Aerospace & Defense Fluid Conveyance Systems Market Size, Share, and Trends Analysis Report

CAGR :

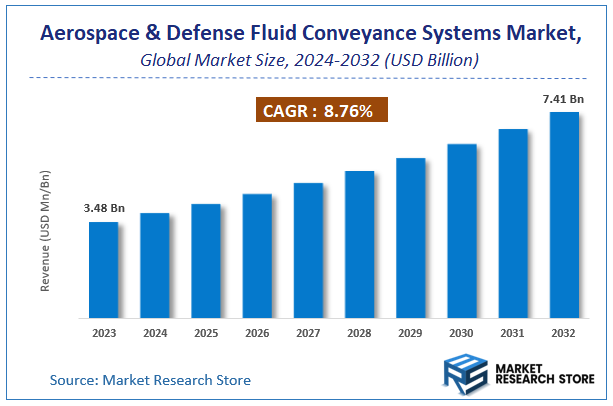

| Market Size 2023 (Base Year) | USD 3.48 Billion |

| Market Size 2032 (Forecast Year) | USD 7.41 Billion |

| CAGR | 8.76% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Aerospace & Defense Fluid Conveyance Systems Market Insights

According to Market Research Store, the global aerospace & defense fluid conveyance systems market size was valued at around USD 3.48 billion in 2023 and is estimated to reach USD 7.41 billion by 2032, to register a CAGR of approximately 8.76% in terms of revenue during the forecast period 2024-2032.

The aerospace & defense fluid conveyance systems report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Aerospace & Defense Fluid Conveyance Systems Market: Overview

Aerospace & Defense Fluid Conveyance Systems are specialized assemblies used to transport fluids such as fuel, hydraulic fluids, lubricants, and air within aircraft and defense vehicles. These systems include components like hoses, tubes, ducts, fittings, and connectors designed to operate under high pressure, temperature, and vibration conditions. Their primary role is to ensure efficient, safe, and reliable fluid transfer throughout various systems such as engines, fuel tanks, braking systems, and environmental control units in both commercial aircraft and military platforms.

Key Highlights

- The aerospace & defense fluid conveyance systems market is anticipated to grow at a CAGR of 8.76% during the forecast period.

- The global aerospace & defense fluid conveyance systems market was estimated to be worth approximately USD 3.48 billion in 2023 and is projected to reach a value of USD 7.41 billion by 2032.

- The growth of the aerospace & defense fluid conveyance systems market is being driven by the increasing production of commercial aircraft, rising defense expenditures, and ongoing technological advancements in fluid handling components.

- Based on the type, the hoses segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the commercial aviation segment is projected to swipe the largest market share.

- In terms of material type, the composite materials segment is expected to dominate the market.

- Based on the pressure rating, the medium pressure systems (1,000 to 5,000 psi) segment is expected to dominate the market.

- In terms of end-user, the aerospace sector segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Aerospace & Defense Fluid Conveyance Systems Market: Dynamics

Key Growth Drivers:

- Increase in Aircraft Production and Fleet Modernization: The rising demand for new commercial aircraft and the modernization of aging military fleets are boosting the need for advanced fluid conveyance systems to support next-generation performance and efficiency.

- Technological Advancements in Materials and Design: The adoption of lightweight, high-strength materials such as composites and titanium in fluid systems enhances fuel efficiency and aircraft performance, driving innovation and demand in the market.

- Rising Defense Expenditure Worldwide: Increased global defense budgets, especially in the U.S., China, and India, are fueling procurement of advanced military aircraft, helicopters, and UAVs, directly contributing to market expansion.

Restraints:

- High Cost and Complexity of System Integration: The precision engineering and stringent certification requirements involved in fluid conveyance systems increase production and integration costs, making it challenging for smaller players to compete.

- Dependence on the Aerospace Production Cycle: The market is closely tied to aircraft production rates. Any delays, cancellations, or downturns in the aerospace sector can directly impact fluid system demand.

Opportunities:

- Emerging Markets and Indigenous Aerospace Programs: Countries like China, India, and Brazil are developing their own aircraft and defense programs, creating new opportunities for fluid conveyance system suppliers to partner or expand locally.

- Growth in MRO and Aftermarket Services: As global fleets expand and age, the need for maintenance, repair, and replacement of fluid systems is rising, offering recurring revenue opportunities for aftermarket service providers.

Challenges:

- Stringent Regulatory and Quality Standards: Compliance with aerospace safety, environmental, and performance regulations requires extensive testing, documentation, and certification, posing entry barriers and slowing down time to market.

