Trailer Assist System Market Size, Share, and Trends Analysis Report

CAGR :

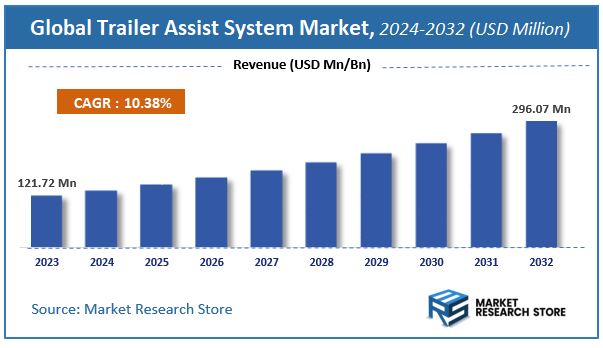

| Market Size 2023 (Base Year) | USD 121.72 Million |

| Market Size 2032 (Forecast Year) | USD 296.07 Million |

| CAGR | 10.38% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Trailer Assist System Market Insights

According to Market Research Store, the global trailer assist system market size was valued at around USD 121.72 million in 2023 and is estimated to reach USD 296.07 million by 2032, to register a CAGR of approximately 10.38% in terms of revenue during the forecast period 2024-2032.

The trailer assist system report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Trailer Assist System Market: Overview

A Trailer Assist System is an advanced driver-assistance system (ADAS) designed to significantly simplify the often-challenging task of reversing a vehicle with a hitched trailer. Unlike conventional reversing, where steering input is counter-intuitive for the trailer's movement, these systems allow the driver to "steer" the trailer directly using an intuitive interface, such as a control knob or a touchscreen. The system then automatically calculates and executes the necessary steering adjustments for the tow vehicle, guiding the trailer along the desired path while the driver controls acceleration and braking. Many systems also include features to prevent jack-knifing and provide visual guidance, greatly reducing stress and improving safety for drivers, especially those new to towing or maneuvering in tight spaces.

Key Highlights

- The trailer assist system market is anticipated to grow at a CAGR of 10.38% during the forecast period.

- The global trailer assist system market was estimated to be worth approximately USD 121.72 million in 2023 and is projected to reach a value of USD 296.07 million by 2032.

- The growth of the trailer assist system market is being driven by increasing demand for enhanced vehicle safety features and the rising popularity of recreational towing.

- Based on the type, the camera/sensor segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology type, the semi-autonomous (L3) segment is projected to swipe the largest market share.

- In terms of vehicle type, the passenger cars segment is expected to dominate the market.

- Based on the end user type, the OEM fitted segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Trailer Assist System Market: Dynamics

The Trailer Assist System market, an integral part of the automotive ADAS landscape, is shaped by a variety of dynamics. These forces collectively influence its growth trajectory, presenting both significant opportunities and notable hurdles for market players.

Key Growth Drivers

- Increasing Demand for Enhanced Vehicle Safety: A primary driver is the growing consumer and regulatory emphasis on vehicle safety. Trailer assist systems significantly mitigate the risk of accidents during challenging maneuvers like reversing, which are often prone to errors and can lead to costly damage or injuries. As road safety regulations become more stringent globally, automakers are compelled to integrate such advanced safety features, thereby boosting market demand.

- Rising Popularity of Recreational Vehicles (RVs) and Towing Activities: The burgeoning trend of outdoor recreational activities, including camping, boating, and off-roading, has led to a surge in the purchase of SUVs, pickup trucks, and RVs. This directly translates into a higher demand for intelligent towing solutions that simplify the process of hitching, maneuvering, and parking trailers, making towing more accessible and convenient for a wider consumer base.

- Advancements in Automotive Technology and Sensor Integration: Continuous innovation in sensor technologies (e.g., high-resolution cameras, ultrasonic, radar, LiDAR), along with sophisticated software algorithms and Artificial Intelligence (AI), has made trailer assist systems more precise, reliable, and user-friendly. These technological improvements enhance system performance, allowing for real-time adjustments and intuitive control, which in turn drives adoption.

- Expansion in Commercial and Logistics Fleets: Beyond recreational use, there's a growing adoption of trailer assist systems in commercial transportation and logistics. Fleet operators are increasingly seeking solutions to improve operational efficiency, reduce downtime from accidents, and enhance driver safety. Trailer assist systems offer significant value by streamlining maneuvers in loading docks and tight spaces, leading to increased productivity and cost savings for businesses.

Restraints

- High Development and Integration Costs: The sophisticated nature of trailer assist systems, requiring advanced sensors, complex AI algorithms, and precise calibration, translates into significant development and manufacturing expenses for automotive OEMs. These high costs can make the systems more expensive for the end consumer, potentially limiting widespread adoption, especially in price-sensitive markets.

