Vegan Makeup Market Size, Share, and Trends Analysis Report

CAGR :

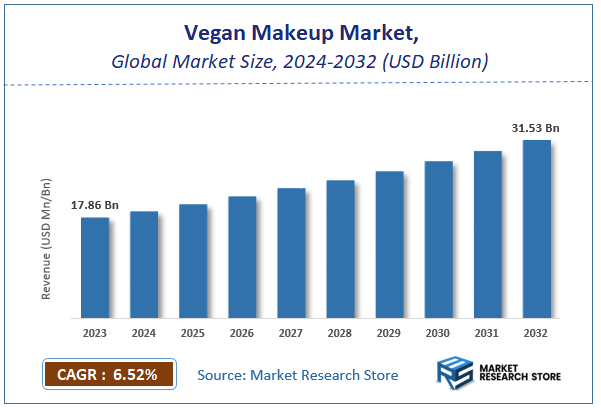

| Market Size 2023 (Base Year) | USD 17.86 Billion |

| Market Size 2032 (Forecast Year) | USD 31.53 Billion |

| CAGR | 6.52% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Vegan Makeup Market Insights

According to Market Research Store, the global vegan makeup market size was valued at around USD 17.86 billion in 2023 and is estimated to reach USD 31.53 billion by 2032, to register a CAGR of approximately 6.52% in terms of revenue during the forecast period 2024-2032.

The vegan makeup report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Vegan Makeup Market: Overview

Vegan makeup refers to cosmetic products formulated without any animal-derived ingredients or by-products, such as beeswax, lanolin, carmine, collagen, or animal-based glycerin. Instead, these products use plant-based, mineral-based, or synthetic alternatives to achieve the desired texture, color, and performance. Vegan makeup is often associated with cruelty-free practices, meaning the products and their ingredients are not tested on animals, although the terms “vegan” and “cruelty-free” are not synonymous and may vary depending on brand policies and certification standards.

The growth of the vegan makeup market is driven by rising consumer awareness around animal welfare, environmental sustainability, and health-conscious beauty practices. As more individuals seek ethical and transparent beauty options, brands are responding by reformulating products, securing vegan certifications, and emphasizing clean, natural ingredients. Social media and influencer marketing have also played a pivotal role in promoting vegan beauty trends, especially among younger, eco-conscious consumers. Additionally, regulatory shifts and increased availability of high-performance plant-based ingredients are enabling vegan makeup to rival traditional cosmetics in quality and efficacy. With growing demand for ethical consumerism, the vegan makeup segment continues to expand within the broader clean beauty and sustainable skincare movements.

Key Highlights

- The vegan makeup market is anticipated to grow at a CAGR of 6.52% during the forecast period.

- The global vegan makeup market was estimated to be worth approximately USD 17.86 billion in 2023 and is projected to reach a value of USD 31.53 billion by 2032.

- The growth of the vegan makeup market is being driven by the growing health and environmental consciousness are playing a crucial role.

- Based on the product type, the face makeup segment is growing at a high rate and is projected to dominate the market.

- On the basis of distribution channel, the online retail segment is projected to swipe the largest market share.

- In terms of consumer demographics, the age group segment is expected to dominate the market.

- Based on the product formulation, the organic ingredients segment is expected to dominate the market.

- Based on the purchase behavior, the loyal customers segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Vegan Makeup Market: Dynamics

Key Growth Drivers:

- Rising Consumer Awareness of Animal Welfare and Cruelty-Free Practices: A primary driver is the increasing global awareness and concern among consumers regarding animal testing and the use of animal-derived ingredients in cosmetics. This ethical shift, particularly strong among Millennials and Gen Z, drives demand for products certified as "cruelty-free" and "vegan."

- Growing Health and Environmental Concerns: Consumers are becoming more conscious of the ingredients in their beauty products and their environmental impact. Vegan makeup is often perceived as "cleaner" and safer, with a focus on plant-based, natural, and non-toxic formulations, appealing to those seeking healthier and more sustainable options.

- Influence of Social Media and Celebrity Endorsements: Social media platforms (Instagram, TikTok, YouTube) and beauty influencers play a crucial role in promoting vegan makeup brands and products. Celebrity endorsements and viral trends surrounding ethical and sustainable beauty further amplify consumer interest and drive adoption.