- Supply Chain Disruptions and Material Shortages: Global disruptions in raw material availability and specialized components can delay production schedules and impact the timely delivery of fluid systems to OEMs and defense agencies.

Aerospace & Defense Fluid Conveyance Systems Market: Report Scope

This report thoroughly analyzes the Aerospace & Defense Fluid Conveyance Systems Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Aerospace & Defense Fluid Conveyance Systems Market |

| Market Size in 2023 | USD 3.48 Billion |

| Market Forecast in 2032 | USD 7.41 Billion |

| Growth Rate | CAGR of 8.76% |

| Number of Pages | 165 |

| Key Companies Covered | Arrowhead Products Corporation, AIM Aerospace, Encore Group, Eaton Corporation, Flexfab Horizons International, Exotic Metals Forming LLC, ITT Corporation, GKN plc, Parker Hannifin Corporation, Meggitt PLC, Senior plc, PFW Aerospace AG, Triumph Group Inc., Stelia Aerospace, United Flexible, Unison Industries, Zodiac Aerospace, and among others |

| Segments Covered | By Type, By Application, By Material Type, By Pressure Rating, By End-user, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Aerospace & Defense Fluid Conveyance Systems Market: Segmentation Insights

The global aerospace & defense fluid conveyance systems market is divided by type, application, material type, pressure rating, end-user, and region.

Based on type, the global aerospace & defense fluid conveyance systems market is divided into hoses, pipes, fittings, valves, connectors, fluid transfer assemblies. Hoses represent the most dominant segment, owing to their flexibility, lightweight construction, and critical role in managing dynamic fluid transfer across moving components. Hoses are widely used in both commercial and military aircraft for hydraulic, fuel, lubrication, and cooling systems. Their adaptability in complex configurations and ability to withstand extreme temperatures and pressures make them indispensable in high-performance aerospace systems.

On the basis of application, the global aerospace & defense fluid conveyance systems market is bifurcated into commercial aviation, military aviation, spacecraft, ground defense vehicles, naval defense ships, and unmanned aerial vehicles (UAVs). Commercial aviation is the most dominant application segment due to the large global fleet of commercial aircraft and the continuous growth in air travel. Fluid conveyance systems are essential for managing fuel, hydraulics, and environmental controls in commercial jets. As airlines prioritize fuel efficiency, reliability, and reduced maintenance, there is high demand for advanced and lightweight fluid systems, especially in newer aircraft models.

Based on material type, the global aerospace & defense fluid conveyance systems market is divided into rubber, composite materials, metals, thermoplastics, and elastomers. Composite materials are the most dominant segment due to their lightweight, high-strength, and corrosion-resistant properties. They are increasingly favored in both commercial and military aircraft to reduce overall weight, enhance fuel efficiency, and meet performance requirements. Composites are widely used in hoses, ducts, and fluid transfer assemblies, especially where flexibility and durability under extreme conditions are essential.

In terms of of pressure rating, the global aerospace & defense fluid conveyance systems market is bifurcated into low pressure (up to 1,000 psi), medium pressure (1,000 to 5,000 psi), and high pressure (above 5,000 psi). Medium pressure systems (1,000 to 5,000 psi) are the most dominant segment, as they are widely used in critical aircraft and defense vehicle functions such as fuel systems, hydraulics, and environmental control systems. These systems offer a balance between performance and cost, making them suitable for most commercial and military aviation applications, including wing actuators, landing gear, and flight control surfaces.

By end-user, the global aerospace & defense fluid conveyance systems market is bifurcated into defense sector, aerospace sector, commercial aircraft manufacturers, space exploration organizations, and aerospace component suppliers. The aerospace sector is the most dominant end-user, driven by strong demand from both commercial aviation and general aviation segments. The need for advanced, lightweight, and high-efficiency fluid systems to support increasing aircraft production, fleet expansion, and modernization programs positions this sector at the forefront. Manufacturers are focusing on optimizing fluid management for fuel efficiency and performance, particularly in next-generation aircraft.

Aerospace & Defense Fluid Conveyance Systems Market: Regional Insights

- North America is expected to dominates the global market

North America leads the global Aerospace & Defense Fluid Conveyance Systems market, primarily driven by the strong presence of major aircraft OEMs, defense contractors, and MRO (maintenance, repair, and overhaul) service providers in the United States. The region benefits from consistent investments in military modernization programs, the development of next-generation fighter jets, and high demand for commercial aircraft. Moreover, the U.S. Department of Defense’s continued focus on upgrading air fleet capabilities ensures steady demand for advanced and reliable fluid conveyance systems. The mature aerospace manufacturing ecosystem and robust supply chain further solidify North America’s dominant position in the market.

