Vinyl Sulphone Ester Market Size, Share, and Trends Analysis Report

CAGR :

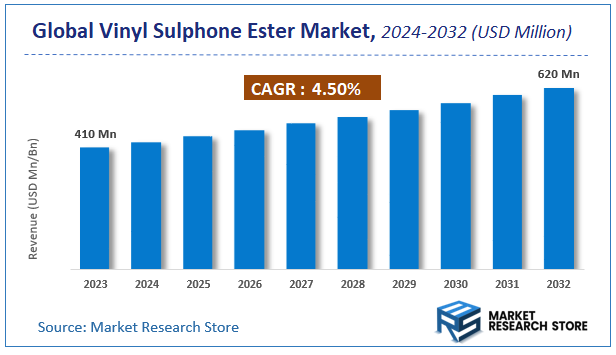

| Market Size 2023 (Base Year) | USD 410 Million |

| Market Size 2032 (Forecast Year) | USD 620 Million |

| CAGR | 4.5% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Vinyl Sulphone Ester Market Insights

According to Market Research Store, the global vinyl sulphone ester market size was valued at around USD 410 million in 2023 and is estimated to reach USD 620 million by 2032, to register a CAGR of approximately 4.5% in terms of revenue during the forecast period 2024-2032.

The vinyl sulphone ester report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Vinyl Sulphone Ester Market: Overview

Vinyl sulphone ester is a chemical compound commonly used in various industrial and chemical applications, particularly in the production of dyes and textiles. It serves as an intermediate in the manufacturing of reactive dyes, where it helps in creating stable covalent bonds with fibers, ensuring color durability and fastness. The compound is also used in the synthesis of other chemicals, including those used in pharmaceuticals and agrochemicals. Vinyl sulphone ester’s role as a versatile intermediate in the textile and dye industries makes it essential for applications requiring strong and long-lasting colorants.

Key Highlights

- The vinyl sulphone ester market is anticipated to grow at a CAGR of 4.5% during the forecast period.

- The global vinyl sulphone ester market was estimated to be worth approximately USD 410 million in 2023 and is projected to reach a value of USD 620 million by 2032.

- The growth of the vinyl sulphone ester market is being driven by the increasing demand for reactive dyes in the textile industry.

- Based on the product type, the vinyl sulphone ester A segment is growing at a high rate and is projected to dominate the market.

- On the basis of end-use industry, the textile industry segment is projected to swipe the largest market share.

- In terms of application, the textile dyeing & printing segment is expected to dominate the market.

- Based on the distribution channel, the direct sales segment is expected to dominate the market.

- In terms of form, the powder segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Vinyl Sulphone Ester Market: Dynamics

Key Growth Drivers:

- Rising Demand in Textile Industry: Vinyl sulphone esters are widely used in textile and dyeing processes, particularly for reactive dyes. The growth of the textile industry, especially in developing countries, is fueling the demand for vinyl sulphone esters.

- Growth of the Apparel Market: The increasing demand for fashion and apparel, driven by changing consumer preferences and rising disposable incomes, has significantly boosted the need for vinyl sulphone esters in dyeing processes.

- Increasing Awareness of Eco-friendly Dyes: Vinyl sulphone esters are used in the production of reactive dyes, which are considered more environmentally friendly compared to other dyeing agents. This shift toward sustainable and eco-friendly dyes is a key factor driving the market growth.

- Expansion of the Chemical Industry: As the chemical industry continues to expand, the demand for vinyl sulphone esters in various applications, including paints, coatings, and adhesives, is growing, driving the market forward.

- Technological Advancements in Dyeing Techniques: The development of advanced dyeing techniques that use vinyl sulphone esters is enhancing efficiency and reducing environmental impact, further boosting their demand in textile and related industries.

Restraints:

- High Manufacturing Costs: The production of vinyl sulphone esters involves complex chemical processes, making it more expensive to manufacture compared to other chemical alternatives. This can limit the growth of the market, particularly in cost-sensitive applications.

- Regulatory Challenges: Stringent environmental and safety regulations in certain regions can pose challenges to the production and use of vinyl sulphone esters, particularly in the chemical and textile industries.

- Fluctuating Raw Material Prices: The prices of raw materials used to produce vinyl sulphone esters can be volatile, which may affect the overall cost structure and availability of the product, posing a restraint to the market.