- Expanding Vegan and Plant-Based Lifestyles: The increasing adoption of veganism as a lifestyle choice, extending beyond diet to encompass all consumer goods, naturally fuels the demand for vegan makeup. This expanding demographic consistently seeks products aligned with their core values.

- Innovations in Formulation and Product Efficacy: Manufacturers are continuously investing in R&D to develop high-performance vegan formulations that rival or even surpass conventional makeup in terms of pigment, longevity, texture, and application. These technological advancements are overcoming previous perceptions of vegan makeup lacking efficacy.

- Supportive Regulatory Landscape: A growing number of countries and regions (e.g., EU, India, parts of the US) are implementing or strengthening bans on animal testing for cosmetics. This regulatory push encourages brands to adopt cruelty-free and vegan practices, accelerating market growth.

- Wider Availability and Accessibility through E-commerce: The expansion of e-commerce platforms and online specialty stores has made vegan makeup more accessible to a global audience. Online channels, including direct-to-consumer (D2C) brand websites, allow niche and emerging vegan brands to reach a wider customer base without extensive physical retail presence.

Restraints:

- Higher Production Costs and Price Sensitivity: Sourcing high-quality, ethically produced plant-based ingredients can be more expensive than traditional animal-derived or synthetic alternatives. This often results in higher production costs, leading to premium pricing for vegan makeup, which can be a restraint for price-sensitive consumers, especially in developing markets.

- Perception of Inferior Performance or Shorter Shelf Life: Despite advancements, some consumers still hold a skepticism that vegan makeup may not perform as well (e.g., less vibrant colors, shorter wear time) or have a shorter shelf life compared to conventional products, due to the absence of certain binders or preservatives traditionally found in non-vegan items.

- Complex and Inconsistent Certification and Labeling: The lack of a single, universally standardized "vegan" certification across all regions can lead to consumer confusion and skepticism. Different certification bodies (e.g., Vegan Society, PETA, Leaping Bunny) have varied criteria, making it challenging for consumers to easily identify truly vegan and cruelty-free products.

- Supply Chain Challenges for Natural and Plant-Based Ingredients: Sourcing consistent, high-quality, and sustainable plant-based ingredients can be complex. Factors like agricultural yield, seasonality, climate change, and ethical sourcing practices can lead to supply chain disruptions and impact ingredient availability and cost.

- Limited Retail Presence in Traditional Channels: While e-commerce is strong, dedicated brick-and-mortar retail space for vegan makeup, especially outside of major metropolitan areas, can still be limited. This can hinder product discovery and accessibility for consumers who prefer to try products in person.

- Competition from "Clean Beauty" and "Natural" Brands (without being strictly vegan): Many brands market themselves as "natural" or "clean" but may still contain animal-derived ingredients or conduct animal testing. This can create a blurred line for consumers and divert potential vegan makeup buyers.

- Counterfeit Products and Brand Authenticity Concerns: The rising popularity of vegan makeup also attracts counterfeiters. The availability of fake products online can erode consumer trust in legitimate vegan brands and undermine the integrity of the market.

Opportunities:

- Hyper-Personalization and AI-Driven Formulations: Leveraging AI and machine learning to analyze consumer skin types, preferences, and ethical concerns can lead to the creation of highly personalized vegan makeup solutions. This could include custom-blended foundations or personalized product recommendations.

- Expansion into Emerging Markets: As awareness of ethical and sustainable living grows in rapidly developing economies (e.g., India, Southeast Asia, parts of Latin America), there's a significant opportunity for vegan makeup brands to expand their presence and cater to these new consumer bases.

- Sustainable Packaging Innovation: With a strong alignment between veganism and environmentalism, there's a huge opportunity for brands to lead in sustainable packaging solutions (e.g., refillable systems, biodegradable materials, zero-waste packaging), differentiating themselves and appealing to eco-conscious consumers.

- Development of Hybrid and Multi-Benefit Products: Creating vegan makeup products that offer additional skincare benefits (e.g., serum foundations, hydrating lip tints) or multi-use functionality can appeal to consumers looking for simplified routines and added value.

- Strategic Partnerships and Collaborations: Collaborations between vegan makeup brands, influencers, environmental organizations, and even non-vegan brands looking to diversify their offerings can help expand market reach, share expertise, and innovate new product categories.