- Lack of Awareness and Limited Penetration in Developing Regions: Despite the benefits, there's still a lack of consumer awareness about trailer assist systems, particularly in many developing and underdeveloped countries. This, coupled with lower towing penetration rates in these regions, limits the market's expansion as consumers may not perceive the immediate need or value of such advanced features.

- Technical Complexity and Reliability Concerns: Integrating trailer assist systems with diverse vehicle architectures and ensuring seamless operation across various trailer types can be technically challenging. Furthermore, concerns about system reliability, especially in adverse weather conditions or due to sensor malfunctions, can impact user trust and slow down market penetration.

Opportunities

- Emergence of AI-Based and Autonomous Towing Solutions: The ongoing development of AI-powered and fully autonomous towing features presents a significant opportunity. As autonomous driving technology matures, the integration of advanced AI could lead to trailer assist systems that offer even greater precision, predictive capabilities, and potentially hands-free towing in the future, creating new market segments and revenue streams.

- Growth in the Aftermarket Segment: While many systems are currently OEM-fitted, there is a growing opportunity in the aftermarket. As older vehicles without integrated systems remain on the road, demand for aftermarket trailer assist solutions could rise, allowing specialized providers to offer retrofit options and broaden the market reach.

- Increasing Demand for Electric and Hybrid Vehicles: The shift towards electric and hybrid vehicles offers a unique opportunity for trailer assist systems. As these vehicles often come with advanced electronics and sophisticated control systems, integrating trailer assist functionalities can be more seamless, potentially enhancing their appeal for towing purposes and catering to a growing segment of environmentally conscious consumers.

Challenges

- Regulatory Variations and Standardization Issues: The absence of universally standardized regulations for trailer assist systems across different countries creates compliance challenges for manufacturers. Varying safety standards and certification requirements can increase development costs and hinder global market penetration, requiring customized solutions for different regions.

- Cybersecurity Risks: As trailer assist systems become more integrated with vehicle networks and rely on connectivity, they become susceptible to cybersecurity threats. Ensuring robust protection against hacking and data breaches is a critical challenge, as any security vulnerability could compromise vehicle control, safety, and user data, leading to a loss of consumer confidence.

- Sensor Performance Limitations in Adverse Conditions: The effectiveness of trailer assist systems heavily relies on the performance of their sensors (cameras, radar, LiDAR). These sensors can be impacted by adverse weather conditions such as heavy rain, snow, fog, or direct sunlight, leading to reduced accuracy or temporary system disablement. Overcoming these environmental limitations remains a significant technical challenge for continuous and reliable operation.

Trailer Assist System Market: Report Scope

This report thoroughly analyzes the Trailer Assist System Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Trailer Assist System Market |

| Market Size in 2023 | USD 121.72 Million |

| Market Forecast in 2032 | USD 296.07 Million |

| Growth Rate | CAGR of 10.38% |

| Number of Pages | 167 |

| Key Companies Covered | Continental, Bosch, Magna, WABCO, Westfalia, Ford, Land Rover |

| Segments Covered | By Type, By Technology Type, By Vehicle Type, By End User Type, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Trailer Assist System Market: Segmentation Insights

The global trailer assist system market is divided by type, technology type, vehicle type, end user type, and region.

Segmentation Insights by Type

Based on type, the global trailer assist system market is divided into camera/sensor and software module.

The Camera/Sensor segment is the most dominant in the Trailer Assist System market. This segment encompasses the crucial hardware components, including high-resolution cameras, ultrasonic sensors, radar, and LiDAR, which are responsible for collecting real-time environmental data. These sensors provide vital information such as the angle of the trailer relative to the vehicle, obstacles in the blind spot, and the overall surroundings. The increasing demand for advanced driver assistance systems (ADAS) and enhanced vehicle safety directly drives the growth of this segment, as accurate and comprehensive data input from these sensors is fundamental for the trailer assist system's ability to calculate precise steering angles and prevent accidents. Automakers are heavily investing in these technologies, integrating AI-powered vision systems to improve accuracy and make trailer maneuvering easier.

The Software Module segment, while equally essential, typically holds a smaller market share compared to Camera/Sensor. This segment comprises the complex algorithms, artificial intelligence (AI), and control logic that process the data received from the cameras and sensors. The software module translates the driver's intended direction for the trailer into precise steering commands for the tow vehicle, preventing issues like jack-knifing and enabling smooth maneuvers. It is responsible for the intelligence and responsiveness of the system, allowing for features like trailer trajectory prediction and real-time visualization. While software development is critical for system functionality and continuous improvement through over-the-air updates, the tangible hardware components (cameras and sensors) often represent a larger portion of the initial cost and are foundational for the system's operation, leading to the Camera/Sensor segment's larger market share.

