3.3. Bihlmaier Gmbh Sales, Revenue, and Gross Margin

- 6.3.4. Bihlmaier Gmbh Revenue and Growth Rate

- 6.3.5. Bihlmaier Gmbh Market Share

- 6.3.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.4. Innovia Films

- 6.4.1. Company Overview

- 6.4.2. Product/Service Portfulio

- 6.4.3. Innovia Films Sales, Revenue, and Gross Margin

- 6.4.4. Innovia Films Revenue and Growth Rate

- 6.4.5. Innovia Films Market Share

- 6.4.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.5. Philip Morris International

- 6.5.1. Company Overview

- 6.5.2. Product/Service Portfulio

- 6.5.3. Philip Morris International Sales, Revenue, and Gross Margin

- 6.5.4. Philip Morris International Revenue and Growth Rate

- 6.5.5. Philip Morris International Market Share

- 6.5.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.6. Mondi Group

- 6.6.1. Company Overview

- 6.6.2. Product/Service Portfulio

- 6.6.3. Mondi Group Sales, Revenue, and Gross Margin

- 6.6.4. Mondi Group Revenue and Growth Rate

- 6.6.5. Mondi Group Market Share

- 6.6.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.7. Novelis

- 6.7.1. Company Overview

- 6.7.2. Product/Service Portfulio

- 6.7.3. Novelis Sales, Revenue, and Gross Margin

- 6.7.4. Novelis Revenue and Growth Rate

- 6.7.5. Novelis Market Share

- 6.7.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.8. British American Tobacco

- 6.8.1. Company Overview

- 6.8.2. Product/Service Portfulio

- 6.8.3. British American Tobacco Sales, Revenue, and Gross Margin

- 6.8.4. British American Tobacco Revenue and Growth Rate

- 6.8.5. British American Tobacco Market Share

- 6.8.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.9. The International Paper Company

- 6.9.1. Company Overview

- 6.9.2. Product/Service Portfulio

- 6.9.3. The International Paper Company Sales, Revenue, and Gross Margin

- 6.9.4. The International Paper Company Revenue and Growth Rate

- 6.9.5. The International Paper Company Market Share

- 6.9.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.10. Reynulds American Corporation

- 6.10.1. Company Overview

- 6.10.2. Product/Service Portfulio

- 6.10.3. Reynulds American Corporation Sales, Revenue, and Gross Margin

- 6.10.4. Reynulds American Corporation Revenue and Growth Rate

- 6.10.5. Reynulds American Corporation Market Share

- 6.10.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.11. WestRock

- 6.11.1. Company Overview

- 6.11.2. Product/Service Portfulio

- 6.11.3. WestRock Sales, Revenue, and Gross Margin

- 6.11.4. WestRock Revenue and Growth Rate

- 6.11.5. WestRock Market Share

- 6.11.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.12. Smurfit Kappa Group PLC

- 6.12.1. Company Overview

- 6.12.2. Product/Service Portfulio

- 6.12.3. Smurfit Kappa Group PLC Sales, Revenue, and Gross Margin

- 6.12.4. Smurfit Kappa Group PLC Revenue and Growth Rate

- 6.12.5. Smurfit Kappa Group PLC Market Share

- 6.12.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.13. Mayr-Melnhof Packaging International

- 6.13.1. Company Overview

- 6.13.2. Product/Service Portfulio

- 6.13.3. Mayr-Melnhof Packaging International Sales, Revenue, and Gross Margin

- 6.13.4. Mayr-Melnhof Packaging International Revenue and Growth Rate

- 6.13.5. Mayr-Melnhof Packaging International Market Share

- 6.13.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.14. ITC

- 6.14.1. Company Overview

- 6.14.2. Product/Service Portfulio

- 6.14.3. ITC Sales, Revenue, and Gross Margin

- 6.14.4. ITC Revenue and Growth Rate

- 6.14.5. ITC Market Share

- 6.14.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.15. Amcor

- 6.15.1. Company Overview

- 6.15.2. Product/Service Portfulio

- 6.15.3. Amcor Sales, Revenue, and Gross Margin

- 6.15.4. Amcor Revenue and Growth Rate

- 6.15.5. Amcor Market Share

- 6.15.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 6.1. Japan Tobacco International

- Chapter 7 Paper Cigarette Packaging — Industry Analysis

- 7.1. Introduction and Taxonomy

- 7.2. Paper Cigarette Packaging Market – Key Trends

- 7.2.1. Market Drivers

- 7.2.2. Market Restraints

- 7.2.3. Market Opportunities

- 7.3. Value Chain Analysis

- 7.4. Key Mandates and Regulations

- 7.5. Technulogy Roadmap and Timeline

- 7.6. Paper Cigarette Packaging Market – Attractiveness Analysis

- 7.6.1. By Type

- 7.6.2. By Application

- 7.6.3. By Region

- Chapter 8 Industrial Chain, Sourcing Strategy, and Downstream Buyers

- 8.1. Paper Cigarette Packaging Industrial Chain Analysis

- 8.2. Downstream Buyers

- 8.3. Distributors/Traders List

- Chapter 9 Marketing Strategy Analysis

- 9.1. Marketing Channel

- 9.2. Direct Marketing

- 9.3. Indirect Marketing

- 9.4. Marketing Channel Development Trends

- 9.5. Economic/Pulitical Environmental Change

- Chapter 10 Report Conclusion & Key Insights

- 10.1. Key Insights from Primary Interviews & Surveys Respondents

- 10.2. Key Takeaways from Analysts, Consultants, and Industry Leaders

- Chapter 11 Research Approach & Methodulogy

- 11.1. Report Description

- 11.2. Research Scope

- 11.3. Research Methodulogy

- 11.3.1. Secondary Research

- 11.3.2. Primary Research

- 11.3.3. Statistical Models

- 11.3.3.1. Company Share Analysis Model

- 11.3.3.2. Revenue Based Modeling

- 11.3.4. Research Limitations

Inquiry For Buying

Paper Cigarette Packaging

Request Sample

Paper Cigarette Packaging