- Targeting the Male Grooming Segment: The increasing interest of men in cosmetic and grooming products, coupled with growing awareness of ethical consumption, presents a significant opportunity for vegan makeup brands to develop specific product lines tailored to the male grooming market.

- Blockchain for Transparency and Traceability: Implementing blockchain technology can provide unparalleled transparency regarding ingredient sourcing, manufacturing processes, and certification status, building deeper trust with consumers who demand authenticity and ethical accountability.

Challenges:

- Maintaining Consistency and Performance of Natural Ingredients: Plant-based ingredients can sometimes be more volatile or less consistent than synthetic alternatives. The challenge lies in formulating vegan makeup that delivers consistent color, texture, and longevity across batches, especially with natural variations in raw materials.

- Stringent Allergen Management: While often perceived as "natural," plant-based ingredients can still be allergens for some individuals. Rigorous testing and clear labeling are crucial to manage potential allergic reactions and ensure product safety for a diverse consumer base.

- Navigating Complex and Evolving Regulatory Landscape Globally: As the market grows, new regulations concerning vegan claims, ingredient restrictions, and marketing practices may emerge in different countries. Staying compliant with this fragmented and evolving regulatory environment is a significant challenge for international brands.

- Educating Consumers on the "Why" Behind Vegan Makeup: While awareness is growing, many consumers still don't fully understand the difference between "vegan" and "cruelty-free" or the specific benefits of vegan formulations. Continuous consumer education is necessary to drive deeper market penetration.

- Combating Greenwashing and Misleading Claims: The popularity of "vegan" and "clean" labels can lead to "greenwashing" by some brands that make misleading claims without full adherence to vegan principles. This poses a challenge for legitimate vegan brands to differentiate themselves and maintain consumer trust.

- Disposal and Environmental Impact of Packaging: Despite efforts towards sustainability, the sheer volume of packaging used in the cosmetics industry, including vegan makeup, still presents an environmental challenge. Finding truly eco-friendly, scalable, and cost-effective packaging solutions remains a hurdle.

- Talent Acquisition for Specialized Formulators: Developing innovative vegan makeup products requires a specialized skill set in cosmetic chemistry and material science focused on plant-based alternatives. Attracting and retaining formulators with this specific expertise can be challenging.

Vegan Makeup Market: Report Scope

This report thoroughly analyzes the Vegan Makeup Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Vegan Makeup Market |

| Market Size in 2023 | USD 17.86 Billion |

| Market Forecast in 2032 | USD 31.53 Billion |

| Growth Rate | CAGR of 6.52% |

| Number of Pages | 178 |

| Key Companies Covered | Debenhams Plc, e.l.f. Beauty Inc., Estée Lauder Co. Inc., L’Oréal SA, Lush Retail Ltd., Natura &Co, Urban Decay, Ecco Bella |

| Segments Covered | By Product Type, By Distribution Channel, By Consumer Demographics, By Product Formulation, By Purchase Behavior, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Vegan Makeup Market: Segmentation Insights

The global vegan makeup market is divided by product type, distribution channel, consumer demographics, product formulation, purchase behaviour, and region.

Segmentation Insights by Product Type

Based on product type, the global vegan makeup market is divided into face makeup, eye makeup, lip makeup, and nail products.

Face Makeup dominates the Vegan Makeup Market, accounting for a substantial share due to the widespread daily use of products like foundation, concealer, blush, highlighter, and setting powders. These products are in high demand across consumer groups prioritizing clean, cruelty-free ingredients that are gentle on sensitive skin and free from animal-derived substances. The rise of multifunctional vegan face products—such as tinted moisturizers with SPF, anti-aging foundations, and hydrating primers—has driven growth in this segment, especially among health-conscious and environmentally aware consumers. Moreover, brands are offering a broader range of inclusive shades and skin-benefiting formulations, further fueling the adoption of vegan face makeup for both every day and professional use.

Eye Makeup forms a significant segment of the market, driven by the popularity of vegan mascaras, eyeliners, eyeshadows, and brow products that deliver performance without the use of animal by-products such as beeswax, carmine, or silk protein. This segment appeals strongly to trend-savvy and ethical beauty buyers who seek bold pigmentation, long wear, and eye-safe formulations derived from plant-based or mineral ingredients. As clean beauty becomes mainstream, more consumers are looking for vegan eye makeup that is ophthalmologist-tested and suitable for sensitive eyes or contact lens wearers, prompting innovation in waterproof, smudge-proof, and nourishing eye cosmetics.

Lip Makeup represents another key area of growth, with a surge in demand for vegan lipsticks, glosses, balms, and liners free from commonly used animal-derived ingredients like lanolin and carmine. Consumers are increasingly opting for vegan lip products with moisturizing benefits, rich color payoff, and ethical packaging. This shift is reinforced by influencers and beauty brands promoting vegan lip care as part of a more holistic, cruelty-free lifestyle. Product developments focusing on long-lasting color, hydrating natural oils, and sustainable packaging materials continue to broaden this category’s appeal, particularly among young consumers and conscious shoppers.

Nail Products in the vegan category, including polishes, treatments, removers, and nail care kits, are gaining momentum as consumers seek non-toxic, cruelty-free alternatives to traditional nail cosmetics. The demand for vegan nail products is fueled by rising awareness around harmful ingredients like formaldehyde, toluene, and DBP, and the inclusion of nourishing plant-based components such as bamboo extract, kale, and vitamins. Brands are expanding their offerings with quick-dry formulas, breathable polish technology, and eco-friendly packaging, making vegan nail products more competitive in both salon and at-home settings.

Segmentation Insights by Distribution Channel

On the basis of distribution channel, the global vegan makeup market is bifurcated into online retail, brick-and-mortar retail, and direct sales.

Online Retail dominates the Vegan Makeup Market as consumers increasingly prioritize convenience, product variety, and access to niche or indie vegan beauty brands. E-commerce platforms, both multi-brand retailers and direct-to-consumer websites, enable shoppers to explore detailed ingredient lists, certifications (such as cruelty-free or Leaping Bunny approval), and user reviews—key decision factors for ethically conscious buyers. Online distribution also supports the rise of subscription boxes, influencer-led promotions, and exclusive digital launches, which are particularly effective in engaging Gen Z and millennial consumers. Additionally, advanced recommendation engines, virtual try-on tools, and personalized skincare quizzes contribute to the enhanced shopping experience and high conversion rates within this channel.

Brick-and-Mortar Retail remains an important segment, especially for consumers who prefer in-person testing, instant gratification, and tactile engagement with products before purchase. Physical stores—including specialty beauty retailers, department stores, and natural product outlets—offer the opportunity to experience textures, shades, and scents firsthand. Many major beauty retailers now feature dedicated vegan sections, clear labeling, and trained staff to guide shoppers through vegan product options. This channel is especially relevant for new users entering the vegan beauty space, as well as for products like foundations or concealers that often require shade matching. Despite the growth of online retail, the physical store presence continues to reinforce brand trust and visibility.

Direct Sales also plays a notable role, particularly through brand-owned platforms, pop-up events, and social selling by independent consultants. This channel is well-suited to niche vegan beauty brands that focus on building close relationships with their customer base and offering tailored beauty education. Direct-to-consumer models enable greater control over brand messaging, pricing, and sustainability commitments, often appealing to ethically minded consumers who value transparency and authenticity. Live demonstrations, virtual consultations, and storytelling around ingredient sourcing are key features of this distribution method, helping to build loyalty and brand advocacy in the competitive vegan makeup landscape.

Segmentation Insights by Consumer Demographics

On the basis of consumer demographics, the global vegan makeup market is bifurcated into age group, gender, and income level.

Age Group dominates the Vegan Makeup Market, with the 18–35 age demographic—primarily consisting of Gen Z and millennials—driving the majority of demand. This age group is highly responsive to ethical consumption trends, placing strong emphasis on cruelty-free practices, plant-based ingredients, and environmental sustainability. Their buying behavior is heavily influenced by social media platforms, where vegan beauty routines, influencer endorsements, and clean beauty tutorials are widely circulated. Younger consumers also show a preference for brands that promote inclusivity, transparency, and eco-consciousness, often favoring companies that align with their personal values. In addition, this demographic is quick to adopt digital shopping platforms and engage with beauty tech innovations like virtual try-ons and AI-powered skincare recommendations. The combination of ethical awareness, trend adoption, and digital savviness makes this age group the dominant force shaping product development, branding, and marketing strategies within the vegan makeup industry.

