Transportation Wireless Module Market Size, Share, and Trends Analysis Report

CAGR :

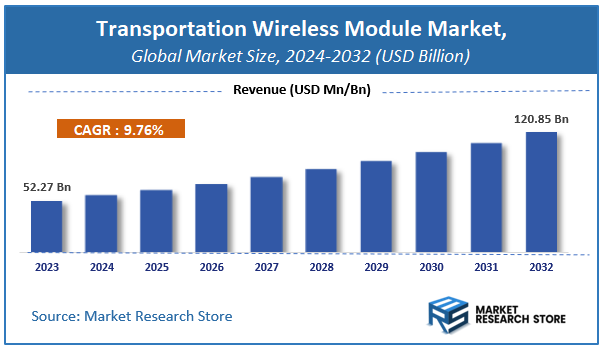

| Market Size 2023 (Base Year) | USD 52.27 Billion |

| Market Size 2032 (Forecast Year) | USD 120.85 Billion |

| CAGR | 9.76% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Transportation Wireless Module Market Insights

According to Market Research Store, the global transportation wireless module market size was valued at around USD 52.27 billion in 2023 and is estimated to reach USD 120.85 billion by 2032, to register a CAGR of approximately 9.76% in terms of revenue during the forecast period 2024-2032.

The transportation wireless module report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Transportation Wireless Module Market: Overview

A transportation wireless module is a compact, integrated component that enables wireless communication within transportation systems, such as vehicles, railways, logistics fleets, and public transit networks. These modules typically support wireless technologies like Wi-Fi, Bluetooth, cellular (3G/4G/5G), GPS, and LoRa, allowing real-time data transmission for applications such as vehicle tracking, remote diagnostics, fleet management, electronic toll collection, and connected infrastructure. Transportation wireless modules are vital to the development of intelligent transportation systems (ITS), autonomous vehicles, and smart logistics, as they ensure seamless data flow between vehicles and central management platforms or cloud-based systems.

Key Highlights

- The transportation wireless module market is anticipated to grow at a CAGR of 9.76% during the forecast period.

- The global transportation wireless module market was estimated to be worth approximately USD 52.27 billion in 2023 and is projected to reach a value of USD 120.85 billion by 2032.

- The growth of the transportation wireless module market is being driven by the rising demand for connected vehicles, advancements in vehicle-to-everything (V2X) technologies, and the integration of IoT in transportation.

- Based on the component, the hardware segment is growing at a high rate and is projected to dominate the market.

- On the basis of technology, the cellular technology segment is projected to swipe the largest market share.

- In terms of vehicle type, the passenger cars segment is expected to dominate the market.

- Based on the application, the fleet management segment is expected to dominate the market.

- In terms of end-user, the automotive sector segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Transportation Wireless Module Market: Dynamics

Key Growth Drivers:

- Rising Demand for Connected Vehicles: The growing adoption of connected vehicles that rely on wireless modules for navigation, infotainment, diagnostics, and safety features is driving market growth.

- Expansion of Smart Transportation Infrastructure: Government investments in smart city initiatives and intelligent transport systems (ITS) are encouraging the deployment of wireless communication modules for real-time monitoring and data exchange.

- Rapid Growth of Electric Vehicles (EVs): EVs increasingly depend on wireless modules for battery management, vehicle-to-grid (V2G) communication, and remote diagnostics, fueling demand in this segment.

- Increasing Adoption of Telematics and Fleet Management Solutions: Logistics and transportation companies are leveraging wireless modules for real-time vehicle tracking, route optimization, and predictive maintenance.

- Advancements in Wireless Communication Technologies: The development of 5G, NB-IoT, and LTE-M technologies enables faster and more reliable communication, improving the functionality of wireless modules in transportation.

Restraints:

- High Integration and Deployment Costs: The cost associated with integrating wireless modules into existing transportation systems and vehicles can be significant, especially for small operators.

- Data Privacy and Security Concerns: As transportation systems become more connected, vulnerabilities in wireless modules can expose critical data to cyber threats.

- Limited Network Infrastructure in Developing Regions: Inadequate network coverage and lower penetration of high-speed internet in some areas restrict the deployment of advanced wireless modules.

Opportunities:

- Emergence of Autonomous Vehicles: The development of autonomous driving technology relies heavily on wireless modules for sensor communication, real-time updates, and decision-making support.

- Growth in Public Transportation Automation: Wireless modules are being increasingly used in smart ticketing, passenger information systems, and automated fare collection, presenting new growth avenues.

- Rising Demand for Vehicle-to-Everything (V2X) Communication: Expansion of V2X technologies open up opportunities for modules that support communication between vehicles, infrastructure, pedestrians, and networks.

- Expansion into Emerging Markets: Rapid urbanization and infrastructure development in emerging economies provide a fertile ground for wireless module integration in transportation.

Challenges:

- Complexity of System Integration: Integrating wireless modules with multiple transportation subsystems (vehicles, infrastructure, cloud) can be technically challenging and require standardization.

- Regulatory and Compliance Hurdles: Varying regulations across regions regarding wireless communication standards and vehicle data management can slow down market expansion.

- Component Shortages and Supply Chain Disruptions: Global shortages in semiconductors and electronic components can impact production and availability of wireless modules.

- Interoperability Issues Across Platforms: Ensuring compatibility between wireless modules and different brands or models of transportation equipment remains a persistent challenge.

Transportation Wireless Module Market: Report Scope

This report thoroughly analyzes the Transportation Wireless Module Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Transportation Wireless Module Market |

| Market Size in 2023 | USD 52.27 Billion |

| Market Forecast in 2032 | USD 120.85 Billion |

| Growth Rate | CAGR of 9.76% |

| Number of Pages | 181 |

| Key Companies Covered | Sierra Wireless, Gemalto (Thales Group), Quectel, Telit, Huawei, Sunsea Group, LG Innotek, U-blox, Fibocom wireless Inc., Neoway |

| Segments Covered | By Component, By Technology, By Vehicle Type, By Application, By End-user, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Transportation Wireless Module Market: Segmentation Insights

The global transportation wireless module market is divided by component, technology, vehicle type, application, end-user, and region.

Segmentation Insights by Component

Based on component, the global transportation wireless module market is divided into hardware, software, services, cloud-based solutions, and network infrastructure.

In the transportation wireless module market, the hardware segment emerges as the most dominant among the components. This dominance is primarily due to the critical role physical devices play in enabling wireless communication across transportation systems, such as GPS modules, vehicle telematics units, wireless routers, and sensors. These modules are foundational for real-time tracking, fleet management, and intelligent transportation systems (ITS). The growing demand for smart and connected vehicles, along with the increasing integration of IoT in transportation, continues to fuel the adoption of advanced hardware components.

Following hardware, the software segment holds a significant share of the market. Software solutions are essential for managing data collected by hardware devices, enabling data analytics, security protocols, and efficient device management. Software also plays a key role in ensuring interoperability among diverse wireless systems and maintaining the performance of connected modules. As transportation systems become increasingly digitalized, software solutions that support automation, predictive maintenance, and communication management gain prominence.

Next in line is the services segment, which includes consulting, integration, maintenance, and support services. These services are vital for deploying, customizing, and optimizing wireless modules in various transportation applications. As transportation companies seek to improve operational efficiency and reduce downtime, the need for managed and professional services has grown steadily. The complexity of integrating wireless technology into existing infrastructures further contributes to the importance of this segment.

The cloud-based solutions segment follows, offering scalability, centralized data access, and enhanced data storage capabilities. Cloud platforms are particularly beneficial in large-scale transportation systems where centralized control and remote monitoring are essential. They support features like real-time traffic data sharing, vehicle diagnostics, and fleet telematics. However, despite their growing adoption, cloud solutions face challenges related to data security, connectivity in remote areas, and latency, which limits their dominance compared to hardware and software.

At the lower end of the spectrum is the network infrastructure segment, which includes communication backbones like cellular networks, satellite systems, and Wi-Fi infrastructure. Although this segment is critical to ensure seamless wireless communication, it is typically managed by telecom providers or governments and is considered more of an enabling layer rather than a standalone commercial segment for many transportation businesses. Consequently, while indispensable, it holds a smaller share in terms of direct market value in the transportation wireless module ecosystem.

Segmentation Insights by Technology

On the basis of technology, the global transportation wireless module market is bifurcated into cellular technology, satellite communication, wi-fi, bluetooth, and LoRaWAN.

In the transportation wireless module market, cellular technology stands out as the most dominant segment by technology. Its dominance is driven by its widespread availability, high data transmission speeds, and support for mobility across wide geographic areas—making it ideal for applications like fleet management, vehicle tracking, and real-time data communication. With advancements like 4G LTE and the emergence of 5G, cellular modules have become even more critical in enabling intelligent transportation systems, autonomous driving, and smart logistics.

Next is satellite communication, which plays a vital role in remote and underserved areas where terrestrial networks like cellular or Wi-Fi are unavailable. This technology is heavily utilized in maritime, aviation, and long-haul trucking sectors. Satellite communication provides reliable connectivity for navigation, tracking, and emergency services across vast distances. While it does not match cellular in terms of data speed or latency, its ability to maintain connections in remote locations ensures strong demand in specific transportation verticals.

Wi-Fi ranks third, serving as a convenient and cost-effective solution for short-range, high-speed communication, particularly in transportation hubs such as airports, railways, and bus terminals. It's also used in passenger information systems, onboard entertainment, and maintenance diagnostics when vehicles are stationary. However, Wi-Fi’s limited range and dependency on fixed infrastructure reduce its viability for long-haul or constantly mobile transportation use cases.

Following Wi-Fi is Bluetooth, known for its low power consumption and effectiveness in short-range communication. In transportation, Bluetooth is commonly used for in-vehicle connectivity between smartphones and infotainment systems, hands-free calling, and driver health monitoring devices. Despite its widespread presence in consumer applications, its limited range and bandwidth prevent it from being a primary technology in large-scale transportation systems.

Lastly, LoRaWAN (Long Range Wide Area Network) holds the smallest share in this market segment. While LoRaWAN is known for its long-range, low-power capabilities and cost efficiency, it is best suited for low-bandwidth applications such as simple vehicle status updates or environmental sensing. Its adoption in transportation remains limited compared to other technologies, although its potential is growing in niche applications within urban fleet and asset tracking where frequent but small data packets are needed.

Segmentation Insights by Vehicle Type

Based on vehicle type, the global transportation wireless module market is divided into passenger cars, commercial vehicles, trucks, buses, and motorcycles.

In the transportation wireless module market, passenger cars represent the most dominant vehicle type segment. The surge in connected car technologies, infotainment systems, telematics, and navigation services has significantly boosted the integration of wireless modules in this segment. Consumers increasingly demand features like real-time traffic updates, remote diagnostics, vehicle tracking, and smartphone integration, all of which require robust wireless connectivity. Automakers are also investing heavily in vehicle-to-everything (V2X) communications and autonomous driving capabilities, further strengthening the demand for wireless modules in passenger vehicles.

Commercial vehicles follow closely, encompassing light and heavy-duty transport vehicles used for logistics, delivery, and service operations. These vehicles heavily rely on wireless modules for fleet management, route optimization, real-time tracking, fuel monitoring, and driver behavior analytics. The growing e-commerce sector and increasing emphasis on supply chain transparency are key drivers for wireless technology adoption in this category.

Next in line are trucks, particularly long-haul and freight carriers, which depend on wireless modules for advanced telematics, driver communication, load monitoring, and remote diagnostics. Trucks often operate across large geographic regions, making technologies like GPS, satellite communication, and 4G/5G modules indispensable for efficient and safe operations. While part of the broader commercial vehicle segment, trucks are often segmented separately due to their specific infrastructure and operational needs.

Buses occupy the next position, where wireless modules support applications such as passenger information systems, onboard Wi-Fi, GPS-based route tracking, automated fare collection, and vehicle health monitoring. As smart public transportation systems gain traction in urban environments, the demand for wireless connectivity in buses is increasing, though not yet on the scale of passenger or commercial vehicles.

At the lower end of the adoption scale are motorcycles. Wireless module integration in motorcycles is still relatively limited due to cost sensitivity and space constraints. However, growth is emerging in high-end and electric motorcycles where GPS tracking, anti-theft systems, and smartphone-based vehicle control apps are becoming more common. Despite the potential, the motorcycle segment currently accounts for a smaller share of the overall wireless module market.

Segmentation Insights by Application

On the basis of application, the global transportation wireless module market is bifurcated into fleet management, passenger information systems, vehicle tracking & telematics, public transportation management, and logistics & supply chain management.

In the transportation wireless module market, fleet management is the most dominant application segment. This dominance is driven by the increasing need among transportation companies to monitor and manage large fleets efficiently in real time. Wireless modules are crucial for enabling GPS tracking, fuel usage monitoring, driver behavior analysis, predictive maintenance, and route optimization. These capabilities help reduce operational costs and improve service delivery, making fleet management a cornerstone application for wireless connectivity in transportation.

Following fleet management, vehicle tracking & telematics is a major application area. While it overlaps with fleet management, this segment focuses more on individual vehicle performance, location tracking, diagnostics, and data analytics. Telematics systems powered by wireless modules provide insights into engine health, emissions, idle time, and trip history. These solutions are widely adopted in both private and commercial vehicles to enhance safety, compliance, and maintenance schedules.

Logistics & supply chain management is another critical and fast-growing application. Wireless modules play a pivotal role in tracking goods in transit, managing inventory, and monitoring environmental conditions such as temperature and humidity for perishable items. The integration of IoT and wireless sensors has revolutionized supply chain visibility, particularly for e-commerce, cold chain logistics, and time-sensitive deliveries. Companies rely on this technology to ensure the accuracy, speed, and security of product deliveries across global networks.

Public transportation management follows next, focusing on optimizing the operation of buses, subways, trams, and other mass transit systems. Wireless modules enable central command centers to monitor schedules, vehicle locations, passenger loads, and maintenance needs in real time. This helps cities improve route planning, reduce congestion, and enhance the commuter experience. Adoption is particularly strong in smart cities and regions investing in digital infrastructure for public transport.

At the lower end is passenger information systems, which use wireless modules to deliver real-time updates about vehicle locations, arrival times, route changes, and service alerts to commuters. These systems are commonly used in buses, trains, and stations, enhancing transparency and customer satisfaction. However, the segment's market size is relatively smaller compared to the operationally critical applications like fleet and logistics management, which deliver higher ROI and efficiency gains.

Segmentation Insights by End-user

On the basis of end-user, the global transportation wireless module market is bifurcated into automotive, logistics & transportation, public transit, airport operations, and railway.

In the transportation wireless module market, the automotive sector is the most dominant end-user segment. This is largely driven by the rapid advancement and integration of connected car technologies. Automakers are equipping vehicles—especially passenger cars and commercial vehicles—with wireless modules for applications such as telematics, vehicle-to-everything (V2X) communication, infotainment, diagnostics, and over-the-air (OTA) updates. The push toward autonomous driving, smart mobility, and electric vehicles further amplifies the demand for robust wireless communication solutions in this sector.

Following closely is the logistics & transportation segment, where wireless modules are essential for tracking shipments, optimizing delivery routes, monitoring fleet performance, and ensuring timely delivery. The rise of e-commerce and demand for real-time visibility in supply chains have made wireless-enabled fleet and asset management indispensable. Whether it's freight carriers, courier services, or third-party logistics providers, the industry relies heavily on wireless connectivity for operational efficiency and customer satisfaction.

Public transit is another key end-user, utilizing wireless modules to manage city bus networks, metro systems, and trams. These modules support real-time vehicle tracking, automated fare collection, route optimization, and passenger information systems. Smart city initiatives and the growing need for sustainable, efficient public transport systems are driving the adoption of wireless technology in this segment, although at a slower rate compared to private automotive and logistics sectors.

Airport operations follow, with wireless modules deployed across various airport functions, including ground vehicle tracking, baggage handling systems, personnel coordination, and real-time communication between terminals and aircraft. Wireless infrastructure helps improve airport efficiency, reduce delays, and enhance safety and security. However, its usage is typically more centralized and infrastructure-heavy, which limits the number of deployed wireless modules compared to vehicle-centric applications.

Lastly, the railway segment holds a smaller share of the market but is gradually increasing adoption. Wireless modules in railways support train control systems, signaling, track monitoring, onboard connectivity for passengers, and communication-based train control (CBTC). While the implementation of wireless technology in railways is growing—especially in high-speed and urban rail systems—its pace is slower due to legacy infrastructure and high capital investment requirements.

Transportation Wireless Module Market: Regional Insights

- North America is expected to dominates the global market

The North America region is the most dominant in the transportation wireless module market. This leadership is driven by the widespread integration of advanced telematics, vehicle-to-everything (V2X) technologies, and strong demand for autonomous and electric vehicles. The presence of major automotive OEMs and technology firms, combined with government mandates supporting vehicle connectivity and safety, accelerates the deployment of wireless modules across commercial fleets and passenger vehicles. The U.S. and Canada also have a mature infrastructure for intelligent transportation systems, further solidifying the region’s leading position.

The Asia Pacific region ranks second in the market, with significant momentum coming from China, Japan, South Korea, and India. The region’s rapid urbanization, large-scale adoption of electric vehicles, and investments in smart city infrastructure are fueling demand for transportation wireless modules. China stands out due to its leadership in EV production and 5G expansion, while Japan and South Korea contribute with innovations in automotive connectivity and strong collaborations between automakers and telecom providers. The growing need for efficient transport systems in densely populated cities also supports this growth.

Europe follows closely, driven by strong regulatory support for sustainable transportation and smart mobility. Initiatives promoting connected and cooperative intelligent transport systems are pushing automakers to adopt wireless modules for navigation, safety, and communication applications. Countries such as Germany, France, and the UK are at the forefront, integrating advanced modules into both public and private vehicles. Europe's focus on reducing emissions and promoting digital infrastructure in transportation helps maintain its competitive share in the global market.

Latin America is gradually advancing in the transportation wireless module market, particularly in Brazil, Mexico, and Argentina. Although infrastructure limitations and economic constraints exist, there is a growing interest in connected fleet solutions among logistics companies and urban transport services. Increased smartphone use, improving 4G coverage, and rising awareness of digital fleet management tools are creating pockets of opportunity, particularly in metropolitan regions undergoing modernization.

Middle East and Africa is the least dominant region but is showing early signs of growth, especially in the Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia. These nations are investing in digital transformation and smart city projects that include connected transportation systems. However, broader regional challenges such as limited transport infrastructure and digital connectivity continue to restrict growth. Despite this, pilot programs in smart logistics and connected transit hint at potential future expansion.

Transportation Wireless Module Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the transportation wireless module market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global transportation wireless module market include:

- Sierra Wireless

- Gemalto (Thales Group)

- Quectel

- Telit

- Huawei

- Sunsea Group

- LG Innotek

- U-blox

- Fibocom wireless Inc.

- Neoway

The global transportation wireless module market is segmented as follows:

By Component

- Hardware

- Software

- Services

- Cloud-based Solutions

- Network Infrastructure

By Technology

- Cellular Technology

- Satellite Communication

- Wi-Fi

- Bluetooth

- LoRaWAN

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Trucks

- Buses

- Motorcycles

By Application

- Fleet Management

- Passenger Information Systems

- Vehicle Tracking and Telematics

- Public Transportation Management

- Logistics and Supply Chain Management

By End-user

- Automotive

- Logistics and Transportation

- Public Transit

- Airport Operations

- Railway

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Transportation Wireless Module

Request Sample

Transportation Wireless Module