Transformer Manufacturing Market Size, Share, and Trends Analysis Report

CAGR :

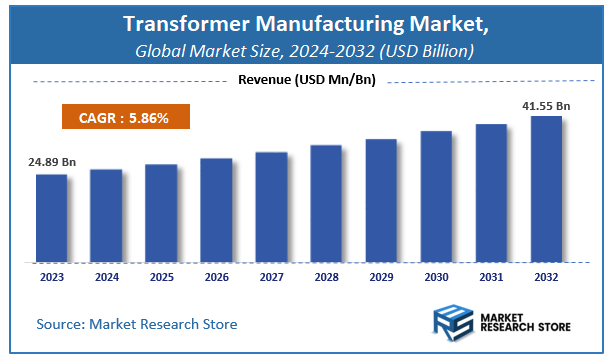

| Market Size 2023 (Base Year) | USD 24.89 Billion |

| Market Size 2032 (Forecast Year) | USD 41.55 Billion |

| CAGR | 5.86% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Transformer Manufacturing Market Insights

According to Market Research Store, the global transformer manufacturing market size was valued at around USD 24.89 billion in 2023 and is estimated to reach USD 41.55 billion by 2032, to register a CAGR of approximately 5.86% in terms of revenue during the forecast period 2024-2032.

The transformer manufacturing report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Transformer Manufacturing Market: Overview

Transformer manufacturing refers to the industrial process of designing, producing, and assembling electrical transformers, which are essential components used to transfer electrical energy between circuits through electromagnetic induction. These devices are critical for voltage regulation in power transmission and distribution networks, ensuring the efficient delivery of electricity from power generation plants to end users. The manufacturing process involves several stages including core assembly, coil winding, insulation, tank fabrication, oil filling (for oil-cooled types), and rigorous testing to meet safety and performance standards. Transformers are classified based on voltage level, insulation medium, installation environment (indoor or outdoor), and application such as power, distribution, instrument, or isolation transformers.

Key Highlights

- The transformer manufacturing market is anticipated to grow at a CAGR of 5.86% during the forecast period.

- The global transformer manufacturing market was estimated to be worth approximately USD 24.89 billion in 2023 and is projected to reach a value of USD 41.55 billion by 2032.

- The growth of the transformer manufacturing market is being driven by increasing demand for electricity, expansion of power infrastructure in developing economies, and the modernization of aging grid systems in developed regions.

- Based on the product type, the power transformers segment is growing at a high rate and is projected to dominate the market.

- On the basis of insulation type, the liquid-immersed segment is projected to swipe the largest market share.

- In terms of phase, the three-phase segment is expected to dominate the market.

- Based on the application, the utilities segment is expected to dominate the market.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Transformer Manufacturing Market: Dynamics

Key Growth Drivers:

- Growing Demand for Electricity Infrastructure: Expanding urbanization, industrialization, and the need to modernize existing power grids globally are driving significant demand for transformers for power transmission and distribution.

- Increasing Investments in Renewable Energy: The surge in renewable energy generation (solar, wind) requires transformers to step up or step-down voltage for grid integration and transmission, boosting market growth.

- Electrification of Transportation and Industries: The shift towards electric vehicles, electric machinery, and electrified industrial processes necessitates a robust electricity infrastructure, consequently increasing the demand for transformers.

- Modernization and Upgradation of Existing Grids: Aging power infrastructure in many developed nations requires replacement and upgrades with more efficient and reliable transformers, creating a substantial replacement market.

- Government Initiatives and Regulations: Government policies promoting grid modernization, rural electrification, and the adoption of renewable energy often include investments in transformer infrastructure.

Restraints:

- High Raw Material Costs: The price volatility of key raw materials like copper, aluminum, and steel significantly impacts the manufacturing cost of transformers, potentially affecting profitability and project timelines.

- Long Manufacturing Lead Times: The production of large power transformers can involve complex manufacturing processes and long lead times, which can create bottlenecks in project development.

- Environmental Concerns and Regulations: Regulations regarding energy efficiency standards, the use of insulating fluids (like mineral oil), and the disposal of old transformers can increase manufacturing costs and complexity.

- Skilled Labor Shortages: The manufacturing and maintenance of transformers require specialized skills, and a shortage of qualified engineers and technicians can hinder production and service capabilities.

- Geopolitical Instability and Trade Barriers: Global geopolitical tensions and trade restrictions can disrupt supply chains for raw materials and components, impacting transformer manufacturing and international trade.

Opportunities:

- Development of Smart and Digital Transformers: The integration of sensors, communication capabilities, and digital technologies into transformers enables remote monitoring, diagnostics, and predictive maintenance, creating new market segments.

- Growing Demand for Energy-Efficient Transformers: Increasing focus on energy conservation and stricter efficiency regulations drive the demand for advanced, energy-efficient transformers that reduce transmission losses.

- Expansion of Microgrids and Distributed Generation: The rise of microgrids and distributed power generation systems (including renewable sources) creates opportunities for smaller, specialized transformers.

