Acute Lymphoblastic Leukemia Market Size, Share, and Trends Analysis Report

CAGR :

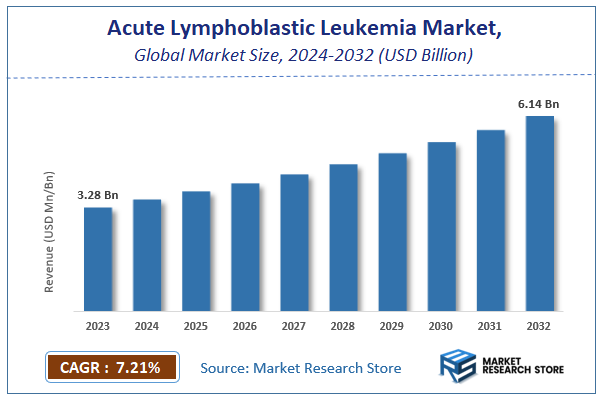

| Market Size 2023 (Base Year) | USD 3.28 Billion |

| Market Size 2032 (Forecast Year) | USD 6.14 Billion |

| CAGR | 7.21% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Acute Lymphoblastic Leukemia Market Insights

According to Market Research Store, the global acute lymphoblastic leukemia market size was valued at around USD 3.28 billion in 2023 and is estimated to reach USD 6.14 billion by 2032, to register a CAGR of approximately 7.21% in terms of revenue during the forecast period 2024-2032.

The acute lymphoblastic leukemia report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Acute Lymphoblastic Leukemia Market: Overview

Acute Lymphoblastic Leukemia is a fast-progressing cancer of the blood and bone marrow that affects the lymphoid cell line responsible for producing lymphocytes, a type of white blood cell. It occurs when the bone marrow produces an excessive number of immature lymphoblasts, which crowd out healthy blood cells and impair the body’s ability to fight infections, carry oxygen, and control bleeding. ALL can affect both children and adults, but it is most common in children aged 2 to 5 years. Symptoms include fatigue, fever, frequent infections, easy bruising or bleeding, bone pain, and swollen lymph nodes. The disease requires urgent treatment, which may include chemotherapy, targeted therapy, radiation therapy, and in some cases, stem cell transplantation.

Key Highlights

- The acute lymphoblastic leukemia market is anticipated to grow at a CAGR of 7.21% during the forecast period.

- The global acute lymphoblastic leukemia market was estimated to be worth approximately USD 3.28 billion in 2023 and is projected to reach a value of USD 6.14 billion by 2032.

- The growth of the acute lymphoblastic leukemia market is being driven by Increasing awareness about early detection, rising healthcare expenditure, and the availability of novel treatment options such as CAR-T cell therapy.

- Based on the type, the pediatrics segment is growing at a high rate and is projected to dominate the market.

- On the basis of therapy type, the chemotherapy segment is projected to swipe the largest market share.

- In terms of drug, the Hyper-CVAD regimen segment is expected to dominate the market.

- Based on the end user, the hospitals & clinics segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Acute Lymphoblastic Leukemia Market: Dynamics

Key Growth Drivers:

- Rising Incidence of ALL Worldwide: Increasing prevalence of acute lymphoblastic leukemia, especially among children and older adults, is driving demand for effective therapies.

- Advancements in Targeted and Immunotherapies: New treatments such as CAR-T cell therapy, monoclonal antibodies, and tyrosine kinase inhibitors are improving patient survival rates.

- Government and Nonprofit Funding for Cancer Research: Financial support for leukemia research is accelerating drug development and expanding treatment options.

- Improved Diagnostic Capabilities: Advances in genetic and molecular testing are enabling earlier detection and more personalized treatment plans.

Restraints:

- High Cost of Advanced Therapies: Innovative treatments like CAR-T therapy are expensive, limiting patient access, especially in low- and middle-income countries.

- Severe Side Effects and Toxicities: Chemotherapy, radiation, and immunotherapies can cause significant adverse effects, affecting treatment adherence.

- Limited Availability of Specialized Care in Developing Regions: Lack of advanced oncology facilities hampers access to effective treatment in certain parts of the world.