Segmentation Insights by Technology Type

On the basis of technology type, the global trailer assist system market is bifurcated into semi-autonomous (l3) and autonomous (l4, l5).

The Semi-Autonomous (L3) segment is currently the most dominant in the Trailer Assist System market. Level 3 automation, also known as "Conditional Driving Automation," means that the vehicle can handle specific driving tasks under certain conditions without constant driver supervision. In the context of trailer assist, this translates to systems that can automatically steer the vehicle to guide the trailer during reversing or maneuvering, while the driver is still required to monitor the environment and be ready to intervene if the system encounters a situation it cannot handle. Most commercially available trailer assist systems today fall into this category, offering significant convenience and safety enhancements without fully removing the human driver from the loop. Their widespread adoption is driven by the balance they strike between automation, cost, and current regulatory frameworks, making them a practical and accessible solution for a broad range of consumers and commercial users.

The Autonomous (L4, L5) segment represents a nascent but rapidly growing area within the Trailer Assist System market. Level 4 (High Driving Automation) allows the vehicle to perform all driving tasks and monitor the driving environment under specific conditions, without requiring human intervention. Level 5 (Full Driving Automation) refers to systems that can operate completely autonomously under all driving conditions. For trailer assist, this would imply systems that can automatically hitch, maneuver, and park a trailer without any driver input, or even with no driver present in the vehicle, within defined operational design domains (ODDs). While the technology for fully autonomous trailer maneuvering is in advanced stages of development and testing, its widespread commercialization is limited by technological complexities, high development costs, and the absence of clear regulatory frameworks. However, as autonomous driving technology matures, this segment holds immense potential for revolutionizing logistics, transportation, and specialized industries by offering unparalleled efficiency and safety.

Segmentation Insights by Vehicle Type

Based on vehicle type, the global trailer assist system market is divided into passenger cars, lcv, and trucks.

Passenger Cars currently represent the most dominant segment in the Trailer Assist System market. This dominance is driven by the surging global sales of SUVs and pickup trucks, which are increasingly being used for recreational towing activities such as camping, boating, and hauling personal equipment. Consumers of these vehicles often prioritize safety and convenience, making integrated trailer assist features a highly desirable option. Automakers are actively incorporating these systems into their passenger vehicle lineups, often as part of advanced driver-assistance system (ADAS) packages, to enhance user experience and simplify challenging maneuvers like hitching, reversing, and parking trailers. The increasing awareness and affordability of these systems are further solidifying the passenger car segment's leading position.

Light Commercial Vehicles (LCVs) constitute a significant and growing segment in the Trailer Assist System market. LCVs, including vans and smaller pickup trucks, are extensively used for various commercial purposes, such as last-mile delivery, trade services, and small business operations, where towing smaller trailers for tools or goods is common. While these vehicles might not tow as frequently or as heavily as large trucks, the demand for efficiency and safety in urban and suburban environments drives the adoption of trailer assist systems. These systems help LCV drivers navigate tight spaces, improve maneuverability in crowded areas, and reduce the risk of costly accidents, leading to increased productivity and reduced operational costs for businesses.

Trucks, particularly heavy-duty commercial trucks, form the third major segment in the Trailer Assist System market. Although the per-unit adoption might be lower than in passenger cars or LCVs, the complexity and potential for severe accidents in heavy-duty towing make trailer assist systems extremely valuable for this segment. These systems are crucial for improving safety, reducing driver fatigue, and enhancing operational efficiency in large-scale logistics and transportation. While the functionalities might differ slightly, often focusing on blind-spot detection, brake control, and preventing jack-knifing rather than automated steering during reversing (which is more common in passenger vehicles), the demand for these specialized towing aids is steadily increasing within the commercial trucking sector, driven by stringent safety regulations and the need for optimized fleet management.

Segmentation Insights by End User Type

On the basis of end user type, the global trailer assist system market is bifurcated into OEM fitted and aftermarket.

OEM Fitted (Original Equipment Manufacturer Fitted) is the most dominant segment in the Trailer Assist System market. This segment comprises trailer assist systems that are pre-installed in new vehicles directly by the automotive manufacturer during the production process. The dominance of OEM-fitted systems is driven by several factors: they offer seamless integration with the vehicle's existing electronic architecture and dashboard controls, ensuring optimal performance, reliability, and user experience. Consumers often prefer factory-installed features due to perceived higher quality, warranty coverage, and the convenience of having the system ready from the moment of purchase. Automakers actively promote these systems as premium features in their SUVs, pickup trucks, and some commercial vehicles, leveraging their extensive sales and marketing networks to make OEM-fitted solutions the primary choice for most new vehicle buyers.

