Synthetic Lethality-based Drugs and Targets Market Size, Share, and Trends Analysis Report

CAGR :

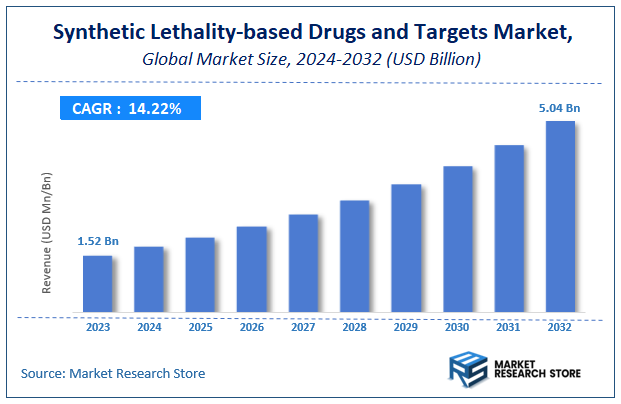

| Market Size 2023 (Base Year) | USD 1.52 Billion |

| Market Size 2032 (Forecast Year) | USD 5.04 Billion |

| CAGR | 14.22% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Synthetic Lethality-based Drugs and Targets Market Insights

According to Market Research Store, the global synthetic lethality-based drugs and targets market size was valued at around USD 1.52 billion in 2023 and is estimated to reach USD 5.04 billion by 2032, to register a CAGR of approximately 14.22% in terms of revenue during the forecast period 2024-2032.

The synthetic lethality-based drugs and targets report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Synthetic Lethality-based Drugs and Targets Market: Overview

Synthetic lethality is a cutting-edge concept in cancer therapeutics that involves targeting gene pairs where the simultaneous impairment of both genes leads to cell death, while the dysfunction of only one gene does not. In cancer cells, certain tumor suppressor genes are often mutated or inactivated. By identifying and targeting their synthetic lethal partners—genes that are essential only in the context of the mutation—researchers can develop drugs that selectively kill cancer cells while sparing healthy ones. This precision approach reduces side effects and enhances treatment efficacy. A well-known example is the use of PARP inhibitors like olaparib in BRCA1/2-mutant cancers, which has validated the clinical potential of synthetic lethality strategies.

Key Highlights

- The synthetic lethality-based drugs and targets market is anticipated to grow at a CAGR of 14.22% during the forecast period.

- The global synthetic lethality-based drugs and targets market was estimated to be worth approximately USD 1.52 billion in 2023 and is projected to reach a value of USD 5.04 billion by 2032.

- The growth of the synthetic lethality-based drugs and targets market is being driven by advancements in functional genomics, CRISPR screening technologies, and bioinformatics platforms.

- Based on the Drug Type, the small molecule drugs segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the cancer segment is projected to swipe the largest market share.

- In terms of end-user, the pharmaceutical companies segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Synthetic Lethality-based Drugs and Targets Market: Dynamics

Key Growth Drivers:

- Rising Prevalence of Cancer: The growing global cancer burden has intensified the need for targeted therapies like synthetic lethality-based drugs, which selectively kill cancer cells without harming healthy tissue.

- Advancements in Genomic and CRISPR Technologies: Enhanced genomic screening and gene-editing tools, particularly CRISPR, have accelerated the discovery of synthetic lethal gene pairs and validated new drug targets.

- Increased R&D Investment in Precision Medicine: Pharmaceutical companies and research institutions are heavily investing in personalized medicine approaches, supporting the development of synthetic lethality-based therapeutics.

- Positive Clinical Outcomes of PARP Inhibitors: The success of PARP inhibitors (like olaparib) in treating BRCA-mutated cancers has validated the synthetic lethality approach, driving further innovation and market confidence.

- Government and Regulatory Support for Oncology Innovation: Public funding, expedited approval pathways, and orphan drug designations are encouraging the development of novel cancer therapies based on synthetic lethality.

Restraints:

- Limited Understanding of Synthetic Lethal Interactions in Humans: Despite promising preclinical data, translating synthetic lethal interactions into safe and effective therapies in humans remains complex and poorly understood.

- High Cost and Time-Intensive Drug Development: Developing synthetic lethality-based drugs requires extensive genomic analysis, target validation, and clinical trials, making the process costly and lengthy.

- Resistance Mechanisms in Tumors: Cancer cells may develop resistance to synthetic lethality-based treatments, limiting long-term effectiveness and requiring combination or backup therapies.

Opportunities:

- Expansion into Non-Oncology Therapeutic Areas: While most applications are currently in oncology, there is growing potential for synthetic lethality in neurodegenerative and infectious diseases.

- Emerging Biomarker Discovery Platforms: New biomarker technologies are improving the identification of patient populations likely to respond to synthetic lethality-based therapies, enabling more precise treatments.

- Collaborations Between Academia and Industry: Partnerships among biotech firms, pharma companies, and research institutions are accelerating discovery pipelines and commercial development.