Europe follows as the second-largest regional market, supported by the presence of prominent aircraft manufacturers and defense organizations across countries like France, Germany, and the UK. The region shows strong demand for advanced fluid systems, especially in military aircraft, helicopters, and space applications. Programs such as Eurofighter Typhoon, Airbus A350, and multinational defense collaborations are key drivers. Additionally, increasing focus on fuel-efficient aircraft and the adoption of lightweight composite materials in system design support market growth across Europe.

Asia Pacific is witnessing rapid expansion in the Aerospace & Defense Fluid Conveyance Systems market, fueled by rising defense budgets, growing commercial aviation traffic, and the emergence of indigenous aircraft manufacturing programs in countries such as China, India, and Japan. The region is increasingly investing in both civil and military aviation infrastructure, including domestic aircraft development initiatives like China’s COMAC and India’s HAL Tejas. As regional airlines expand fleets and governments prioritize defense modernization, demand for advanced fluid transfer systems is growing steadily.

Middle East and Africa (MEA) has a smaller but steadily developing market, primarily driven by defense aircraft procurement and investments in aviation infrastructure in countries like Saudi Arabia, the UAE, and South Africa. The Middle East’s strategic focus on enhancing military capabilities and developing its domestic aerospace industry contributes to rising adoption of modern fluid conveyance technologies. However, limited manufacturing capabilities and reliance on imports constrain faster market growth compared to more industrialized regions.

Latin America represents the smallest share in the global market, with growth largely concentrated in Brazil and Mexico. Brazil’s Embraer plays a pivotal role in the region’s aerospace sector, contributing to demand for fluid systems in commercial and military aircraft. While overall defense spending and aerospace production in the region remain modest, economic development and gradual fleet upgrades are expected to create long-term opportunities for fluid conveyance system providers. Nonetheless, political and economic instability continue to pose challenges to sustained growth.

Aerospace & Defense Fluid Conveyance Systems Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the aerospace & defense fluid conveyance systems market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global aerospace & defense fluid conveyance systems market include:

- Arrowhead Products Corporation

- AIM Aerospace

- Encore Group

- Eaton Corporation

- Flexfab Horizons International

- Exotic Metals Forming LLC

- ITT Corporation

- GKN plc

- Parker Hannifin Corporation

- Meggitt PLC

- Senior plc

- PFW Aerospace AG

- Triumph Group Inc.

- Stelia Aerospace

- United Flexible

- Unison Industries

- Zodiac Aerospace

The global aerospace & defense fluid conveyance systems market is segmented as follows:

By Type

- Hoses

- Pipes

- Fittings

- Valves

- Connectors

- Fluid Transfer Assemblies

By Application

- Commercial Aviation

- Military Aviation

- Spacecraft

- Ground Defense Vehicles

- Naval Defense Ships

- Unmanned Aerial Vehicles (UAVs)

By Material Type

- Rubber

- Composite Materials

- Metals

- Thermoplastics

- Elastomers

By Pressure Rating

- Low Pressure (up to 1,000 psi)

- Medium Pressure (1,000 to 5,000 psi)

- High Pressure (above 5,000 psi)

By End-user

- Defense Sector

- Aerospace Sector

- Commercial Aircraft Manufacturers

- Space Exploration Organizations

- Aerospace Component Suppliers

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

What will be the value of the aerospace & defense fluid conveyance systems market during 2024- 2032?

Table Of Content

- Chapter 1 Executive Summary

- 1.1. Introduction of Aerospace & Defense Fluid Conveyance Systems

- 1.2. Global Aerospace & Defense Fluid Conveyance Systems Market, 2019 & 2026 (USD Million)

- 1.3. Global Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 1.4. Global Aerospace & Defense Fluid Conveyance Systems Market Absulute Revenue Opportunity, 2016 – 2026 (USD Million)

- 1.5. Global Aerospace & Defense Fluid Conveyance Systems Market Incremental Revenue Opportunity, 2020 – 2026 (USD Million)

- Chapter 2 Aerospace & Defense Fluid Conveyance Systems Market – Aircraft Analysis

- 2.1. Global Aerospace & Defense Fluid Conveyance Systems Market – Aircraft Overview