Gender segmentation in the vegan makeup market is evolving, with female consumers continuing to represent the largest share, but increasing traction among male and non-binary individuals. Women typically lead demand across all product categories—particularly face and eye makeup—driven by both daily beauty routines and growing concern for ethical sourcing. However, as societal norms shift and gender inclusivity becomes more mainstream in the beauty industry, brands are expanding their offerings to include gender-neutral packaging, marketing, and product design. Male consumers are increasingly exploring vegan cosmetics for subtle grooming, skincare integration, and performance-based formulations that align with personal wellness and ethical values, signaling broadening appeal across gender lines.

Income Level impacts both product preference and frequency of purchase in the vegan makeup market. Higher-income consumers are more inclined to buy premium vegan brands that emphasize luxurious ingredients, sustainable sourcing, and elevated packaging. These buyers often expect advanced formulations, high product performance, and exclusive brand experiences, supporting the growth of the luxury vegan segment. Meanwhile, middle-income consumers contribute significantly to market volume, especially as mass-market brands introduce budget-friendly vegan alternatives. Affordable price points, combined with accessible retail channels, allow ethically conscious consumers across a wider economic spectrum to participate in the market, reinforcing inclusive growth.

Segmentation Insights by Product Formulation

On the basis of product formulation, the global vegan makeup market is bifurcated into organic ingredients, mineral-based products, plant-derived ingredients, and alcohol-free formulas.

Organic Ingredients dominate the Vegan Makeup Market due to their strong alignment with consumer demand for clean, safe, and environmentally responsible beauty products. These formulations are crafted from certified organic botanical sources, such as fruits, herbs, and seeds, cultivated without synthetic chemicals or GMOs. Consumers, particularly within the 18–35 age group, are increasingly drawn to organic vegan makeup for its transparency, minimal skin irritation risk, and compatibility with sensitive skin types. Organic ingredients like organic jojoba oil, aloe vera, chamomile, and rosehip extract offer multifunctional benefits, such as hydration, anti-aging, and anti-inflammatory effects, making them a preferred choice across face, eye, and lip makeup products. Additionally, the presence of organic certifications and eco-friendly packaging further boosts credibility and appeal, helping brands differentiate themselves in a saturated market.

Mineral-Based Products hold significant market presence as well, particularly among consumers who prioritize gentle, skin-beneficial formulations. These products utilize natural minerals such as mica, zinc oxide, and titanium dioxide to deliver breathable coverage and sun protection while avoiding synthetic additives, fragrances, and dyes. Mineral-based vegan makeup is favored for its non-comedogenic qualities, making it ideal for individuals with acne-prone or sensitive skin. The lightweight texture and skin-soothing properties have led to increased adoption in foundations, setting powders, and blushes, with continued innovation around natural pigmentation and wearability.

Plant-Derived Ingredients form the essential foundation of most vegan makeup formulations, offering a broad spectrum of skincare benefits through botanical extracts and oils. Ingredients such as green tea, calendula, coconut oil, and shea butter provide hydration, nourishment, and antioxidant protection, while replacing conventional animal-derived components. These ingredients not only cater to the ethical preferences of vegan consumers but also fulfill the demand for high-performance cosmetics with natural actives. Plant-based formulations are especially prevalent in lipsticks, mascaras, and skincare-infused makeup hybrids, reinforcing the market’s emphasis on ingredient integrity and wellness.

Alcohol-Free Formulas are also gaining traction, particularly among users with dry or reactive skin who seek gentle alternatives to traditional cosmetics. By excluding harsh alcohols that can dehydrate or irritate, these vegan makeup formulations deliver a more comfortable wear and skin-friendly application experience. Instead, alcohol-free products rely on hydrating agents and botanical extracts to preserve formula stability and enhance absorption. The rising demand for alcohol-free vegan makeup is evident in categories such as setting sprays, foundations, and concealers, where skin tolerance and prolonged wear are critical consumer priorities.

Segmentation Insights by Purchase Behavior

On the basis of purchase behavior, the global vegan makeup market is bifurcated into. loyal customers, occasional buyers, impulse purchasers, and trial users

Loyal Customers dominate the Vegan Makeup Market and form the backbone of consistent sales for many ethical beauty brands. These consumers are deeply committed to cruelty-free living and often align their personal values with the products they purchase. They usually follow a vegan lifestyle or actively seek out plant-based, non-toxic, and sustainable beauty alternatives. Loyal customers frequently research ingredient transparency, sustainability certifications, and brand ethics before making a purchase and tend to stick with brands that maintain high standards in formulation, packaging, and sourcing. They also engage with brands on social media, participate in referral programs, and contribute to word-of-mouth promotion, acting as brand ambassadors. Their willingness to pay premium prices for ethically aligned products makes them particularly valuable in driving both profitability and brand equity in the long term.

Occasional Buyers are an important secondary segment within the Vegan Makeup Market, purchasing products less frequently and usually in response to specific needs such as seasonal changes, promotional events, or personal milestones. These consumers may not follow a strictly vegan or clean beauty regimen but are interested in the benefits of specific vegan makeup products—such as improved skin health, hypoallergenic properties, or eco-friendly ingredients. Their buying decisions are influenced by accessibility, positive reviews, product availability in mainstream retail, and competitive pricing. Although they lack the same level of brand commitment as loyal customers, they offer conversion potential through positive product experiences, especially if brands focus on education, sample offerings, and accessible customer service.

Impulse Purchasers add dynamism to the Vegan Makeup Market, making spontaneous buying decisions based on visual appeal, packaging, influencer endorsements, or trending social media content. They are typically drawn to eye-catching displays in stores or digital campaigns on platforms like Instagram, TikTok, and YouTube. These buyers often explore new product lines, limited editions, or celebrity collaborations without long-term consideration of ingredients or brand philosophy. While their engagement may be short-term, their behavior is valuable for market buzz and short-cycle sales, especially during product launches, holidays, or promotional windows. Brands targeting impulse purchasers benefit from attention-grabbing visuals, user-generated content, and persuasive storytelling that evokes emotion and immediacy.

Trial Users represent a gateway audience for the Vegan Makeup Market, comprising individuals who are testing vegan products for the first time due to health concerns, curiosity, or influence from friends and media. They typically begin with travel-sized products, sample kits, or lower-cost items to evaluate product quality, texture, performance, and skin compatibility. Trial users are highly influenced by packaging clarity, product education, and in-store or online support that guides them through usage and ingredient benefits. Although their initial engagement is exploratory, they hold long-term potential to become loyal customers if their initial experiences are positive. Brands that offer easy returns, educational resources, and clean branding are best positioned to convert trial users into recurring buyers.

Vegan Makeup Market: Regional Insights

- North America is expected to dominate the global market

North America dominate the vegan makeup market globally due to a combination of heightened consumer awareness, progressive regulatory environments, and a mature clean beauty industry infrastructure. The U.S. and Canada have seen a significant rise in demand for cruelty-free, plant-based cosmetics driven by socially conscious millennials and Gen Z consumers who actively seek products aligned with their ethical values. This demographic prioritizes transparency in ingredient sourcing and demands certifications like PETA and Leaping Bunny, which many brands now prominently feature. Retail giants such as Sephora, Ulta Beauty, and drugstore chains like CVS and Walgreens have expanded their vegan beauty aisles and e-commerce offerings to meet this growing demand. Influencer marketing and social media campaigns emphasizing vegan lifestyles have also contributed to consumer education and market penetration. Additionally, legacy cosmetic brands and newer indie brands alike are innovating with sustainable packaging and formulation technologies to reduce environmental impact, which resonates strongly with North American consumers. The region benefits from well-developed supply chains and logistics networks, enabling fast product launches and accessibility nationwide. Government regulations that discourage animal testing further create a favorable environment for vegan makeup brands to flourish.

Europe holds a significant share of the vegan makeup market, underpinned by strict EU regulations that prohibit animal testing on cosmetics and increasingly stringent environmental policies. Countries such as the United Kingdom, Germany, France, and Italy represent mature and influential markets where consumers place strong emphasis on product safety, ethical manufacturing, and sustainability. European consumers are particularly discerning, favoring brands that combine vegan formulations with organic and natural ingredients, as well as sustainable and recyclable packaging solutions. Iconic brands such as Lush, The Body Shop, and Charlotte Tilbury have led the way by introducing extensive vegan ranges and embracing eco-conscious marketing strategies. The EU’s Green Deal and other sustainability frameworks have spurred brands to reduce carbon footprints and waste, encouraging innovation in biodegradable packaging and refillable cosmetics. Additionally, European consumers often seek certifications from recognized bodies such as Vegan Society and Cruelty Free International, which reinforce brand credibility. The rise of minimalist beauty trends and ‘skinimalism’ further boosts demand for multi-functional vegan makeup products that are gentle on the skin and free of harsh chemicals.

Asia-Pacific is the fastest-growing region for vegan makeup, with a surge driven by urbanization, rising disposable incomes, and a younger population eager to adopt global beauty trends that emphasize wellness and sustainability. South Korea and Japan, both major beauty innovation hubs, are integrating vegan and clean beauty concepts into their established skincare and makeup lines, focusing on high efficacy combined with ethical sourcing. The K-beauty wave has helped popularize natural ingredients and cruelty-free claims, which resonate well with younger consumers. Australia and India are witnessing growing interest in plant-based cosmetics as consumers become more health-conscious and environmentally aware. E-commerce penetration is a major catalyst in Asia-Pacific, with platforms like Tmall, Shopee, and Amazon accelerating access to international and local vegan makeup brands. Social media influencers and beauty bloggers educate consumers on ingredient transparency, product benefits, and animal welfare, boosting market growth. However, regulatory landscapes vary widely across countries, with some markets still developing clear standards for vegan certification, posing challenges for brand consistency. Despite this, the increasing popularity of natural and organic beauty, combined with cultural shifts toward ethical consumption, underpins robust regional expansion.

Latin America is an emerging market in vegan makeup, with Brazil and Mexico driving most of the regional growth. This region’s rising middle class, expanding internet and smartphone penetration, and increasing consumer exposure to global beauty trends have spurred interest in clean, cruelty-free products. Younger demographics in urban centers are particularly drawn to vegan makeup as part of a broader lifestyle shift toward health and sustainability. Local brands are beginning to develop vegan product lines, while international brands are expanding their presence through e-commerce and specialty retail stores. Challenges remain due to fragmented distribution channels, varying regulatory standards, and consumer education gaps, especially outside metropolitan areas. However, social media campaigns by influencers and NGOs promoting animal rights and environmental sustainability are making an impact. The region also shows growing demand for eco-friendly packaging and refillable cosmetics, signaling opportunities for innovation. Additionally, cultural appreciation for natural and herbal ingredients aligns well with vegan makeup formulations, aiding acceptance.

Middle East and Africa show steady, though nascent, growth in the vegan makeup market. The GCC countries, including the UAE, Saudi Arabia, and Qatar, are at the forefront in the Middle East, supported by high per capita incomes, a young population, and increasing demand for luxury and ethical beauty products. Consumers in this region often seek halal-compliant and vegan-certified makeup products, merging religious and ethical standards. Luxury e-commerce platforms and regional retailers have started to curate extensive vegan beauty collections, featuring both international and homegrown brands. In Africa, South Africa is the most developed market for vegan cosmetics, driven by a growing eco-conscious middle class and increased access to online shopping. Challenges in these regions include limited availability of products in rural areas, higher prices due to import costs, and infrastructural issues affecting distribution. However, rising awareness campaigns, expanding fintech payment solutions, and growing interest in sustainability and health create promising conditions for market expansion. Brands that offer localized marketing, culturally relevant formulations, and educational initiatives are better positioned to capitalize on these opportunities.

Vegan Makeup Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the vegan makeup market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global vegan makeup market include:

- Debenhams Plc

- e.l.f. Beauty Inc.

- Estée Lauder Co. Inc.

- L’Oréal SA

- Lush Retail Ltd.

- Natura &Co

- Urban Decay

- Ecco Bella

The global vegan makeup market is segmented as follows:

By Product Type

- Face Makeup

- Eye Makeup

- Lip Makeup

- Nail Products

By Distribution Channel

- Online Retail

- Brick-and-Mortar Retail

- Direct Sales

By Consumer Demographics

- Age Group

- Gender

- Income Level

By Product Formulation

- Organic Ingredients

- Mineral-Based Products

- Plant-Derived Ingredients

- Alcohol-Free Formulas

By Purchase Behavior

- Loyal Customers

- Occasional Buyers

- Impulse Purchasers

- Trial Users

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Vegan Makeup

Request Sample

Vegan Makeup