- Growing Interest in Next-Generation Synthetic Lethality Approaches: Beyond PARP inhibitors, novel targets such as ATR, WEE1, and DNA polymerases are drawing attention, expanding the scope of future drug development.

Challenges:

- Complexity of Target Validation and Drug Delivery: Verifying synthetic lethal gene pairs and ensuring efficient delivery of drugs to target tissues remain significant scientific and technical challenges.

- Regulatory Uncertainty for Novel Mechanisms: As synthetic lethality is a relatively new therapeutic approach, regulatory frameworks are still evolving, which may delay approvals or raise barriers.

- Limited Awareness Among Clinicians: Many healthcare providers are not yet fully familiar with synthetic lethality-based treatments, potentially slowing adoption and integration into standard care.

- Data Privacy and Ethical Issues in Genomic Profiling: As synthetic lethality strategies often rely on patient-specific genetic information, privacy concerns and ethical considerations may impact patient participation and data use.

Synthetic Lethality-based Drugs and Targets Market: Report Scope

This report thoroughly analyzes the Synthetic Lethality-based Drugs and Targets Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Synthetic Lethality-based Drugs and Targets Market |

| Market Size in 2023 | USD 1.52 Billion |

| Market Forecast in 2032 | USD 5.04 Billion |

| Growth Rate | CAGR of 14.22% |

| Number of Pages | 165 |

| Key Companies Covered | AbbVie, AstraZeneca, BeiGene, Clovis Oncology, GlaxoSmithKline, Pfizer, AtlasMedx, Chordia Therapeutics, IDEAYA Biosciences, Mission Therapeutics, Repare Therapeutics, Sierra Oncology, SyntheX Labs |

| Segments Covered | By Drug Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Synthetic Lethality-based Drugs and Targets Market: Segmentation Insights

The global synthetic lethality-based drugs and targets market is divided by drug type, application, end-user, and region.

Segmentation Insights by Drug Type

Based on drug type, the global synthetic lethality-based drugs and targets market is divided into small molecule drugs and biologic drugs.

In the synthetic lethality-based drugs and targets market, small molecule drugs represent the most dominant segment by drug type. These compounds are favored for their ease of production, relatively lower cost, and well-established development pathways. Small molecules are typically administered orally and can easily penetrate cell membranes, making them effective in targeting intracellular pathways involved in synthetic lethality mechanisms. Their ability to interfere with specific proteins or enzymes involved in DNA repair pathways — such as PARP inhibitors used in BRCA-mutated cancers — has positioned them as the frontrunners in this emerging therapeutic field. Furthermore, the availability of high-throughput screening technologies has accelerated the identification of potential synthetic lethality targets suitable for small molecule intervention, further fueling their dominance.

On the other hand, biologic drugs — which include monoclonal antibodies, therapeutic proteins, and gene therapies — constitute a growing but currently less dominant segment. Biologics are often more specific in their mechanism of action and can engage targets that are not easily accessible to small molecules, such as extracellular proteins or complex signaling cascades. Their role in synthetic lethality is still evolving, particularly in the context of precision oncology and immune-based strategies. However, challenges such as high manufacturing costs, delivery complexities, and stringent regulatory requirements have somewhat limited their widespread adoption compared to small molecules. Despite this, advancements in biotechnology and a deeper understanding of tumor genomics are expected to enhance the role of biologics in the synthetic lethality market over time.

Segmentation Insights by Application

On the basis of application, the global synthetic lethality-based drugs and targets market is bifurcated into cancer, neurodegenerative diseases, infectious diseases, and others.

In the synthetic lethality-based drugs and targets market, cancer stands out as the most dominant application segment. The concept of synthetic lethality was first explored and validated extensively in oncology, especially with the development of PARP inhibitors for BRCA1/2-mutated cancers. Cancer cells often harbor genetic defects that make them more reliant on specific DNA repair pathways for survival. Targeting these compensatory pathways through synthetic lethal interactions allows for highly selective killing of cancer cells while sparing normal cells, making it an ideal strategy in precision oncology. As a result, significant research funding, clinical trial activity, and pharmaceutical investment have been directed toward cancer applications, solidifying its leading position in the market.

Neurodegenerative diseases represent a promising but less dominant segment. Synthetic lethality is being explored in this space to uncover gene interactions that may mitigate the effects of mutations associated with conditions like ALS, Alzheimer’s, and Parkinson’s disease. While still in early stages of development, the potential to identify pathways that promote neuronal survival or prevent toxic protein accumulation is attracting growing interest. However, due to the complex nature of these diseases and the challenges of crossing the blood-brain barrier, progress has been slower compared to cancer.

Infectious diseases are an emerging area of application for synthetic lethality. Researchers are investigating synthetic lethal interactions in pathogens or between host and pathogen to identify novel antimicrobial targets, especially in the face of rising antibiotic resistance. Although the potential is significant, this application is still nascent, with fewer validated targets and clinical candidates compared to cancer.