Opportunities:

- Growing Textile Export Markets: As textile manufacturing in developing countries increases, particularly in regions such as Asia-Pacific and Africa, there is a growing opportunity for vinyl sulphone ester manufacturers to tap into emerging markets.

- Expansion in the Emerging Markets: The expansion of vinyl sulphone ester usage in emerging markets, where industrialization and urbanization are driving the growth of the textile and chemical industries, presents significant growth potential.

- Research and Development in Dyeing Technologies: Ongoing R&D in dyeing technologies that integrate vinyl sulphone esters is creating new applications, improving product quality, and reducing environmental impact. This opens up new opportunities for innovation and growth.

- Rising Focus on Eco-friendly and Sustainable Products: The increasing consumer demand for sustainable and eco-friendly products, particularly in textiles and consumer goods, is pushing industries to adopt greener alternatives, which presents opportunities for vinyl sulphone esters.

Challenges:

- Competition from Alternative Dyes: The market faces competition from alternative dyes and chemicals that offer similar properties to vinyl sulphone esters but may be more cost-effective or simpler to produce.

- Environmental Concerns and Toxicity Issues: While vinyl sulphone esters are used in more eco-friendly dyeing processes, their production and use still raise concerns regarding toxicity and environmental impact, especially if not properly managed.

- Dependence on Key Suppliers: The vinyl sulphone ester market relies heavily on a few key suppliers of raw materials. Disruptions in the supply chain, whether due to geopolitical factors or market conditions, can lead to shortages or price fluctuations.

- Limited Awareness in Non-Textile Industries: The use of vinyl sulphone esters outside the textile industry is still relatively limited. Increasing awareness and applications in other industries, such as paints, coatings, and adhesives, could be challenging.

Vinyl Sulphone Ester Market: Report Scope

This report thoroughly analyzes the Vinyl Sulphone Ester Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Vinyl Sulphone Ester Market |

| Market Size in 2023 | USD 410 Million |

| Market Forecast in 2032 | USD 620 Million |

| Growth Rate | CAGR of 4.5% |

| Number of Pages | 173 |

| Key Companies Covered | Matangi Industries, EMCO Dyestuff, BHAGERIA INDUSTRIE, Nanjing Chem Import and Export, BHIMANI CHEMICALS, Henan Xinxiang Weixing Dyestuff Chemical Plant, Crystal Quinone |

| Segments Covered | By Product Type, By End-Use Industry, By Application, By Distribution Channel, By Form, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Vinyl Sulphone Ester Market: Segmentation Insights

The global vinyl sulphone ester market is divided by product type, end-use industry, application, distribution channel, form, and region.

Segmentation Insights by Product Type

Based on product type, the global vinyl sulphone ester market is divided into vinyl sulphone ester A, vinyl sulphone ester B, and vinyl sulphone ester C.

In the vinyl sulphone ester market, Vinyl Sulphone Ester A emerges as the most dominant product type segment. This dominance can be attributed to its superior reactivity and compatibility with a wide range of reactive dyes, particularly in the textile industry. Vinyl Sulphone Ester A is extensively used in dye formulations for cotton and other cellulosic fibers, where it imparts excellent wash fastness, bright shades, and long-term stability. Its well-balanced molecular structure makes it ideal for achieving high fixation rates during the dyeing process, which in turn supports mass adoption across various textile manufacturing hubs, especially in Asia-Pacific regions.

Vinyl Sulphone Ester B holds the second position in the market. It is characterized by a slightly different functional group structure that offers unique application benefits in niche textile segments, including blended fabrics. Although it doesn’t match the wide-scale applicability of Ester A, its usage is growing among manufacturers looking to diversify colorfastness properties in challenging dyeing environments. Additionally, Vinyl Sulphone Ester B is being explored for its potential in ink formulations, adding to its versatility in select downstream industries.

Vinyl Sulphone Ester C is currently the least dominant segment. It is used in more specialized or limited applications where specific solubility or reactivity parameters are needed. Ester C typically finds relevance in research-based dye formulations or in smaller-scale manufacturing units where customized dye properties are essential. While its demand is relatively low, it still maintains a consistent niche presence, supported by industries focusing on tailored dye solutions or environmental compliance experiments.

Segmentation Insights by End-Use Industry

On the basis of end-use industry, the global vinyl sulphone ester market is bifurcated into textile industry, pharmaceutical industry, chemicals manufacturing, and water treatment industry.

In the vinyl sulphone ester market, the textile industry stands out as the most dominant end-use industry segment. This dominance is primarily driven by the widespread use of vinyl sulphone esters as reactive intermediates in the formulation of dyes, particularly for dyeing cellulose-based fibers like cotton and viscose. The high reactivity and excellent wash and light fastness properties of vinyl sulphone-based dyes make them ideal for large-scale textile production. With the global textile market expanding rapidly—especially in regions like Asia-Pacific—the demand for vinyl sulphone esters continues to be robust and consistent.

Following the textile sector, the chemicals manufacturing industry holds the second most prominent share. Vinyl sulphone esters are utilized as key intermediates in various chemical synthesis processes. Their ability to form stable covalent bonds with nucleophiles makes them valuable in manufacturing specialty chemicals and intermediates, including advanced organic compounds used in industrial applications. Though this segment is not as large as textiles, its steady demand stems from the consistent need for specialty chemicals across multiple industries.

The pharmaceutical industry ranks next in terms of end-use. Here, vinyl sulphone esters are occasionally used in the synthesis of biologically active compounds and in the development of certain drug intermediates. Their selective reactivity and stability make them suitable for research and development in medicinal chemistry, though their use is more limited compared to broader industrial sectors. Growth in this segment is often tied to innovation and specific drug development initiatives.

Lastly, the water treatment industry represents the least dominant segment. While vinyl sulphone esters may be used in the synthesis of compounds for water purification or treatment agents, their application here remains minimal. The industry generally relies on more traditional or cost-effective chemicals for large-scale operations. Nonetheless, there is potential for this segment to grow, especially if new water treatment formulations emerge that require vinyl sulphone-based chemistries.

Segmentation Insights by Application

Based on application, the global vinyl sulphone ester market is divided into textile dyeing & printing, pharmaceutical manufacturing, surface coatings, and polymerization reactions.

In terms of application, Textile Dyeing & Printing is the most dominant segment in the vinyl sulphone ester market. This dominance is due to the extensive use of vinyl sulphone esters as key intermediates in reactive dyes that bond covalently with fibers, particularly cotton and other cellulosic textiles. These esters enable the production of vibrant, wash-fast, and light-resistant colors, making them highly preferred for textile dyeing and printing processes. The booming textile industry in developing economies, coupled with increasing consumer demand for high-quality colored fabrics, further fuels growth in this segment.

Pharmaceutical Manufacturing follows as the second most prominent application. Vinyl sulphone esters are utilized in the synthesis of drug intermediates and active pharmaceutical ingredients (APIs), where their electrophilic nature facilitates specific chemical transformations. Although the volume of consumption in this sector is not as large as in textiles, the high value and precision-driven demand of pharmaceutical applications contribute significantly to the segment’s importance.

The Surface Coatings segment ranks third, with vinyl sulphone esters being used in the formulation of specialty coatings where cross-linking reactions are necessary to improve durability, adhesion, or chemical resistance. Their presence in this segment is more niche, often limited to high-performance coatings in industrial or automotive sectors where customized chemical interactions are required.

Polymerization Reactions constitute the least dominant application segment. In this area, vinyl sulphone esters may act as reactive monomers or co-monomers in specialty polymer synthesis. However, their use is generally limited to research, experimental polymers, or very specific industrial needs, making the segment relatively small in terms of overall market share.

Segmentation Insights by Distribution Channel

On the basis of distribution channel, the global vinyl sulphone ester market is bifurcated into direct sales, online sales, and third-party distribution.

In the vinyl sulphone ester market, Direct Sales is the most dominant distribution channel. This is primarily because vinyl sulphone esters are typically sold in bulk quantities to large industrial buyers—particularly in the textile and chemical sectors—who require consistent quality, technical support, and long-term supply agreements. Direct sales allow manufacturers to build strong relationships with end-users, customize product specifications, and ensure timely delivery, all of which are critical in high-volume, quality-sensitive industries.

Third-party Distribution follows as the second most prominent channel. Distributors and agents often play a crucial role in regions where manufacturers lack a direct sales presence. These third-party entities help expand market reach by offering logistics, warehousing, and customer service capabilities. They are especially important for serving smaller or mid-sized companies that do not purchase in large volumes or need localized support in areas with limited direct access to suppliers.

Online Sales is currently the least dominant distribution channel. While digital platforms are gaining popularity in many chemical markets, the adoption of online sales for vinyl sulphone esters remains relatively low due to the technical and regulatory complexities of selling industrial-grade chemicals online. However, online channels are slowly emerging as a supplementary option for small-volume orders, research purposes, and sample procurement, particularly among academic institutions and small-scale formulators.

Segmentation Insights by Form

On the basis of form, the global vinyl sulphone ester market is bifurcated into powder and liquid.

In the vinyl sulphone ester market, the Powder form holds the most dominant position. This dominance is attributed to the powder form’s superior stability, ease of transportation, longer shelf life, and compatibility with a wide range of dyeing applications—particularly in the textile industry. Powdered vinyl sulphone esters are preferred by dye manufacturers and textile processors because they are easier to store and can be precisely measured and mixed during dye formulation. Additionally, their lower risk of leakage or spillage during handling and shipping makes them more practical for bulk industrial use.

On the other hand, the Liquid form of vinyl sulphone esters is less dominant in the market. Liquids may offer advantages such as quicker dissolution and easier integration into certain chemical processes, making them suitable for specific high-precision applications like pharmaceutical synthesis or specialty chemical reactions. However, they tend to have shorter shelf lives, higher storage costs, and more complex handling requirements due to potential reactivity and packaging concerns. As a result, their adoption is limited compared to the powder form.

Vinyl Sulphone Ester Market: Regional Insights

- Asia Pacific is expected to dominates the global market

The Asia Pacific (APAC) region dominates the vinyl sulphone ester market due to the strong presence of textile and dye industries in countries like China and India. China, being the largest producer and consumer of textiles, significantly drives demand for vinyl sulphone esters as intermediates in the production of reactive dyes. India's expanding textile sector further supports the market growth, and government initiatives are providing additional support for the industry's expansion. The rapid industrialization and urbanization in this region continue to bolster the demand for high-performance dyes, positioning Asia Pacific as the dominant region in this market.

North America holds a significant market share, with the United States being the key contributor. The demand for vinyl sulphone esters in this region is largely driven by the textile industry's need for high-quality dyes and intermediates. Stringent environmental regulations in the U.S. have led to the adoption of sustainable and eco-friendly dyeing processes, further boosting the market. The region's established chemical manufacturing base and focus on innovation in dye technologies help maintain a steady growth rate in North America.

In Europe, countries such as Germany, France, and the United Kingdom play a leading role in the vinyl sulphone ester market. The region is highly focused on sustainability and environmental compliance, which has led to increased demand for eco-friendly dyes. Germany, with its strong textile and automotive industries, is a major consumer of vinyl sulphone esters for dyeing and printing purposes. The EU's policies that promote renewable and bio-based resources further stimulate market growth in this region.

The Middle East and Africa (MEA) region shows moderate growth in the vinyl sulphone ester market, with countries like Saudi Arabia and the UAE witnessing steady industrial development. While the textile industry in these regions is expanding, it does so at a slower pace compared to other regions, making the market smaller. However, ongoing industrialization and increased investment in manufacturing sectors provide gradual growth potential for the market in MEA.

Latin America, particularly Brazil and Colombia, displays a developing market for vinyl sulphone esters. The textile industry in these countries is growing, driven by both domestic and export demand. Although the market share remains relatively small, economic conditions, industrial development, and evolving trade policies are expected to contribute to steady growth in Latin America. However, it remains the least dominant region in comparison to others.

Vinyl Sulphone Ester Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the vinyl sulphone ester market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global vinyl sulphone ester market include:

- Matangi Industries

- EMCO Dyestuff

- BHAGERIA INDUSTRIE

- Nanjing Chem Import and Export

- BHIMANI CHEMICALS

- Henan Xinxiang Weixing Dyestuff Chemical Plant

- Crystal Quinone

The global vinyl sulphone ester market is segmented as follows:

By Product Type

- Vinyl Sulphone Ester A

- Vinyl Sulphone Ester B

- Vinyl Sulphone Ester C

By End-Use Industry

- Textile Industry

- Pharmaceutical Industry

- Chemicals Manufacturing

- Water Treatment Industry

By Application

- Textile Dyeing and Printing

- Pharmaceutical Manufacturing

- Surface Coatings

- Polymerization Reactions

By Distribution Channel

- Direct Sales

- Online Sales

- Third-party Distribution

By Form

- Powder

- Liquid

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Vinyl Sulphone Ester

Request Sample

Vinyl Sulphone Ester