- 2.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Aircraft, 2019 & 2026 (USD Million)

- 2.3. Commercial Aircraft

- 2.3.1. Global Commercial Aircraft Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 2.4. Regional Jet

- 2.4.1. Global Regional Jet Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 2.5. Business Jet

- 2.5.1. Global Business Jet Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 2.6. Military Aircraft

- 2.6.1. Global Military Aircraft Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 2.7. Helicopter

- 2.7.1. Global Helicopter Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 3 Aerospace & Defense Fluid Conveyance Systems Market – Fluid Analysis

- 3.1. Global Aerospace & Defense Fluid Conveyance Systems Market – Fluid Overview

- 3.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Fluid, 2019 & 2026 (USD Million)

- 3.3. Fuel

- 3.3.1. Global Fuel Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 3.4. Pneumatic

- 3.4.1. Global Pneumatic Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 3.5. Hydraulic

- 3.5.1. Global Hydraulic Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 4 Aerospace & Defense Fluid Conveyance Systems Market – Component Analysis

- 4.1. Global Aerospace & Defense Fluid Conveyance Systems Market – Component Overview

- 4.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Component, 2019 & 2026 (USD Million)

- 4.3. Hoses

- 4.3.1. Global Hoses Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 4.4. Couplings

- 4.4.1. Global Couplings Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 4.5. Ducts

- 4.5.1. Global Ducts Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 4.6. Seals

- 4.6.1. Global Seals Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 5 Aerospace & Defense Fluid Conveyance Systems Market – Distribution Channel Analysis

- 5.1. Global Aerospace & Defense Fluid Conveyance Systems Market – Distribution Channel Overview

- 5.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Distribution Channel, 2019 & 2026 (USD Million)

- 5.3. OEM

- 5.3.1. Global OEM Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 5.4. Aftermarket

- 5.4.1. Global Aftermarket Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 6 Aerospace & Defense Fluid Conveyance Systems Market – Application Analysis

- 6.1. Global Aerospace & Defense Fluid Conveyance Systems Market – Application Overview

- 6.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Application, 2019 & 2026 (USD Million)

- 6.3. Engine

- 6.3.1. Global Engine Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 6.4. Airframe

- 6.4.1. Global Airframe Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 7 Aerospace & Defense Fluid Conveyance Systems Market – Regional Analysis

- 7.1. Global Aerospace & Defense Fluid Conveyance Systems Market Regional Overview

- 7.2. Global Aerospace & Defense Fluid Conveyance Systems Market Share, by Region, 2019 & 2026 (USD Million)

- 7.3. North America

- 7.3.1. North America Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.3.1.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Country, 2016 - 2026 (USD Million)

- 7.3.2. North America Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026

- 7.3.2.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026 (USD Million)

- 7.3.3. North America Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026

- 7.3.3.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026 (USD Million)

- 7.3.4. North America Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026

- 7.3.4.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026 (USD Million)

- 7.3.5. North America Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026

- 7.3.5.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026 (USD Million)

- 7.3.6. North America Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026

- 7.3.6.1. North America Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026 (USD Million)

- 7.3.7. U.S.

- 7.3.7.1. U.S. Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.3.8. Canada

- 7.3.8.1. Canada Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.3.1. North America Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4. Europe

- 7.4.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.1.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Country, 2016 - 2026 (USD Million)

- 7.4.2. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026

- 7.4.2.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026 (USD Million)

- 7.4.3. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026

- 7.4.3.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026 (USD Million)

- 7.4.4. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026

- 7.4.4.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026 (USD Million)

- 7.4.5. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026

- 7.4.5.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026 (USD Million)

- 7.4.6. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026

- 7.4.6.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026 (USD Million)

- 7.4.7. Germany

- 7.4.7.1. Germany Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.8. France

- 7.4.8.1. France Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.9. U.K.

- 7.4.9.1. U.K. Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.10. Italy

- 7.4.10.1. Italy Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.11. Spain

- 7.4.11.1. Spain Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.12. Rest of Europe

- 7.4.12.1. Rest of Europe Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.4.1. Europe Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5. Asia Pacific

- 7.5.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.1.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Country, 2016 - 2026 (USD Million)

- 7.5.2. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026

- 7.5.2.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026 (USD Million)

- 7.5.3. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026

- 7.5.3.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026 (USD Million)

- 7.5.4. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026

- 7.5.4.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026 (USD Million)

- 7.5.5. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026

- 7.5.5.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026 (USD Million)

- 7.5.6. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026

- 7.5.6.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026 (USD Million)