The Aftermarket segment for Trailer Assist Systems is a smaller but growing portion of the market. This segment includes systems that are purchased and installed by consumers or third-party installers after the vehicle has been sold by the manufacturer. Aftermarket solutions cater primarily to owners of older vehicles that lack integrated trailer assist features, or to those who opted not to purchase the OEM version at the time of vehicle acquisition. These systems often provide similar functionalities through standalone kits that may involve external cameras, sensors, and dedicated control units. While aftermarket solutions offer flexibility and cost-effectiveness, their market share is limited by factors such as potential compatibility issues with various vehicle models, the need for professional installation, and a perceived difference in integration compared to factory-fitted systems. However, as the installed base of older vehicles remains substantial, and as technological advancements make aftermarket kits more user-friendly, this segment continues to offer growth opportunities.

Trailer Assist System Market: Regional Insights

- North America is expected to dominates the global market

North America stands as the undisputed leader in the global Trailer Assist System market. This dominance is primarily attributed to the region's robust automotive industry, particularly the high sales volume of pickup trucks and SUVs, which are frequently used for recreational and commercial towing. The strong culture of outdoor activities and RVing in countries like the United States and Canada directly translates to a high demand for advanced towing aids. Furthermore, early adoption of cutting-edge automotive technologies and a well-established infrastructure for ADAS development and integration contribute significantly to North America's leading position. Major automotive manufacturers in the region are actively incorporating trailer assist systems into their new vehicle models, further solidifying its market share.

Europe holds a substantial share in the Trailer Assist System market, positioned as the second-largest region. The market growth in Europe is driven by stringent safety regulations, a strong focus on vehicle safety, and the increasing adoption of ADAS features in passenger vehicles. While the towing culture might differ slightly from North America, there is a significant demand for trailer assist systems in commercial vehicles, agricultural machinery, and for leisure activities involving caravans and boat trailers. European automakers are at the forefront of automotive innovation, consistently introducing advanced technologies, including sophisticated towing aids, into their vehicle lineups. The emphasis on smart mobility solutions and autonomous driving technologies also indirectly contributes to the development and integration of trailer assist systems across the continent.

The Asia Pacific (APAC) region is emerging as the fastest-growing market for Trailer Assist Systems. This rapid growth is fueled by the booming automotive industry in countries like China, India, Japan, and South Korea, coupled with rising disposable incomes and changing consumer lifestyles that include more leisure and outdoor activities. Governments in this region are increasingly investing in smart city initiatives and advanced transportation systems, which creates a conducive environment for the adoption of ADAS technologies. While the initial adoption rate might be lower than in North America or Europe, the sheer volume of vehicle sales and the increasing awareness of safety features are expected to propel the APAC market significantly in the coming years. Local and international automotive players are actively developing and integrating these systems to cater to the region's evolving demands.

Latin America represents a nascent but growing market for Trailer Assist Systems. The market expansion in this region is primarily driven by increasing vehicle production and sales, particularly in countries like Brazil and Mexico. As economic conditions improve and the automotive industry expands, there is a gradual increase in the demand for advanced vehicle features, including towing assistance systems. However, the market growth is comparatively slower due to factors such as lower average disposable incomes, less stringent safety regulations compared to developed regions, and a lower penetration rate of advanced ADAS technologies in general. Nevertheless, as the automotive sector matures and consumer awareness of safety features increases, Latin America is expected to witness steady growth in the adoption of trailer assist systems.

The Middle East and Africa (MEA) region currently holds the smallest share in the global Trailer Assist System market. The growth in this region is primarily concentrated in the Middle East, driven by significant investments in infrastructure development, increasing sales of luxury vehicles and SUVs, and a growing emphasis on road safety. Countries in the Gulf Cooperation Council (GCC) are leading this growth due to higher purchasing power and the presence of advanced automotive technologies. In contrast, the African continent faces challenges such as underdeveloped automotive infrastructure, lower disposable incomes, and limited awareness regarding advanced driver-assistance systems. While there are emerging opportunities in key African economies, the overall adoption rate for trailer assist systems remains relatively low compared to other regions, resulting in its smaller market share.

Trailer Assist System Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the trailer assist system market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global trailer assist system market include:

- Continental

- Bosch

- Magna

- WABCO

- Westfalia

- Ford

- Land Rover

The global trailer assist system market is segmented as follows:

By Type

- Camera/Sensor

- Software Module

By Technology Type

- Semi-Autonomous (L3)

- Autonomous (L4, L5)

By Vehicle Type

- Passenger Cars

- LCV

- Trucks

By End User Type

- OEM Fitted

- Aftermarket

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Trailer Assist System

Request Sample

Trailer Assist System