- Demand for Compact and Substation Transformers: Urbanization and space constraints in cities are driving the need for compact and aesthetically integrated substation transformers.

- Aftermarket Services and Refurbishment: The market for transformer maintenance, repair, and refurbishment is growing as the installed base of transformers ages, offering opportunities for service providers and manufacturers.

Challenges:

- Ensuring Reliability and Durability: Transformers are critical infrastructure components, and ensuring their long-term reliability and durability under various operating conditions is a paramount challenge.

- Managing Short-Circuit Faults and Overloads: Designing transformers that can withstand and safely interrupt short-circuit faults and overloads is crucial for grid stability and safety.

- Harmonization of Standards and Specifications: Varying technical standards and specifications across different regions can create challenges for manufacturers operating globally.

- Adapting to Grid Modernization and Smart Grid Requirements: Transformer manufacturers need to innovate and adapt their products to meet the evolving requirements of smart grids, including bidirectional power flow and integration with digital control systems.

- Competition from Global Players: The transformer manufacturing market is globally competitive, requiring manufacturers to focus on innovation, cost efficiency, and quality to maintain market share.

Transformer Manufacturing Market: Report Scope

This report thoroughly analyzes the transformer manufacturing market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Transformer Manufacturing Market |

| Market Size in 2023 | USD 24.89 Billion |

| Market Forecast in 2032 | USD 41.55 Billion |

| Growth Rate | CAGR of 5.86% |

| Number of Pages | 150 |

| Key Companies Covered | ABB Ltd., Siemens AG, General Electric Company, Schneider Electric SE, Mitsubishi Electric Corporation, Toshiba Corporation, Eaton Corporation plc, Hitachi Ltd., Crompton Greaves Limited, Hyundai Heavy Industries Co. Ltd., SPX Transformer Solutions Inc., |

| Segments Covered | By Product Type, By Insulation Type, By Phase, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Transformer Manufacturing Market: Segmentation Insights

The global transformer manufacturing market is divided by product type, insulation type, phase, application, and region.

Segmentation Insights by Product Type

Based on product type, the global transformer manufacturing market is divided into power transformers, distribution transformers, instrument transformers, and others.

In the transformer manufacturing market, Power Transformers represent the most dominant product segment. These transformers are primarily used in transmission networks for stepping up or stepping down voltage levels, typically handling voltages above 33 kV. Their large capacity and role in high-voltage applications make them essential for grid stability and long-distance power transmission, particularly in regions undergoing major infrastructure development and grid modernization. The increasing demand for energy and the expansion of power generation facilities—especially renewable energy—further boost the adoption of power transformers globally.

Following power transformers, Distribution Transformers constitute the second most dominant segment. These transformers operate at lower voltage levels and are crucial in delivering electricity from substations to end-users, such as homes and businesses. Their prevalence in urban and rural distribution networks, combined with growing urbanization and the need for efficient local power distribution, contributes to their significant market share. Moreover, smart grid development and rural electrification initiatives in developing countries further fuel demand for distribution transformers.

Instrument Transformers come next and serve a specialized role in power systems. They are used to isolate, transform, and measure electrical parameters like current and voltage for protection and metering purposes. While their market size is smaller compared to power and distribution transformers, they are vital in ensuring safe and accurate monitoring in high-voltage environments, making them indispensable in substations and power plants.

Segmentation Insights by Insulation Type

On the basis of insulation type, the global transformer manufacturing market is bifurcated into dry type and liquid-immersed.

In the transformer manufacturing market, Liquid-Immersed Transformers hold the dominant position by insulation type. These transformers use oil or other liquid as a cooling and insulating medium, offering higher efficiency and better overload capacity. They are widely used in utility-scale applications, industrial settings, and high-voltage transmission networks due to their superior cooling capabilities and longer service life. Their ability to handle higher voltage levels and heavy-duty operations makes them the preferred choice for large-scale power distribution and transmission infrastructure. Moreover, advancements in biodegradable and fire-safe insulating fluids have helped maintain their market leadership even as environmental concerns grow.

Dry Type Transformers, on the other hand, are the secondary but growing segment in the market. These transformers rely on air instead of liquid for cooling and are typically used in indoor or environmentally sensitive applications such as commercial buildings, hospitals, data centers, and transportation systems. They are safer in terms of fire risk, require less maintenance, and pose no threat of oil leakage, making them ideal for use in densely populated or confined spaces. Although dry type transformers cannot match the power handling capabilities of liquid-immersed models, their increasing use in urban infrastructure and renewable energy projects is gradually expanding their market share.

Segmentation Insights by Phase

Based on phase, the global transformer manufacturing market is divided into single phase and three phase.

In the transformer manufacturing market, Three-Phase Transformers are the most dominant segment by phase type. These transformers are widely used in industrial applications, utility grids, and large commercial facilities due to their ability to handle high power loads efficiently. Three-phase transformers support balanced load distribution, reduced copper usage, and better performance over long-distance power transmission, making them the standard in modern power systems. Their integral role in high-voltage transmission and large-scale industrial processes continues to drive their dominance across developed and developing regions alike.