- 7.5.7. China

- 7.5.7.1. China Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.8. Japan

- 7.5.8.1. Japan Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.9. India

- 7.5.9.1. India Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.10. South Korea

- 7.5.10.1. South Korea Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.11. South-East Asia

- 7.5.11.1. South-East Asia Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.12. Rest of Asia Pacific

- 7.5.12.1. Rest of Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.5.1. Asia Pacific Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.6. Latin America

- 7.6.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.6.1.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Country, 2016 - 2026 (USD Million)

- 7.6.2. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026

- 7.6.2.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026 (USD Million)

- 7.6.3. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026

- 7.6.3.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026 (USD Million)

- 7.6.4. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026

- 7.6.4.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026 (USD Million)

- 7.6.5. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026

- 7.6.5.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026 (USD Million)

- 7.6.6. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026

- 7.6.6.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026 (USD Million)

- 7.6.7. Brazil

- 7.6.7.1. Brazil Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.6.8. Mexico

- 7.6.8.1. Mexico Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.6.9. Rest of Latin America

- 7.6.9.1. Rest of Latin America Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.6.1. Latin America Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.7. The Middle-East and Africa

- 7.7.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.7.1.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Country, 2016 - 2026 (USD Million)

- 7.7.2. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026

- 7.7.2.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Aircraft, 2016 – 2026 (USD Million)

- 7.7.3. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026

- 7.7.3.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Fluid, 2016 – 2026 (USD Million)

- 7.7.4. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026

- 7.7.4.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Component, 2016 – 2026 (USD Million)

- 7.7.5. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026

- 7.7.5.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Distribution Channel, 2016 – 2026 (USD Million)

- 7.7.6. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026

- 7.7.6.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, by Application, 2016 – 2026 (USD Million)

- 7.7.7. GCC Countries

- 7.7.7.1. GCC Countries Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.7.8. South Africa

- 7.7.8.1. South Africa Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.7.9. Rest of Middle-East Africa

- 7.7.9.1. Rest of Middle-East Africa Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- 7.7.1. The Middle-East and Africa Aerospace & Defense Fluid Conveyance Systems Market, 2016 – 2026 (USD Million)

- Chapter 8 Aerospace & Defense Fluid Conveyance Systems Market – Competitive Landscape

- 8.1. Competitor Market Share – Revenue

- 8.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players

- 8.3. Strategic Developments

- 8.3.1. Acquisitions and Mergers

- 8.3.2. New Products

- 8.3.3. Research & Development Activities

- Chapter 9 Company Profiles

- 9.1. AIM Aerospace

- 9.1.1. Company Overview

- 9.1.2. Product/Service Portfulio

- 9.1.3. AIM Aerospace Sales, Revenue, and Gross Margin

- 9.1.4. AIM Aerospace Revenue and Growth Rate

- 9.1.5. AIM Aerospace Market Share

- 9.1.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.2. Arrowhead Products Corporation

- 9.2.1. Company Overview

- 9.2.2. Product/Service Portfulio

- 9.2.3. Arrowhead Products Corporation Sales, Revenue, and Gross Margin

- 9.2.4. Arrowhead Products Corporation Revenue and Growth Rate

- 9.2.5. Arrowhead Products Corporation Market Share

- 9.2.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.3. Eaton Corporation

- 9.3.1. Company Overview

- 9.3.2. Product/Service Portfulio

- 9.3.3. Eaton Corporation Sales, Revenue, and Gross Margin

- 9.3.4. Eaton Corporation Revenue and Growth Rate

- 9.3.5. Eaton Corporation Market Share

- 9.3.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.4. Encore Group

- 9.4.1. Company Overview

- 9.4.2. Product/Service Portfulio

- 9.4.3. Encore Group Sales, Revenue, and Gross Margin

- 9.4.4. Encore Group Revenue and Growth Rate

- 9.4.5. Encore Group Market Share

- 9.4.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.5. Exotic Metals Forming LLC

- 9.5.1. Company Overview

- 9.5.2. Product/Service Portfulio

- 9.5.3. Exotic Metals Forming LLC Sales, Revenue, and Gross Margin

- 9.5.4. Exotic Metals Forming LLC Revenue and Growth Rate

- 9.5.5. Exotic Metals Forming LLC Market Share

- 9.5.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.6. Flexfab Horizons International

- 9.6.1. Company Overview

- 9.6.2. Product/Service Portfulio

- 9.6.3. Flexfab Horizons International Sales, Revenue, and Gross Margin

- 9.6.4. Flexfab Horizons International Revenue and Growth Rate

- 9.6.5. Flexfab Horizons International Market Share

- 9.6.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.7. GKN plc

- 9.7.1. Company Overview

- 9.7.2. Product/Service Portfulio

- 9.7.3. GKN plc Sales, Revenue, and Gross Margin

- 9.7.4. GKN plc Revenue and Growth Rate

- 9.7.5. GKN plc Market Share

- 9.7.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.8. ITT Corporation

- 9.8.1. Company Overview

- 9.8.2. Product/Service Portfulio

- 9.8.3. ITT Corporation Sales, Revenue, and Gross Margin

- 9.8.4. ITT Corporation Revenue and Growth Rate

- 9.8.5. ITT Corporation Market Share

- 9.8.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.9. Meggitt PLC

- 9.9.1. Company Overview

- 9.9.2. Product/Service Portfulio

- 9.9.3. Meggitt PLC Sales, Revenue, and Gross Margin

- 9.9.4. Meggitt PLC Revenue and Growth Rate

- 9.9.5. Meggitt PLC Market Share

- 9.9.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.10. Parker Hannifin Corporation

- 9.10.1. Company Overview

- 9.10.2. Product/Service Portfulio

- 9.10.3. Parker Hannifin Corporation Sales, Revenue, and Gross Margin

- 9.10.4. Parker Hannifin Corporation Revenue and Growth Rate

- 9.10.5. Parker Hannifin Corporation Market Share

- 9.10.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.11. PFW Aerospace AG

- 9.11.1. Company Overview

- 9.11.2. Product/Service Portfulio

- 9.11.3. PFW Aerospace AG Sales, Revenue, and Gross Margin

- 9.11.4. PFW Aerospace AG Revenue and Growth Rate

- 9.11.5. PFW Aerospace AG Market Share

- 9.11.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.12. Senior plc

- 9.12.1. Company Overview

- 9.12.2. Product/Service Portfulio

- 9.12.3. Senior plc Sales, Revenue, and Gross Margin

- 9.12.4. Senior plc Revenue and Growth Rate

- 9.12.5. Senior plc Market Share

- 9.12.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.13. Stelia Aerospace

- 9.13.1. Company Overview

- 9.13.2. Product/Service Portfulio

- 9.13.3. Stelia Aerospace Sales, Revenue, and Gross Margin

- 9.13.4. Stelia Aerospace Revenue and Growth Rate

- 9.13.5. Stelia Aerospace Market Share

- 9.13.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.14. Triumph Group Inc.

- 9.14.1. Company Overview

- 9.14.2. Product/Service Portfulio

- 9.14.3. Triumph Group Inc. Sales, Revenue, and Gross Margin

- 9.14.4. Triumph Group Inc. Revenue and Growth Rate

- 9.14.5. Triumph Group Inc. Market Share

- 9.14.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.15. Unison Industries

- 9.15.1. Company Overview

- 9.15.2. Product/Service Portfulio

- 9.15.3. Unison Industries Sales, Revenue, and Gross Margin

- 9.15.4. Unison Industries Revenue and Growth Rate

- 9.15.5. Unison Industries Market Share

- 9.15.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.16. United Flexible

- 9.16.1. Company Overview

- 9.16.2. Product/Service Portfulio

- 9.16.3. United Flexible Sales, Revenue, and Gross Margin

- 9.16.4. United Flexible Revenue and Growth Rate

- 9.16.5. United Flexible Market Share

- 9.16.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.17. Zodiac Aerospace

- 9.17.1. Company Overview

- 9.17.2. Product/Service Portfulio

- 9.17.3. Zodiac Aerospace Sales, Revenue, and Gross Margin

- 9.17.4. Zodiac Aerospace Revenue and Growth Rate

- 9.17.5. Zodiac Aerospace Market Share

- 9.17.6. Recent Initiatives, Funding/VC Activities, and Technulogical Innovations

- 9.1. AIM Aerospace

- Chapter 10 Aerospace & Defense Fluid Conveyance Systems — Industry Analysis

- 10.1. Introduction and Taxonomy

- 10.2. Aerospace & Defense Fluid Conveyance Systems Market – Key Trends

- 10.2.1. Market Drivers

- 10.2.2. Market Restraints

- 10.2.3. Market Opportunities

- 10.3. Value Chain Analysis

- 10.4. Key Mandates and Regulations

- 10.5. Technulogy Roadmap and Timeline

- 10.6. