Skid Steer Snow Plows Market Size, Share, and Trends Analysis Report

CAGR :

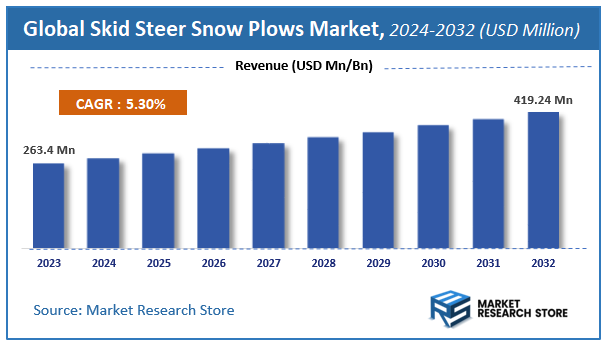

| Market Size 2023 (Base Year) | USD 263.4 Million |

| Market Size 2032 (Forecast Year) | USD 419.24 Million |

| CAGR | 5.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Skid Steer Snow Plows Market Insights

According to Market Research Store, the global skid steer snow plows market size was valued at around USD 263.4 million in 2023 and is estimated to reach USD 419.24 million by 2032, to register a CAGR of approximately 5.3% in terms of revenue during the forecast period 2024-2032.

The skid steer snow plows report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032

To Get more Insights, Request a Free Sample

Global Skid Steer Snow Plows Market: Overview

A skid steer snow plow is an attachment designed for skid steer loaders, commonly used in snow removal operations. The plow is mounted to the front of the skid steer and is ideal for clearing snow from driveways, roads, parking lots, and other outdoor surfaces. Skid steer snow plows come in various sizes and configurations, with options such as straight blades, V-shaped blades, or angle blades, providing versatility for different snow removal tasks. These attachments are popular due to their high maneuverability, efficiency, and ability to handle various snow depths and terrain types.

Key Highlights

- The skid steer snow plows market is anticipated to grow at a CAGR of 5.3% during the forecast period.

- The global skid steer snow plows market was estimated to be worth approximately USD 263.4 million in 2023 and is projected to reach a value of USD 419.24 million by 2032.

- The growth of the skid steer snow plows market is being driven by increasing frequency of harsh winter conditions in regions prone to heavy snowfall.

- Based on the product type, the standard snow plows segment is growing at a high rate and is projected to dominate the market.

- On the basis of drive system, the hydraulic systems segment is projected to swipe the largest market share.

- In terms of blade material, the steel blades segment is expected to dominate the market.

- Based on the application, the commercial use segment is expected to dominate the market.

- In terms of control type, the manual-controlled plows segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Skid Steer Snow Plows Market: Dynamics

Key Growth Drivers:

- Rising Demand for Efficient Snow Removal: The increasing frequency and severity of winter storms in various regions are pushing municipalities, commercial establishments, and individuals to invest in efficient snow removal equipment, including skid steer snow plows.

- Versatility of Skid Steers: Skid steers are compact, versatile machines that can be easily equipped with various attachments, including snow plows, making them ideal for a wide range of snow removal tasks in both residential and commercial sectors.

- Growth in Construction and Landscaping Sectors: The expansion of the construction and landscaping industries, where snow removal is an essential service, is contributing to the rising adoption of skid steer snow plows as these industries look for efficient and cost-effective solutions.

- Increase in Winter Tourism and Recreational Activities: The growth in winter tourism and recreational activities, such as skiing and snowboarding, demands efficient snow clearing to maintain safe and accessible pathways, driving the need for skid steer snow plows.

- Technological Advancements: Innovations in skid steer designs and snow plow attachments, such as enhanced hydraulics, improved durability, and automation, are encouraging more businesses and municipalities to adopt these machines for snow removal.

Restraints:

- High Initial Cost of Equipment: The upfront cost of skid steer snow plows, especially when considering the skid steer itself and the required attachments, can be high, particularly for small businesses or individuals with limited budgets.

- Maintenance and Operational Costs: Skid steers require regular maintenance and can have high operational costs, especially in harsh winter conditions, which may deter smaller operators from purchasing or leasing the equipment.

- Seasonal Demand Fluctuations: The demand for skid steer snow plows is highly seasonal, primarily peaking in winter months. This fluctuation in demand can create challenges for manufacturers, suppliers, and operators who need to balance equipment utilization and profitability during off-seasons.

- Environmental Impact and Regulations: Growing environmental concerns regarding emissions and fuel consumption associated with traditional skid steers may lead to stricter regulations and the need for more eco-friendly solutions, which could increase costs for manufacturers and users.

Opportunities:

- Expansion in Emerging Markets: As winter-related services and infrastructure develop in emerging markets, there is significant growth potential for skid steer snow plows, especially in countries experiencing their first major snowfall events.

- Demand for Electric and Hybrid Models: With increasing awareness about environmental sustainability, the market for electric or hybrid skid steers and snow plows is expanding. These models offer lower operational costs and reduce environmental impact, appealing to businesses looking to align with green initiatives.

- Integration of GPS and Automation: The integration of GPS technology and automation in snow plows can provide precise control and improve efficiency in snow removal. This is an opportunity for manufacturers to innovate and create advanced systems that appeal to large-scale municipal and commercial customers.

- Rental Services and Leasing Models: With the high upfront costs, offering skid steer snow plows on a rental or lease basis presents an opportunity for businesses to target customers who need the equipment on a seasonal or short-term basis.

Challenges:

- Competition from Alternative Snow Removal Equipment: The presence of alternative snow removal solutions, such as traditional snow plows, snow blowers, and larger vehicles, may limit the market share growth for skid steer snow plows, especially in certain regions or applications.

- Shortage of Skilled Operators: Operating skid steers efficiently requires skilled operators, and there is a shortage of trained personnel. This can create challenges for businesses looking to maintain a fleet of snow removal equipment.

- Unpredictability of Weather Patterns: Climate change and the unpredictability of winter weather can make it difficult for businesses and municipalities to plan their snow removal operations, affecting long-term investment in skid steer snow plows.

- Regulatory Compliance: As snow removal becomes an increasingly critical service in urban areas, regulations regarding the efficiency, emissions, and operational safety of skid steer snow plows may become stricter, posing compliance challenges for manufacturers and users.

Skid Steer Snow Plows Market: Report Scope

This report thoroughly analyzes the Skid Steer Snow Plows Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Skid Steer Snow Plows Market |

| Market Size in 2023 | USD 263.4 Million |

| Market Forecast in 2032 | USD 419.24 Million |

| Growth Rate | CAGR of 5.3% |

| Number of Pages | 197 |

| Key Companies Covered | Douglas Dynamics, BOSS, Meyer Products, SnowEx, Kage, SNO-WAY, Hiniker Company, Construction Implements Depot, Titan Implement, Metal Pless, Truck Utilities, T.C. Winter Servicesa |

| Segments Covered | By Product Type, By Drive System, By Blade Material, By Application, By Control Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Skid Steer Snow Plows Market: Segmentation Insights

The global skid steer snow plows market is divided by product type, drive system, application, blade material, control type, and region.

Segmentation Insights by Product Type

Based on product type, the global skid steer snow plows market is divided into standard snow plows, v-plows, box plows, universal mount plows, and heavy-duty plows.

In the skid steer snow plows market, the most dominant product type is the Standard Snow Plows. These plows are widely used for general snow clearing due to their simplicity, affordability, and effectiveness. They are typically straight blades and are easy to attach and maneuver, making them a popular choice for both residential and commercial snow clearing. Their versatility in handling a wide range of snow depths and their ability to clear moderate snowfall contribute to their dominance in the market.

The next most significant segment is V-Plows. V-plows are designed to handle larger amounts of snow with more precision, thanks to their unique V-shaped design that allows for better snow management. These plows are particularly effective in severe snow conditions, such as heavy or wet snow, where a more aggressive plow is necessary. Their ability to open up snowbanks and efficiently move snow to the sides gives them an edge in more demanding snow removal tasks.

Box Plows come next in terms of market share. These plows feature a large enclosed blade design that can contain and move larger volumes of snow at once, making them ideal for clearing wide areas, parking lots, and roads. Their design allows for more effective snow containment, preventing snow from spilling over the sides. While they are effective in heavy snow conditions, their use is typically more specialized compared to standard or V-plows, which limits their dominance in the overall market.

Following Box Plows, Universal Mount Plows hold a smaller share. These plows are designed for use with multiple machines, offering flexibility in deployment. However, while they provide adaptability across different vehicles, their less specialized design and the increased need for customization make them less popular than more dedicated plow types like Standard Snow Plows or V-Plows.

Finally, Heavy-Duty Plows represent the least dominant segment. These plows are built for extreme snow removal needs, such as in industrial applications or large-scale snow clearing operations. While they offer significant power and durability, their higher cost and niche application reduce their widespread use compared to other plow types. These plows are often used by municipalities or large snow removal companies rather than smaller contractors or homeowners.

Segmentation Insights by Drive System

On the basis of drive system, the global skid steer snow plows market is bifurcated into hydraulic systems, mechanical systems, and electric systems.

In the skid steer snow plows market, the Hydraulic Systems segment is the most dominant. Hydraulic systems are widely used in skid steer snow plows due to their powerful, efficient, and smooth operation. The ability to control the plow’s movement (such as lifting, tilting, and angling) with precision is a significant advantage, making them ideal for heavy-duty snow clearing. Hydraulically powered plows offer excellent responsiveness and durability, which makes them the preferred choice for both commercial and residential snow clearing operations. Their versatility in handling different snow depths and conditions contributes to their strong market position.

The Mechanical Systems segment comes next in terms of market share. These systems use mechanical linkages and gears to control the movement of the plow. While not as versatile or precise as hydraulic systems, mechanical systems are simpler and less expensive to maintain. They are often found in smaller or budget-conscious snow plows, where advanced hydraulic features are not necessary. While mechanical systems may not offer the same level of efficiency in heavy snow conditions, they are a solid choice for lighter or occasional snow clearing tasks.

Lastly, the Electric Systems segment represents a smaller share of the market. Electric systems are newer and offer a more environmentally friendly alternative to hydraulic and mechanical systems. They are typically used in smaller snow plows, as electric motors can provide enough power for lighter snow removal tasks. One of the advantages of electric systems is their quieter operation and lower environmental impact. However, the range of operation and power required for large-scale snow clearing are limitations for electric systems, making them less dominant in comparison to hydraulic and mechanical systems.

Segmentation Insights by Blade Material

Based on blade material, the global skid steer snow plows market is divided into steel blades, polyethylene blades, rubber blades, and composite blades.

In the skid steer snow plows market, Steel Blades are the most dominant segment. Steel is the traditional and most widely used material for snow plow blades due to its strength, durability, and ability to handle heavy-duty tasks. Steel blades are highly effective at cutting through dense, compacted snow and ice, making them ideal for clearing large areas such as roads, parking lots, and industrial spaces. They are well-suited for both light and heavy snow conditions, which contributes to their dominance in the market. Steel’s resistance to wear and tear, as well as its relatively low maintenance requirements, makes it the preferred choice for commercial and municipal snow clearing.

Next, Polyethylene Blades hold a significant share in the market. These blades are lightweight, resistant to corrosion, and less prone to damage from rough surfaces compared to steel. Polyethylene blades are particularly effective in situations where there is a need to protect the surface being cleared, such as on delicate or newly paved roads and driveways. They also offer quieter operation compared to steel blades and are less likely to cause damage to the underlying surface. Although polyethylene blades are not as durable as steel in extreme conditions, they are favored in residential or light commercial snow removal applications where surface protection is a priority.

Rubber Blades are another important segment, particularly valued for their flexibility and ability to clear snow without damaging delicate surfaces. Rubber blades provide a gentler touch and are often used in areas where the risk of surface damage is a concern, such as parking lots, driveways, or areas with fragile asphalt. These blades can adapt to uneven surfaces, providing efficient snow removal while minimizing surface wear. While rubber blades are effective in certain environments, their performance in heavy snow and ice conditions can be limited compared to steel or polyethylene blades, reducing their market share.

Finally, Composite Blades represent a smaller segment. These blades are made from a combination of materials, such as fiberglass or plastic reinforced with other substances, designed to offer a balance of durability, weight, and flexibility. Composite blades are often used in specialized applications, where their unique properties—such as being lighter than steel but more durable than rubber—make them a good option. However, due to their higher cost and niche use cases, they hold a smaller market share compared to steel, polyethylene, and rubber blades.

Segmentation Insights by Application

On the basis of application, the global skid steer snow plows market is bifurcated into commercial use, residential use, agricultural use, and infrastructure maintenance.

In the skid steer snow plows market, Commercial Use is the most dominant application segment. This includes snow removal for businesses, parking lots, roadways, and larger commercial properties. The need for efficient, heavy-duty snow removal in these areas drives the demand for skid steer snow plows. Commercial operations require powerful and versatile snow plows that can handle large volumes of snow in a variety of conditions, making them the primary market for these products. The increased demand for snow removal services during the winter months further fuels the growth of this segment.

Infrastructure Maintenance follows closely as a significant application segment. Snow removal in public infrastructure areas such as highways, streets, and municipal facilities is essential for maintaining access and safety during winter months. Government agencies and contractors use skid steer snow plows for routine maintenance of public roads and pathways. These plows must be durable and efficient enough to handle the challenges of larger, heavily trafficked areas. Infrastructure maintenance accounts for a considerable share of the market due to the need for year-round snow clearing services in various weather conditions.

Next is Residential Use, which represents a growing segment, especially in regions with heavy snowfall. Homeowners, particularly in suburban and rural areas, rely on skid steer snow plows to clear driveways, walkways, and private roads. The need for efficient snow removal equipment is particularly prominent in residential areas with frequent snowfalls. Although this segment does not match the commercial or infrastructure markets in terms of overall volume, the increasing number of individuals and small businesses investing in snow clearing equipment for personal or light commercial use drives its steady growth.

Finally, Agricultural Use is the smallest application segment for skid steer snow plows. Agricultural areas, especially those with large properties and farms, occasionally require snow removal for access to fields, barns, and other facilities. However, the need for skid steer snow plows in agriculture is more specialized compared to commercial or infrastructure applications. Snow clearing on farms tends to be less frequent and less intensive, which is why this segment remains the least dominant in the market. Still, it holds significance in areas with large agricultural operations that experience heavy winter snowfall.

Segmentation Insights by Control Type

On the basis of control type, the global skid steer snow plows market is bifurcated into manual-controlled plows, remote-controlled plows, and automated plowing systems.

In the skid steer snow plows market, Manual-Controlled Plows are the most dominant control type. These plows are the traditional option and remain highly popular due to their simplicity, reliability, and affordability. Manual-controlled plows require the operator to physically control the movement of the blade, typically using levers or hydraulic controls within the cab of the skid steer. Despite the rise of more advanced systems, manual-controlled plows continue to dominate due to their ease of use and cost-effectiveness, making them a common choice for both residential and commercial snow clearing operations.

Remote-Controlled Plows are the next most significant segment in the market. These plows offer the advantage of allowing the operator to control the plow from a distance, which can be especially useful for accessing difficult or hazardous areas, such as tight spaces or locations where the operator cannot be in close proximity to the machine. Remote-controlled plows are popular in more specialized commercial snow removal applications where flexibility and safety are important. While they provide greater ease of operation, they come at a higher cost and require a skilled operator, which limits their market share compared to manual-controlled plows.

Automated Plowing Systems represent the least dominant control type in the market, but they are gradually gaining attention as technology advances. Automated systems use sensors, GPS, and software to control the plow's movement and optimize snow removal processes. These systems are designed to reduce the need for operator intervention, making them particularly attractive for large-scale commercial or infrastructure snow clearing operations. Automated plowing systems can improve efficiency, reduce labor costs, and enhance safety by minimizing human error. However, the high initial investment, complexity of the technology, and ongoing maintenance requirements make these systems less common in the overall market, especially for smaller or less demanding snow clearing tasks.

Skid Steer Snow Plows Market: Regional Insights

- North America is expected to dominates the global market

The North America region is the most dominant in the skid steer snow plow market, driven by the United States and Canada. The demand is bolstered by consistent snowfall and the need for municipalities and private businesses to maintain road safety during harsh winter conditions. The established infrastructure and high levels of investment in snow removal equipment make this region a leader in the market.

Europe follows closely in demand, particularly in countries like Germany, France, and the Nordic nations. These countries place a strong emphasis on infrastructure maintenance and snow removal during winter, creating significant demand for efficient snow plowing equipment. Strict safety regulations and frequent snowfall in these regions further contribute to the growth of the market.

The Asia Pacific region is experiencing rapid growth in the skid steer snow plow market, especially in Japan, South Korea, and parts of China. Increasing urbanization, along with infrastructure development and greater awareness of winter road safety, are driving the market's expansion. Though snowfall is less frequent in some areas, the demand for snow plows is on the rise due to changing weather patterns and improved urban planning.

In Latin America, the adoption of skid steer snow plows is relatively limited, though countries like Brazil and Argentina are gradually increasing their usage. Snowfall is less frequent compared to other regions, but urbanization and infrastructure development in certain areas are gradually boosting the demand for snow removal solutions.

The Middle East and Africa region exhibits the lowest demand for skid steer snow plows, largely due to the generally warm climate across most of the region. However, there are areas with occasional snowfall or specific needs that are beginning to explore snow removal technologies, albeit at a smaller scale compared to other regions.

Skid Steer Snow Plows Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the skid steer snow plows market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global skid steer snow plows market include:

- Douglas Dynamics

- BOSS

- Meyer Products

- SnowEx

- Kage

- SNO-WAY

- Hiniker Company

- Construction Implements Depot

- Titan Implement

- Metal Pless

- Truck Utilities

- T.C. Winter Servicesa

The global skid steer snow plows market is segmented as follows:

By Product Type

- Standard Snow Plows

- V-Plows

- Box Plows

- Universal Mount Plows

- Heavy-Duty Plows

By Drive System

- Hydraulic Systems

- Mechanical Systems

- Electric Systems

By Blade Material

- Steel Blades

- Polyethylene Blades

- Rubber Blades

- Composite Blades

By Application

- Commercial Use

- Residential Use

- Agricultural Use

- Infrastructure Maintenance

By Control Type

- Manual-Controlled Plows

- Remote-Controlled Plows

- Automated Plowing Systems

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Skid Steer Snow Plows

Request Sample

Skid Steer Snow Plows