Single-Phase Transformers, while less dominant, serve a crucial role in residential and light commercial applications. These transformers are simpler in design and are typically used to supply power to individual homes, small businesses, and rural areas where power demand is lower. They are also commonly found in low-voltage appliances and equipment. Although they handle lower loads compared to their three-phase counterparts, the growing need for rural electrification and reliable backup systems keeps this segment relevant, especially in emerging markets and off-grid solutions.

Segmentation Insights by Application

On the basis of application, the global transformer manufacturing market is bifurcated into utilities, industrial, commercial, residential, and others.

In the transformer manufacturing market, the Utilities segment is the most dominant by application. Utility companies require large-scale transformers—especially power and distribution types—for electricity transmission and distribution across vast networks. The ongoing modernization of power grids, the integration of renewable energy sources, and the expansion of transmission infrastructure all contribute significantly to the demand in this segment. Utilities play a central role in national and regional energy systems, making them the largest and most consistent consumers of transformers globally.

The Industrial segment follows closely behind. Transformers used in industrial settings must support high-load machinery, production lines, and heavy-duty operations in sectors such as manufacturing, mining, oil & gas, and chemical processing. Industrial applications often require custom solutions, including both three-phase and specialty transformers, to manage complex electrical needs. As industrialization progresses in developing countries and automation expands in developed regions, the demand for industrial transformers continues to grow steadily.

Next is the Commercial segment, which includes applications in office buildings, shopping centers, educational institutions, and healthcare facilities. These settings require reliable and safe power distribution, typically supported by dry type transformers due to their safety and lower maintenance needs. Urban expansion and the rising number of commercial establishments contribute to the steady demand in this segment.

The Residential segment has a comparatively smaller share but remains significant, particularly in densely populated areas and regions undergoing electrification. Single-phase distribution transformers are commonly used to deliver power to individual homes and small apartment complexes. Growth in housing developments and rural electrification initiatives in emerging economies drive this segment.

Transformer Manufacturing Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

Asia-Pacific is the most dominant region in the global transformer manufacturing market. This leadership is fueled by rapid industrialization, widespread urban development, and a rising demand for electricity across major economies like China, India, and Japan. China, in particular, contributes significantly due to its massive infrastructure expansion and extensive power grid modernization initiatives. The region's strong manufacturing capabilities, along with government-backed energy projects and a growing focus on renewable integration, continue to drive robust demand for transformers across utility and industrial sectors.

North America ranks as the second most influential region in the transformer manufacturing market. The United States and Canada are at the forefront of replacing aging grid infrastructure and promoting clean energy sources. With an emphasis on energy efficiency and advanced transmission systems, the region is seeing a steady demand for high-performance transformers. Grid resilience projects, coupled with the increasing adoption of electric vehicles and renewable energy integration, further support market growth in this region.

Europe holds a prominent position in the market, primarily driven by its focus on sustainability and stringent environmental standards. Countries such as Germany, France, and the United Kingdom are investing heavily in smart grid development and energy-efficient transformer technologies. The region's push toward reducing greenhouse gas emissions and enhancing renewable capacity, especially from wind and solar sources, plays a crucial role in its steady demand for both power and distribution transformers.

Middle East and Africa is an emerging region in the transformer manufacturing market, showing steady growth as nations work to diversify their energy sources and expand grid capacity. Countries like Saudi Arabia and the United Arab Emirates are investing in large-scale power infrastructure, including smart grids and renewable energy facilities. This is driving the demand for transformers that can support both traditional and modernized power systems, with increasing emphasis on grid reliability and energy access.

Latin America represents a developing but active region in the transformer market. Countries such as Brazil and Mexico are enhancing their electricity infrastructure through public and private investments in energy projects. The growing demand for electricity in both urban and rural areas, along with efforts to integrate renewable sources and modernize existing power networks, is creating opportunities for transformer manufacturers to cater to diverse and expanding needs across the region.

Transformer Manufacturing Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the transformer manufacturing market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global transformer manufacturing market include:

- ABB Ltd.

- Siemens AG

- General Electric Company

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Eaton Corporation plc

- Hitachi Ltd.

- Crompton Greaves Limited

- Hyundai Heavy Industries Co. Ltd.

- SPX Transformer Solutions Inc.

- SGB-SMIT Group

- Hyosung Heavy Industries

- Bharat Heavy Electricals Limited (BHEL)

- Fuji Electric Co. Ltd.

- Zhejiang TBEA Transformer Co. Ltd.

- Alstom SA

- Wilson Transformer Company

- Virginia Transformer Corp.

- Kirloskar Electric Company Ltd.

The global transformer manufacturing market is segmented as follows:

By Product Type

- Power Transformers

- Distribution Transformers

- Instrument Transformers

- Others

By Insulation Type

- Dry Type

- Liquid-Immersed

By Phase

- Single Phase

- Three Phase

By Application

- Utilities

- Industrial

- Commercial

- Residential

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Transformer Manufacturing

Request Sample

Transformer Manufacturing