Opportunities:

- Expansion of Precision Medicine Approaches: Tailoring treatments based on genetic profiling of patients can improve outcomes and reduce side effects.

- Growth in Emerging Markets: Increasing healthcare investments in Asia-Pacific, Latin America, and the Middle East open new avenues for acute lymphoblastic leukemia therapeutics.

- Development of Combination Therapies: Research on combining targeted drugs, immunotherapy, and chemotherapy offers potential for improved efficacy.

Challenges:

- High Clinical Trial Failure Rate: Many experimental drugs fail during late-stage trials due to safety or efficacy concerns, slowing new product launches.

- Rapid Disease Progression: The aggressive nature of acute lymphoblastic leukemia leaves limited time for diagnosis and therapeutic intervention.

- Stringent Regulatory Approval Processes: Complex approval requirements for oncology drugs can delay market entry for novel therapies.

Acute Lymphoblastic Leukemia Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Acute Lymphoblastic Leukemia Market |

| Market Size in 2023 | USD 3.28 Billion |

| Market Forecast in 2032 | USD 6.14 Billion |

| Growth Rate | CAGR of 7.21% |

| Number of Pages | 160 |

| Key Companies Covered | Celegene Corporation, Erytech Pharma, Genmab A/S, Novartis AG, Sanofi SA, Bristol Myer Squibb Company, Eisai Co Ltd, Hoffmann-La Roche Ltd, GlaxoSmithKline PLC, and Pfizer Inc. among others |

| Segments Covered | By Type, By Therapy Type, By Drug, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Acute Lymphoblastic Leukemia Market: Segmentation Insights

The global acute lymphoblastic leukemia market is divided by type, therapy type, drug, end user, and region.

Based on type, the global acute lymphoblastic leukemia market is divided into pediatrics and adults. Pediatrics is the most dominant segment, as ALL is the most common cancer in children, particularly between the ages of 2 and 5 years. Pediatric patients generally respond better to treatment compared to adults, with higher remission and survival rates due to fewer comorbidities and greater tolerance to intensive chemotherapy. The strong focus on pediatric oncology research, specialized treatment protocols, and access to advanced therapies such as targeted drugs and immunotherapies further contribute to the segment’s leadership. Adults represent the smaller segment but face more complex treatment challenges, as adult ALL often presents with higher genetic risk factors, lower tolerance to aggressive chemotherapy, and a greater likelihood of relapse. Survival rates in adults are generally lower compared to pediatric cases, which has driven the need for more targeted and novel therapies. Ongoing advancements in immunotherapies, precision medicine, and stem cell transplantation are gradually improving treatment outcomes for this segment.

On the basis of therapy type, the global acute lymphoblastic leukemia market is bifurcated into chemotherapy, targeted therapy, radiation therapy, and stem cell transplantation. Chemotherapy is the most dominant therapy type, serving as the primary first-line treatment for both pediatric and adult patients. It involves multi-phase regimens induction, consolidation, and maintenance to eliminate leukemia cells and prevent relapse. The long-standing clinical success, established treatment protocols, and broad accessibility of chemotherapy ensure its continued leadership, despite the emergence of newer treatment options. Targeted therapy holds the second-largest share, driven by the increasing use of drugs designed to act on specific genetic mutations or molecular markers, such as tyrosine kinase inhibitors for Philadelphia chromosome–positive ALL. These therapies offer improved precision, reduced side effects, and better outcomes for certain patient subgroups, making them a rapidly expanding part of the treatment landscape.

Based on drug, the global acute lymphoblastic leukemia market is divided into hyper-cvad regimen, linker regimen, nucleoside metabolic inhibitors, targeted drugs & immunotherapy, calgb 8811 regimen, oncaspar, and others. Hyper-CVAD regimen is the most dominant drug segment, widely used as a standard chemotherapy protocol for adult ALL patients. It involves alternating cycles of high-dose cyclophosphamide, vincristine, doxorubicin, and dexamethasone with methotrexate and cytarabine, offering proven efficacy in inducing remission. Its established clinical success and adaptability to combination with targeted agents help maintain its leading position. Targeted drugs & immunotherapy hold the second-largest share, driven by the growing use of agents such as blinatumomab, inotuzumab ozogamicin, and tyrosine kinase inhibitors for Philadelphia chromosome–positive ALL. These treatments provide precision targeting of leukemia cells with improved outcomes, particularly for relapsed or refractory patients, and represent one of the fastest-growing areas in the market.