Segmentation Insights by End-User

On the basis of end-user, the global synthetic lethality-based drugs and targets market is bifurcated into pharmaceutical companies, biotechnology companies, research institutes, and contract research organizations (CROs).

In the synthetic lethality-based drugs and targets market, pharmaceutical companies represent the most dominant end-user segment. These companies possess the financial resources, infrastructure, and regulatory expertise necessary to drive synthetic lethality programs from discovery through clinical development and commercialization. The success of PARP inhibitors has encouraged many major pharmaceutical firms to invest heavily in this area, often through collaborations with biotech startups or academic institutions. Their focus is primarily on translating synthetic lethality discoveries into viable therapeutics, particularly in oncology, where clinical pipelines are increasingly being populated with synthetic lethality-based drug candidates.

Biotechnology companies form the second most dominant segment, playing a crucial role in innovation and early-stage development. These companies are often at the forefront of discovering novel synthetic lethal gene interactions and developing next-generation tools like CRISPR-based screening and functional genomics platforms. Due to their agility and focus on cutting-edge science, biotech firms frequently partner with larger pharmaceutical companies to advance promising leads into clinical trials. Their contributions are instrumental in expanding the scope of synthetic lethality beyond cancer into other therapeutic areas.

Research institutes are essential drivers of basic and translational research in synthetic lethality, though they are less dominant in terms of market influence. These academic and government-funded institutions conduct foundational studies to uncover gene-gene interactions and biological mechanisms underlying synthetic lethality. Their findings often serve as the basis for drug development by pharma and biotech companies. While research institutes are not directly involved in commercialization, their work is vital in shaping the future direction of the market.

Contract Research Organizations (CROs) represent the least dominant segment but play a supportive and increasingly valuable role. CROs provide outsourced services such as high-throughput screening, biomarker discovery, and preclinical or clinical trial management. As the demand for synthetic lethality-focused drug development grows, CROs are expanding their capabilities in this area. However, their role is more auxiliary compared to the other end-users, contributing indirectly to the market by enabling faster and more cost-effective research and development.

Synthetic Lethality-based Drugs and Targets Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the synthetic lethality-based drugs and targets market. This leadership is driven by a strong foundation in genomic research, significant investment in biotechnology, and a high burden of cancer cases. The United States plays a central role, with active clinical trial pipelines, substantial support from public and private sectors, and a regulatory environment that encourages fast-track development and approval of novel therapies. The region’s emphasis on personalized medicine and cutting-edge oncology practices further solidifies its leading position.

Europe follows North America in market dominance, supported by a growing focus on precision medicine and supportive healthcare policies. Countries like the United Kingdom, Germany, and France are spearheading advancements through strategic collaborations, government funding, and an increase in clinical research. The region’s infrastructure for genomic and cancer research, coupled with efforts to integrate advanced therapies into standard care, supports its strong presence in this market.

Asia Pacific is showing rapid growth in the synthetic lethality-based drugs and targets market, propelled by increasing healthcare investments, rising cancer prevalence, and advancements in biotechnology. Countries such as China, Japan, and India are enhancing research capabilities and building partnerships with international pharmaceutical companies. The region’s adoption of genomic diagnostics and focus on precision oncology are creating new opportunities for market expansion.

Latin America is gradually emerging in this space, with countries like Brazil and Argentina investing in healthcare improvements and expanding access to advanced treatments. The region is beginning to adopt precision medicine frameworks, and initiatives such as government-backed cancer programs and international collaborations are helping to drive awareness and market penetration.

Middle East and Africa represent the least dominant region, but it is experiencing steady growth due to increasing investments in healthcare infrastructure and rising interest in innovative oncology solutions. Efforts to improve access to molecular diagnostics and targeted therapies, along with regional collaborations, are slowly transforming the landscape and enhancing the region’s potential in the synthetic lethality-based market.

Synthetic Lethality-based Drugs and Targets Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the synthetic lethality-based drugs and targets market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global synthetic lethality-based drugs and targets market include:

- AbbVie

- AstraZeneca

- BeiGene

- Clovis Oncology

- GlaxoSmithKline

- Pfizer

- AtlasMedx

- Chordia Therapeutics

- IDEAYA Biosciences

- Mission Therapeutics

- Repare Therapeutics

- Sierra Oncology

- SyntheX Labs

The global synthetic lethality-based drugs and targets market is segmented as follows:

By Drug Type

- Small Molecule Drugs

- Biologic Drugs

By Application

- Cancer

- Neurodegenerative Diseases

- Infectious Diseases

- Others

By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Research Institutes

- Contract Research Organizations (CROs)

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

.

Frequently Asked Questions

What will be the value of the Synthetic Lethality-based Drugs and Targets market during 2024 - 2032?

Table Of Content

Inquiry For Buying

Synthetic Lethality-based Drugs and Targets

Request Sample

Synthetic Lethality-based Drugs and Targets