Telecom Connector and Datacom Connector Market Size, Share, and Trends Analysis Report

CAGR :

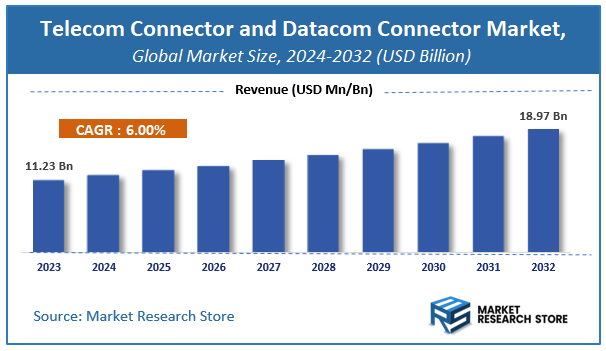

| Market Size 2023 (Base Year) | USD 11.23 Billion |

| Market Size 2032 (Forecast Year) | USD 18.97 Billion |

| CAGR | 6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Telecom Connector and Datacom Connector Market Insights

According to Market Research Store, the global telecom connector and datacom connector market size was valued at around USD 11.23 billion in 2023 and is estimated to reach USD 18.97 billion by 2032, to register a CAGR of approximately 6% in terms of revenue during the forecast period 2024-2032.

The telecom connector and datacom connector report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Telecom Connector and Datacom Connector Market: Overview

Telecom connector and datacom connector are critical components used to establish reliable electrical or optical signal transmission in telecommunications and data communication networks. These connectors serve as interfaces between cables and devices, enabling seamless transmission of voice, video, and data signals. Telecom connectors are primarily used in voice and long-distance communication systems, while datacom connectors are designed for high-speed data transfer in local area networks (LANs), data centers, and enterprise IT environments. Common types include RJ-11 and RJ-45 connectors, fiber optic connectors (LC, SC, ST), coaxial connectors, and modular jacks and plugs.

The growth of the telecom connector and datacom connector market is driven by the increasing global demand for high-speed internet, the expansion of 5G infrastructure, rising data traffic, and the proliferation of cloud computing and IoT devices. As networks require greater bandwidth, reliability, and signal integrity, connector designs are evolving to support higher data rates, reduce latency, and ensure secure connections in harsh or high-density environments. Additionally, trends like network virtualization, edge computing, and the modernization of telecom infrastructure across both developed and emerging economies continue to fuel investment in advanced connectivity solutions, positioning telecom and datacom connectors as foundational enablers of next-generation communication systems.

Key Highlights

- The telecom connector and datacom connector market is anticipated to grow at a CAGR of 6% during the forecast period.

- The global telecom connector and datacom connector market was estimated to be worth approximately USD 11.23 billion in 2023 and is projected to reach a value of USD 18.97 billion by 2032.

- The growth of the telecom connector and datacom connector market is being driven by the explosive expansion of global data traffic and the increasing demand for high-speed, reliable connectivity.

- Based on the type, the fiber optic connectors segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the telecommunications segment is projected to swipe the largest market share.

- In terms of end-user, the enterprises segment is expected to dominate the market.

- Based on the configuration, the modular connectors segment is expected to dominate the market.

- Based on the material, the plastic connectors segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Telecom Connector and Datacom Connector Market: Dynamics

Key Growth Drivers:

- Rapid Expansion of 5G Network Infrastructure: The global rollout of 5G networks is a primary driver. 5G requires significantly denser network architectures, more base stations, and increased fiber optic deployments, all of which necessitate a massive demand for high-performance, high-frequency, and robust connectors (especially fiber optic and RF coaxial connectors).

- Proliferation of IoT Devices and Applications: The increasing adoption of IoT devices across various industries (smart homes, industrial IoT, smart cities, connected vehicles) generates enormous amounts of data. This drives the need for reliable and high-speed connectivity solutions, boosting the demand for compact, efficient, and durable connectors for sensors, edge devices, and network infrastructure.

- Explosive Growth in Data Traffic and Bandwidth Requirements: The continuous surge in internet usage, cloud computing, video streaming, online gaming, and big data analytics demands ever-increasing bandwidth and faster data transfer rates. This fuels the need for advanced connectors capable of handling higher frequencies, minimizing signal loss, and supporting next-generation networking standards.

- Expansion of Data Centers and Cloud Infrastructure: The continuous growth of hyperscale and enterprise data centers, driven by cloud adoption and AI/ML workloads, requires vast numbers of high-speed, high-density connectors (e.g., fiber optic, PCB, and backplane connectors) for servers, switches, and storage systems to ensure efficient and reliable data flow.

- Digital Transformation Across Industries: Industries are undergoing digital transformation, adopting automation, Industry 4.0 practices, and integrated IT systems. This necessitates robust and reliable connectivity solutions for industrial control systems, robotics, smart manufacturing, and logistics, driving the demand for specialized industrial-grade telecom and datacom connectors.

- Growing Demand for Fiber Optic Connectivity: Fiber optic cables are becoming the backbone for high-speed communication due to their superior bandwidth, longer transmission distances, and immunity to electromagnetic interference. The increasing deployment of Fiber-to-the-Home/Business (FTTH/FTTB) and fiber optic backbones for 5G drives significant demand for fiber optic connectors (e.g., LC, SC, MPO/MTP).

- Technological Advancements in Connector Design: Ongoing innovation in connector technology, including miniaturization, higher contact density, improved signal integrity, enhanced thermal management, and ruggedized designs for harsh environments, expands their application scope and boosts market growth.

Restraints:

- Price Pressure and Commoditization of Standard Connectors: For common or older-generation connectors, intense competition among manufacturers can lead to price wars and commoditization, impacting profit margins for companies that do not differentiate with advanced or specialized products.

- Supply Chain Volatility and Raw Material Price Fluctuations: The market is susceptible to disruptions in global supply chains (as seen during the pandemic) and volatility in raw material prices (e.g., copper, plastics, precious metals). These factors can lead to increased production costs, extended lead times, and unstable pricing, affecting market stability.

- Rapid Technological Obsolescence: The rapid pace of technological advancements in telecom and datacom (e.g., from 4G to 5G, then 6G, and new Ethernet standards) means that connector designs can become obsolete quickly. This requires continuous R&D investment and can lead to shorter product lifecycles, challenging manufacturers to keep pace.

- Complex Certification and Standardization Processes: Connectors used in critical telecom and datacom infrastructure must meet stringent industry standards and certifications to ensure interoperability, reliability, and performance. Navigating these complex and often evolving regulatory frameworks can be time-consuming and costly.

- Integration Challenges with Legacy Infrastructure: Many existing telecom and datacom networks still rely on older infrastructure. Integrating new, high-speed connector technologies with these legacy systems can be complex and costly, hindering rapid upgrades.

- Impact of Global Economic Downturns: The market is closely tied to capital expenditures by telecom operators, data center builders, and enterprises. Economic downturns or reduced investment in infrastructure development can directly impact the demand for connectors.

Opportunities:

- Development of 6G Technology and Beyond: The research and development into 6G networks, anticipated to be significantly faster and more pervasive than 5G, will create a massive opportunity for entirely new generations of ultra-high-speed, high-frequency, and highly integrated connectors.

- Edge Computing and Distributed Data Centers: The shift towards edge computing, bringing data processing closer to the source, will drive demand for specialized, robust, and compact connectors suitable for smaller, distributed data centers and edge devices, often operating in less controlled environments.

- Deployment of Private 5G Networks: Industries are increasingly deploying private 5G networks for enhanced security, low latency, and tailored connectivity within their facilities. This creates a dedicated market for telecom and datacom connectors for industrial automation, smart manufacturing, and logistics.

- Advancements in Optical-Electrical Hybrid Connectors: The increasing convergence of optical and electrical signals, especially in data centers and high-speed networks, will drive the demand for hybrid connectors that can efficiently manage both power and optical data transmission in a single form factor.

- Miniaturization and Higher Density Connectors: The ongoing trend towards smaller electronic devices and higher port density in network equipment creates opportunities for connectors that offer increased performance in smaller footprints, enabling more compact and efficient designs.

- Automotive Ethernet and In-Vehicle Networking: The growing complexity of vehicle electronics, connected cars, and autonomous driving necessitates high-speed, reliable datacom connectors for in-vehicle networks, camera systems, and infotainment, representing a significant long-term growth opportunity.

- Focus on Sustainability and Green Connectors: Developing energy-efficient connectors, using sustainable materials, and improving recyclability will be a growing opportunity as industries increasingly prioritize environmental, social, and governance (ESG) goals.

Challenges:

- Managing Rapid Product Development Cycles: The need to continuously innovate and shorten product development cycles to keep pace with evolving industry standards (e.g., PCIe generations, Ethernet speeds) is a significant challenge for connector manufacturers.

- Ensuring Signal Integrity at Higher Speeds: As data rates increase, maintaining signal integrity becomes incredibly challenging. Connectors must be designed to minimize signal loss, crosstalk, and electromagnetic interference (EMI) at ever-higher frequencies.

- Talent Shortage in R&D and Manufacturing: The development and production of advanced connectors require specialized expertise in materials science, electrical engineering, and precision manufacturing. Attracting and retaining skilled talent in these areas is a continuous challenge.

- Addressing Thermal Management Issues: Higher data rates and increased power delivery through connectors can lead to significant heat generation. Designing connectors with effective thermal management capabilities to prevent performance degradation and ensure reliability is a growing challenge.

- Cybersecurity Risks in Connected Infrastructure: As telecom and datacom networks become more interconnected, the connectors themselves, or the interfaces they create, can become potential points of vulnerability for cyberattacks. Ensuring robust security at the physical layer is a critical challenge.

- Intense Competition and Intellectual Property Protection: The market is characterized by strong competition. Protecting intellectual property and differentiating products through innovation is crucial for sustained success.

- Global Geopolitical Factors and Trade Policies: Trade tensions, tariffs, and geopolitical shifts can impact supply chains, market access, and the overall business environment for connector manufacturers, posing a challenge to global market stability.

Telecom Connector and Datacom Connector Market: Report Scope

This report thoroughly analyzes the Telecom Connector and Datacom Connector Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

Telecom Connector and Datacom Connector Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Telecom Connector and Datacom Connector Market |

| Market Size in 2023 | USD 11.23 Billion |

| Market Forecast in 2032 | USD 18.97 Billion |

| Growth Rate | CAGR of 6% |

| Number of Pages | 140 |

| Key Companies Covered | Delphi, HARTING Technology Group, Belden Incorporated, Foxconn Technology, Yazaki, TE Connectivity, 3M, Molex Incorporated, Amphenol, Sumitomo Wiring Systems |

| Segments Covered | By Type, By Application, By End-User, By Configuration, By Material, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Telecom Connector and Datacom Connector Market: Segmentation Insights

The global telecom connector and datacom connector market is divided by type, application, end-user, configuration, material, and region.

Segmentation Insights by Type

Based on type, the global telecom connector and datacom connector market is divided into fiber optic connectors, coaxial connectors, rj45 connectors, micro connectors, and HDMI connectors.

Fiber Optic Connectors dominate the telecom connector and datacom connector market due to their critical role in supporting high-speed data transmission across telecom and datacom networks. These connectors enable low-loss and high-bandwidth communication, making them indispensable in modern broadband infrastructure, 5G deployments, and data center applications. The rising global demand for faster internet, streaming services, and cloud computing continues to drive the adoption of fiber optic connectors. Their use in FTTH (Fiber-to-the-Home) and enterprise networks has further strengthened their market share, especially with the growing preference for single-mode and multi-mode fiber systems.

Coaxial Connectors remain a vital segment, primarily used in legacy telecom infrastructure, cable television, and RF communication systems. They provide excellent shielding against electromagnetic interference, making them suitable for high-frequency signal transmissions. Though gradually being phased out in favor of fiber optics in some sectors, coaxial connectors are still widely used in last-mile connectivity, broadcasting, and some military applications where robustness and signal fidelity are essential.

RJ45 Connectors are extensively utilized in Ethernet networking, local area networks (LANs), and structured cabling systems. They offer simplicity, cost-effectiveness, and ease of installation, making them the standard choice in commercial buildings, educational institutions, and residential internet setups. With ongoing growth in IoT devices, smart homes, and office digitization, RJ45 connectors continue to maintain a strong foothold in short-to-medium range connectivity.

Micro Connectors cater to applications requiring compact and high-density connectivity solutions, such as mobile devices, telecommunications equipment, and aerospace systems. These connectors are designed for space-constrained environments without compromising signal integrity. Their rising demand is driven by the miniaturization trend across industries, particularly in wearable tech, small-form-factor networking devices, and edge computing units.

HDMI Connectors are predominantly used in audio-visual transmission but have also found application in datacom systems involving multimedia content sharing, video conferencing, and digital signage. While not traditionally associated with telecom infrastructure, their inclusion in communication endpoints and integration with smart systems (e.g., unified communications and AV-over-IP solutions) has expanded their relevance. The market for HDMI connectors continues to grow as video data becomes more integral to communication workflows.

Segmentation Insights by Application

On the basis of application, the global telecom connector and datacom connector market is bifurcated into telecommunications, data centers, networking, infrastructure, and consumer electronics.

Telecommunications is the dominant application segment and the telecom connector and datacom connector market growth. Telecom connectors are essential in establishing robust wired and wireless communications, particularly in base stations, telecom towers, central offices, and switching centers. The ongoing global deployment of 5G networks has intensified the need for fiber optic connectors that support ultra-high data transfer rates with minimal latency and signal loss. Furthermore, the shift from traditional circuit-switched systems to IP-based and cloud-native networks has increased demand for modular and scalable connector systems. With the rising penetration of mobile broadband and government investments in rural telecom connectivity, this segment is expected to continue its lead throughout the forecast period.

Data Centers are another key application area, experiencing explosive demand driven by the rise of cloud computing, video streaming, and real-time analytics. Hyperscale and edge data centers require ultra-dense, low-latency interconnections to handle terabytes of data flow between servers, storage devices, and networking switches. Fiber optic connectors dominate this space due to their high bandwidth and ability to support parallel optical transceivers and high-speed links such as 100G, 400G, and beyond. Additionally, increased adoption of software-defined networking (SDN) and AI-driven automation in data centers has necessitated enhanced thermal performance, energy efficiency, and signal integrity—further shaping connector requirements in this segment.

Networking applications encompass enterprise LANs, wireless access points, branch offices, educational campuses, and government networks. Connectors in this segment serve as the backbone of structured cabling systems and are vital for Ethernet-based connectivity (especially Cat6, Cat6a, and Cat7 via RJ45 connectors). The proliferation of IoT devices, IP surveillance systems, and smart office infrastructure is accelerating demand for both copper and optical connectors. Plug-and-play capabilities, durability, and backward compatibility are key purchase criteria in this space. The ongoing shift toward Wi-Fi 6 and multi-gigabit Ethernet also plays a significant role in shaping demand.

Infrastructure includes outdoor and mission-critical environments such as telecom shelters, railway signaling systems, smart city grids, power utility networks, and traffic control systems. These applications require robust, weatherproof, and vibration-resistant connectors capable of withstanding temperature fluctuations, moisture, UV radiation, and dust. Coaxial and hybrid connectors are often used for RF signal transmission in long-distance communication lines, while ruggedized fiber connectors support high-speed backbone networks in industrial and defense infrastructure. The rising trend of urban infrastructure digitization and public safety networks is expected to boost demand in this category.

Consumer Electronics represents a rapidly expanding segment due to widespread adoption of internet-connected devices. HDMI, RJ45, USB, and compact fiber connectors are widely used in devices such as smart TVs, streaming media players, gaming consoles, set-top boxes, routers, and smart home control hubs. The demand is driven by 4K/8K video streaming, interactive media content, and integration of voice-controlled assistants. With the growth of home networking and entertainment systems, connectors that support high data rates, low power consumption, and compact form factors are in strong demand. Furthermore, as consumers seek seamless connectivity across multiple devices, connector compatibility and user convenience are becoming increasingly important.

Segmentation Insights by End-User

On the basis of end-user, the global telecom connector and datacom connector market is bifurcated into enterprises, telecommunication service providers, government organizations, educational institutions, and healthcare facilities.

Enterprises dominate the end-user segment of the Telecom Connector and Datacom Connector Market, driven by their growing need for advanced, high-speed connectivity solutions across various operational levels. From small businesses to large multinational corporations, enterprises require robust communication infrastructure to support data centers, internal networks, unified communications, video conferencing, and cloud-based applications. The increasing adoption of hybrid work environments and digital transformation initiatives is accelerating the deployment of fiber optic and RJ45 connectors in LAN setups, server rooms, and structured cabling.

Telecommunication Service Providers are the dominant end-user segment, given their extensive role in deploying, maintaining, and upgrading network infrastructure. These service providers are heavily investing in 5G networks, fiber-to-the-home (FTTH) solutions, and edge computing architecture—all of which require a vast range of optical and coaxial connectors. Their need for high-density, low-loss, and field-deployable connectors is critical to supporting high bandwidth and low latency demands. As telecom operators shift to software-defined and virtualized network architectures, the importance of connectors that facilitate quick integration and minimize signal degradation becomes paramount.

Government Organizations utilize telecom and datacom connectors in a wide range of secure and mission-critical communication systems. These include defense communication networks, emergency response systems, surveillance infrastructure, and national data centers. The demand here is driven by requirements for high-security, interference-free transmission, and rugged hardware that can withstand harsh environments. Fiber optic connectors are particularly preferred for their resistance to electromagnetic interference and eavesdropping, making them ideal for classified and critical infrastructure deployments.

Educational Institutions rely on a strong IT and communications backbone for digital learning, campus management, and research activities. Schools, universities, and research centers deploy connectors across campus-wide networks, computer labs, smart classrooms, and server rooms. As institutions adopt e-learning platforms, cloud-based applications, and video conferencing tools, the need for reliable, high-speed connectors has grown. RJ45 connectors remain widespread, but fiber connectors are increasingly being introduced to support higher bandwidth for collaborative and virtual learning environments.

Healthcare Facilities such as hospitals, diagnostic centers, and telemedicine units are rapidly digitizing operations, which boosts the demand for dependable and hygienic connector systems. Applications range from EHR (electronic health records) and imaging systems to patient monitoring and real-time data transfer across medical departments. High-speed data transmission with zero tolerance for failure is critical in clinical settings, making fiber optic and shielded coaxial connectors vital for ensuring data accuracy and operational continuity. The increasing use of connected medical devices and remote care platforms further fuels demand in this sector.

Segmentation Insights by Configuration

On the basis of configuration, the global telecom connector and datacom connector market is bifurcated into modular connectors, fixed connectors, stackable connectors, and field-installable connectors.

Modular Connectors dominate the telecom connector and datacom connector market segment, owing to their widespread use in LANs and structured cabling. These connectors are primarily employed in structured cabling systems and LAN networks, especially in enterprise and residential settings. RJ45 connectors, a common type of modular connector, are used extensively in Ethernet-based networks. Their modularity allows for quick and tool-less replacement or upgrades, making them ideal for scalable infrastructure. As demand for modular data centers and flexible workspace cabling grows, modular connectors are gaining traction in both commercial and industrial environments.

Fixed Connectors are designed for permanent installations where stability, durability, and performance are paramount. These connectors are typically used in backbone cabling, telecommunications towers, and equipment that requires minimal human interference post-installation. Fixed connectors are known for superior signal integrity and resistance to environmental wear, making them suitable for long-term deployment in critical communication systems. Industries such as defense, telecom infrastructure, and broadcast rely on fixed connectors for maintaining uninterrupted service and reduced signal loss over long distances.

Stackable Connectors are engineered to support high-density configurations, particularly in environments where space-saving is crucial. They are used in server rooms, networking equipment, and high-performance computing systems to accommodate multiple connections in a compact footprint. Stackable connectors are key to optimizing rack space in data centers and communication hubs. Their modular stacking capability ensures quick scalability and supports evolving network demands without the need for complete system overhauls. As cloud service providers and colocation centers expand, the demand for stackable connector solutions is projected to increase steadily.

Field-Installable Connectors cater to real-time, on-site installations and are favored for their convenience and cost-effectiveness in environments requiring quick deployment and repair. These connectors are popular in fiber optic networks, where field splicing is required during installations or maintenance in outdoor and indoor setups. Technicians use field-installable connectors for drop cables in FTTH systems, enterprise networks, and campus connectivity. Their ability to be assembled without specialized tools and their compatibility with a wide range of cable types make them highly valuable in dynamic installation conditions.

Segmentation Insights by Material

On the basis of material, the global telecom connector and datacom connector market is bifurcated into plastic connectors, metal connectors, ceramic connectors, and hybrid connectors.

Plastic Connectors dominate in telecom connector and datacom connector market segments due to their affordability and design flexibility. These connectors are generally made from high-performance plastics such as polycarbonate or nylon, offering insulation properties and resistance to environmental stress. Plastic connectors are commonly found in internal device connections and cable assemblies that do not require shielding against high electromagnetic interference. Their affordability and ease of mass production make them dominant in high-volume, low-cost applications such as routers, modems, and home networking systems.

Metal Connectors offer superior durability, shielding, and conductivity, making them essential in high-performance and industrial-grade telecom and datacom systems. Materials such as aluminum, stainless steel, and brass are often used for their strength and resistance to corrosion. Metal connectors are favored in environments where signal integrity and protection from electromagnetic and radio frequency interference are critical, such as in telecommunications base stations, data centers, and critical infrastructure. Their robustness makes them suitable for harsh environments including outdoor installations, industrial machinery, and aerospace-grade networks.

Ceramic Connectors are niche yet crucial components in ultra-high-performance applications, especially in fiber optic systems. They are primarily used in the alignment ferrules of fiber optic connectors due to their exceptional thermal stability, hardness, and low thermal expansion, which ensures precise signal transmission. Ceramic materials like zirconia provide high durability and superior alignment accuracy, which is vital for maintaining signal fidelity in high-speed and long-distance communication networks. While costlier, ceramic connectors are indispensable in mission-critical applications such as high-speed internet backbones and precision instrumentation.

Hybrid Connectors combine materials (e.g., metal and plastic, or ceramic and plastic) to balance cost, performance, and durability. These connectors are tailored for specific applications requiring a mix of flexibility, conductivity, and insulation. Hybrid connectors are increasingly adopted in modern telecom equipment that demands high signal integrity while maintaining weight and cost constraints. They are particularly useful in modular systems, where parts of the connector might face different environmental or mechanical conditions, such as automotive telecom units and multi-port communication devices.

Telecom Connector and Datacom Connector Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Telecom Connector and Datacom Connector Market due to its highly developed telecommunications landscape, widespread adoption of fiber-optic networks, and the region’s leadership in cloud computing and data center growth. The United States, in particular, continues to be a global hub for hyperscale data centers operated by companies like Amazon, Microsoft, and Google, which creates significant demand for high-speed and high-density datacom connectors. The rollout of 5G infrastructure across major cities is accelerating the need for robust telecom connectors capable of handling increased data transmission volumes. Furthermore, increasing use of IoT, AI-powered networks, and edge computing technologies further supports the demand for reliable and miniaturized interconnect solutions. In Canada, federal investments in broadband expansion in underserved regions are also contributing to steady market growth.

Europe is a mature and technologically progressive market, with strong demand for telecom and datacom connectors driven by government initiatives promoting digitalization, smart manufacturing, and green ICT infrastructure. Countries like Germany, the UK, France, and the Netherlands are aggressively upgrading their telecom networks to support high-speed 5G connectivity and next-gen broadband services. The European Union's emphasis on data sovereignty and the General Data Protection Regulation (GDPR) is fueling local data center construction, which in turn requires sophisticated connector technologies for server racks, optical transceivers, and high-speed interconnects. Additionally, the rising number of edge data centers and the adoption of Industry 4.0 practices are expected to enhance demand across both telecom and datacom verticals in the region.

Asia-Pacific is the fastest-growing regional market, largely driven by surging data consumption, a booming electronics manufacturing base, and substantial investments in next-generation network infrastructure. China is both a major manufacturer and consumer of telecom/datacom connectors, with state-sponsored 5G deployment, rapid expansion of FTTH (Fiber-to-the-Home), and large-scale digital transformation initiatives. Japan and South Korea continue to lead in high-speed broadband access, encouraging the use of advanced connectors to support real-time data processing. India’s increasing smartphone penetration, digital inclusion campaigns (e.g., Digital India), and data center capacity additions across major cities are accelerating connector demand. The rapid rise of smart city initiatives, connected vehicles, and AI-powered network infrastructure also adds to the market’s momentum across Asia-Pacific.

Latin America is showing steady growth in the telecom connector and datacom connector space, mainly led by Brazil, Mexico, Colombia, and Chile. The expansion of 4G LTE networks and the beginning stages of 5G trials are creating new opportunities for high-frequency connectors and fiber-optic components. Brazil’s data center ecosystem is expanding in response to rising demand for cloud services, while Mexico is becoming a key location for network infrastructure expansion and smart manufacturing. Despite facing some infrastructural and regulatory hurdles, growing internet penetration, regional IT outsourcing, and the digital transformation of enterprises are enhancing demand for reliable and cost-effective connector solutions across telecom and data communication applications.

Middle East and Africa are emerging regions with untapped potential, especially in urbanizing countries that are investing in telecom infrastructure, smart cities, and digitization. In the Middle East, the UAE, Saudi Arabia, and Qatar are spearheading advanced network deployments, including nationwide 5G coverage, which drives demand for compact, rugged, and high-speed telecom connectors. Investment in smart infrastructure for events like Expo 2020 and Vision 2030 initiatives further supports the demand. In Africa, although rural connectivity remains a challenge, countries such as South Africa, Kenya, and Nigeria are developing mobile broadband infrastructure and upgrading datacenters to support local content hosting. Satellite and wireless broadband are being leveraged in remote regions, increasing the need for specialized interconnect technologies.

Telecom Connector and Datacom Connector Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the telecom connector and datacom connector market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global telecom connector and datacom connector market include:

- Delphi

- HARTING Technology Group

- Belden Incorporated

- Foxconn Technology

- Yazaki

- TE Connectivity

- 3M

- Molex Incorporated

- Amphenol

- Sumitomo Wiring Systems

The global telecom connector and datacom connector market is segmented as follows:

By Type

- Fiber Optic Connectors

- Coaxial Connectors

- RJ45 Connectors

- Micro Connectors

- HDMI Connectors

By Application

- Telecommunications

- Data Centers

- Networking

- Infrastructure

- Consumer Electronics

By End-User

- Enterprises

- Telecommunication Service Providers

- Government Organizations

- Educational Institutions

- Healthcare Facilities

By Configuration

- Modular Connectors

- Fixed Connectors

- Stackable Connectors

- Field-Installable Connectors

By Material

- Plastic Connectors

- Metal Connectors

- Ceramic Connectors

- Hybrid Connectors

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Telecom Connector and Datacom Connector

Request Sample

Telecom Connector and Datacom Connector