On the basis of end user, the global acute lymphoblastic leukemia market is bifurcated into hospitals & clinics, cancer care centers, and research & academic institutes. Hospitals & clinics are the most dominant end-user segment, as they serve as the primary treatment centers for diagnosis, chemotherapy administration, targeted therapy infusions, and supportive care. Hospitals offer comprehensive oncology departments, advanced diagnostic tools, and access to multidisciplinary teams, making them the central hub for managing ALL cases from initial treatment to follow-up care. Cancer care centers hold the second-largest share, specializing in oncology-focused treatment and offering advanced therapies such as immunotherapy, stem cell transplantation, and clinical trial participation. These centers often provide highly personalized care, rapid access to specialized oncologists, and innovative treatment protocols, making them a preferred choice for complex or relapsed cases.

Acute Lymphoblastic Leukemia Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the Acute Lymphoblastic Leukemia therapeutics market, driven by advanced healthcare infrastructure, high investment in research and development, and early adoption of innovative therapies such as CAR‑T cell treatments and targeted drugs. The region’s strong insurance coverage and reimbursement policies ensure patient access to cutting-edge treatments, while a high level of clinical trial activity further strengthens its leadership position.

Europe holds the second-largest share, supported by well-established public healthcare systems, favorable regulatory frameworks, and strong adoption of precision medicine approaches. Countries like Germany, the UK, and France lead the region in implementing advanced ALL therapies, with growing emphasis on clinical trials and collaborative research to improve patient outcomes.

Asia Pacific ranks third but is the fastest-growing region, driven by rising incidence rates, improving healthcare infrastructure, and increasing awareness about leukemia treatments. Expanding access to advanced therapies in countries like China, India, Japan, and Australia is contributing to rapid market growth, along with government initiatives aimed at strengthening cancer care services.

Latin America accounts for a smaller share, with growth primarily concentrated in Brazil, Mexico, and Argentina. Rising healthcare investments and expanding oncology treatment facilities are boosting adoption, but economic constraints and limited access to high-cost therapies continue to hinder broader market penetration.

Middle East and Africa represent the smallest share of the market, with demand centered in urbanized and high-income areas of the Gulf countries and select African nations. Gradual improvements in healthcare infrastructure and increasing availability of advanced treatments are driving growth, though overall market development remains in the early stages compared to other regions.

Acute Lymphoblastic Leukemia Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the acute lymphoblastic leukemia market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global acute lymphoblastic leukemia market include:

- Celegene Corporation

- Erytech Pharma

- Genmab A/S

- Novartis AG

- Sanofi SA

- Bristol Myer Squibb Company

- Eisai Co Ltd

- Hoffmann-La Roche Ltd

- GlaxoSmithKline PLC

- Pfizer Inc.

The global acute lymphoblastic leukemia market is segmented as follows:

By Type

- Pediatrics

- Adults

By Therapy Type

- Chemotherapy

- Targeted Therapy

- Radiation Therapy

- Stem Cell Transplantation

By Drug

- Hyper-CVAD Regimen

- Linker Regimen

- Nucleoside Metabolic Inhibitors

- Targeted Drugs & Immunotherapy

- CALGB 8811 Regimen

- Oncaspar

- Others

By End User

- Hospitals & Clinics

- Cancer Care Centers

- Research & Academic Institutes

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1 Executive Summary

- 1.1. Introduction of Acute Lymphoblastic Leukemia

- 1.2. Global Acute Lymphoblastic Leukemia Market, 2019 & 2026 (USD Million)

- 1.3. Global Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 1.4. Global Acute Lymphoblastic Leukemia Market Absulute Revenue Opportunity, 2016 – 2026 (USD Million)

- 1.5. Global Acute Lymphoblastic Leukemia Market Incremental Revenue Opportunity, 2020 – 2026 (USD Million)

- Chapter 2 Acute Lymphoblastic Leukemia Market – Type Analysis

- 2.1. Global Acute Lymphoblastic Leukemia Market – Type Overview

- 2.2. Global Acute Lymphoblastic Leukemia Market Share, by Type, 2019 & 2026 (USD Million)

- 2.3. Pediatrics

- 2.3.1. Global Pediatrics Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 2.4. Adults

- 2.4.1. Global Adults Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- Chapter 3 Acute Lymphoblastic Leukemia Market – Therapy Type Analysis

- 3.1. Global Acute Lymphoblastic Leukemia Market – Therapy Type Overview

- 3.2. Global Acute Lymphoblastic Leukemia Market Share, by Therapy Type, 2019 & 2026 (USD Million)

- 3.3. Chemotherapy

- 3.3.1. Global Chemotherapy Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 3.4. Targeted Therapy

- 3.4.1. Global Targeted Therapy Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 3.5. Radiation Therapy

- 3.5.1. Global Radiation Therapy Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 3.6. Stem Cell Transplantation

- 3.6.1. Global Stem Cell Transplantation Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- Chapter 4 Acute Lymphoblastic Leukemia Market – Drug Analysis

- 4.1. Global Acute Lymphoblastic Leukemia Market – Drug Overview

- 4.2. Global Acute Lymphoblastic Leukemia Market Share, by Drug, 2019 & 2026 (USD Million)

- 4.3. Hyper-CVAD Regimen

- 4.3.1. Global Hyper-CVAD Regimen Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.4. Linker Regimen

- 4.4.1. Global Linker Regimen Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.5. Nucleoside Metabulic Inhibitors

- 4.5.1. Global Nucleoside Metabulic Inhibitors Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.6. Targeted Drugs & Immunotherapy

- 4.6.1. Global Targeted Drugs & Immunotherapy Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.7. CALGB 8811 Regimen

- 4.7.1. Global CALGB 8811 Regimen Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.8. Oncaspar

- 4.8.1. Global Oncaspar Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 4.9. Others

- 4.9.1. Global Others Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- Chapter 5 Acute Lymphoblastic Leukemia Market – Regional Analysis

- 5.1. Global Acute Lymphoblastic Leukemia Market Regional Overview

- 5.2. Global Acute Lymphoblastic Leukemia Market Share, by Region, 2019 & 2026 (USD Million)

- 5.3. North America

- 5.3.1. North America Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.3.1.1. North America Acute Lymphoblastic Leukemia Market, by Country, 2016 - 2026 (USD Million)

- 5.3.2. North America Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026

- 5.3.2.1. North America Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026 (USD Million)

- 5.3.3. North America Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026

- 5.3.3.1. North America Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026 (USD Million)

- 5.3.4. North America Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026

- 5.3.4.1. North America Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026 (USD Million)

- 5.3.5. U.S.

- 5.3.5.1. U.S. Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.3.6. Canada

- 5.3.6.1. Canada Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.3.1. North America Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4. Europe

- 5.4.1. Europe Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.1.1. Europe Acute Lymphoblastic Leukemia Market, by Country, 2016 - 2026 (USD Million)

- 5.4.2. Europe Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026

- 5.4.2.1. Europe Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026 (USD Million)

- 5.4.3. Europe Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026

- 5.4.3.1. Europe Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026 (USD Million)

- 5.4.4. Europe Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026

- 5.4.4.1. Europe Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026 (USD Million)

- 5.4.5. Germany

- 5.4.5.1. Germany Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.6. France

- 5.4.6.1. France Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.7. U.K.

- 5.4.7.1. U.K. Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.8. Italy

- 5.4.8.1. Italy Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.9. Spain

- 5.4.9.1. Spain Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.10. Rest of Europe

- 5.4.10.1. Rest of Europe Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.4.1. Europe Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5. Asia Pacific

- 5.5.1. Asia Pacific Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.1.1. Asia Pacific Acute Lymphoblastic Leukemia Market, by Country, 2016 - 2026 (USD Million)

- 5.5.2. Asia Pacific Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026

- 5.5.2.1. Asia Pacific Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026 (USD Million)

- 5.5.3. Asia Pacific Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026

- 5.5.3.1. Asia Pacific Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026 (USD Million)

- 5.5.4. Asia Pacific Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026

- 5.5.4.1. Asia Pacific Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026 (USD Million)

- 5.5.5. China

- 5.5.5.1. China Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.6. Japan

- 5.5.6.1. Japan Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.7. India

- 5.5.7.1. India Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.8. South Korea

- 5.5.8.1. South Korea Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.9. South-East Asia

- 5.5.9.1. South-East Asia Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.10. Rest of Asia Pacific

- 5.5.10.1. Rest of Asia Pacific Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.5.1. Asia Pacific Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.6. Latin America

- 5.6.1. Latin America Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.6.1.1. Latin America Acute Lymphoblastic Leukemia Market, by Country, 2016 - 2026 (USD Million)

- 5.6.2. Latin America Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026

- 5.6.2.1. Latin America Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026 (USD Million)

- 5.6.3. Latin America Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026

- 5.6.3.1. Latin America Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026 (USD Million)

- 5.6.4. Latin America Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026

- 5.6.4.1. Latin America Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026 (USD Million)

- 5.6.5. Brazil

- 5.6.5.1. Brazil Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.6.6. Mexico

- 5.6.6.1. Mexico Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.6.7. Rest of Latin America

- 5.6.7.1. Rest of Latin America Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.6.1. Latin America Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.7. The Middle-East and Africa

- 5.7.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.7.1.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Country, 2016 - 2026 (USD Million)

- 5.7.2. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026

- 5.7.2.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Type, 2016 – 2026 (USD Million)

- 5.7.3. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026

- 5.7.3.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Therapy Type, 2016 – 2026 (USD Million)

- 5.7.4. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026

- 5.7.4.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, by Drug, 2016 – 2026 (USD Million)

- 5.7.5. GCC Countries

- 5.7.5.1. GCC Countries Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.7.6. South Africa

- 5.7.6.1. South Africa Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.7.7. Rest of Middle-East Africa

- 5.7.7.1. Rest of Middle-East Africa Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- 5.7.1. The Middle-East and Africa Acute Lymphoblastic Leukemia Market, 2016 – 2026 (USD Million)

- Chapter 6 Acute Lymphoblastic Leukemia Market – Competitive Landscape

- 6.1. Competitor Market Share – Revenue

- 6.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players

- 6.3. Strategic Developments

- 6.3.1. Acquisitions and Mergers

- 6.3.2. New Products

- 6.3.3. Research & Development Activities

- Chapter 7 Company Profiles

- 7.1. Bristul Myer Squibb Company

- 7.1.1. Company Overview

- 7.1.2. Product/Service Portfulio

- 7.1.3. Bristul Myer Squibb Company Sales, Revenue, and Gross Margin

- 7.1.4. Bristul Myer Squibb Company Revenue and Growth Rate

- 7.1.5. Bristul Myer Squibb Company Market Share

- 7.1.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.2. Celegene Corporation

- 7.2.1. Company Overview

- 7.2.2. Product/Service Portfulio

- 7.2.3. Celegene Corporation Sales, Revenue, and Gross Margin

- 7.2.4. Celegene Corporation Revenue and Growth Rate

- 7.2.5. Celegene Corporation Market Share

- 7.2.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.3. Eisai Co Ltd

- 7.3.1. Company Overview

- 7.3.2. Product/Service Portfulio

- 7.3.3. Eisai Co Ltd Sales, Revenue, and Gross Margin

- 7.3.4. Eisai Co Ltd Revenue and Growth Rate

- 7.3.5. Eisai Co Ltd Market Share

- 7.3.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.4. Erytech Pharma

- 7.4.1. Company Overview

- 7.4.2. Product/Service Portfulio

- 7.4.3. Erytech Pharma Sales, Revenue, and Gross Margin

- 7.4.4. Erytech Pharma Revenue and Growth Rate

- 7.4.5. Erytech Pharma Market Share

- 7.4.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.5. Hoffmann-La Roche Ltd

- 7.5.1. Company Overview

- 7.5.2. Product/Service Portfulio

- 7.5.3. Hoffmann-La Roche Ltd Sales, Revenue, and Gross Margin

- 7.5.4. Hoffmann-La Roche Ltd Revenue and Growth Rate

- 7.5.5. Hoffmann-La Roche Ltd Market Share

- 7.5.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.6. Genmab A/S

- 7.6.1. Company Overview

- 7.6.2. Product/Service Portfulio

- 7.6.3. Genmab A/S Sales, Revenue, and Gross Margin

- 7.6.4. Genmab A/S Revenue and Growth Rate

- 7.6.5. Genmab A/S Market Share

- 7.6.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.7. GlaxoSmithKline PLC

- 7.7.1. Company Overview

- 7.7.2. Product/Service Portfulio

- 7.7.3. GlaxoSmithKline PLC Sales, Revenue, and Gross Margin

- 7.7.4. GlaxoSmithKline PLC Revenue and Growth Rate

- 7.7.5. GlaxoSmithKline PLC Market Share

- 7.7.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.8. Novartis AG

- 7.8.1. Company Overview

- 7.8.2. Product/Service Portfulio

- 7.8.3. Novartis AG Sales, Revenue, and Gross Margin

- 7.8.4. Novartis AG Revenue and Growth Rate

- 7.8.5. Novartis AG Market Share

- 7.8.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.9. Pfizer Inc.

- 7.9.1. Company Overview

- 7.9.2. Product/Service Portfulio

- 7.9.3. Pfizer Inc. Sales, Revenue, and Gross Margin

- 7.9.4. Pfizer Inc. Revenue and Growth Rate

- 7.9.5. Pfizer Inc. Market Share

- 7.9.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.10. Sanofi SA

- 7.10.1. Company Overview

- 7.10.2. Product/Service Portfulio

- 7.10.3. Sanofi SA Sales, Revenue, and Gross Margin

- 7.10.4. Sanofi SA Revenue and Growth Rate

- 7.10.5. Sanofi SA Market Share

- 7.10.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 7.1. Bristul Myer Squibb Company

- Chapter 8 Acute Lymphoblastic Leukemia — Industry Analysis

- 8.1. Introduction and Taxonomy

- 8.2. Acute Lymphoblastic Leukemia Market – Key Trends

- 8.2.1. Market Drivers

- 8.2.2. Market Restraints

- 8.2.3. Market Opportunities

- 8.3. Value Chain Analysis

- 8.4. Key Mandates and Regulations

- 8.5. Technulogy Roadmap and Timeline

- 8.6. Acute Lymphoblastic Leukemia Market – Attractiveness Analysis

- 8.6.1. By Type

- 8.6.2. By Therapy Type

- 8.6.3. By Drug

- 8.6.4. By Region

- Chapter 9 Industrial Chain, Sourcing Strategy, and Downstream Buyers

- 9.1. Acute Lymphoblastic Leukemia Industrial Chain Analysis

- 9.2. Downstream Buyers

- 9.3. Distributors/Traders List

- Chapter 10 Marketing Strategy Analysis

- 10.1. Marketing Channel

- 10.2. Direct Marketing

- 10.3. Indirect Marketing

- 10.4. Marketing Channel Development Trends

- 10.5. Economic/Pulitical Environmental Change

- Chapter 11 Report Conclusion & Key Insights

- 11.1. Key Insights from Primary Interviews & Surveys Respondents

- 11.2. Key Takeaways from Analysts, Consultants, and Industry Leaders

- Chapter 12 Research Approach & Methodulogy

- 12.1. Report Description

- 12.2. Research Scope

- 12.3. Research Methodulogy

- 12.3.1. Secondary Research

- 12.3.2. Primary Research

- 12.3.3. Statistical Models

- 12.3.3.1. Company Share Analysis Model

- 12.3.3.2. Revenue Based Modeling

- 12.3.4. Research Limitations

Inquiry For Buying

Acute Lymphoblastic Leukemia

Request Sample

Acute Lymphoblastic Leukemia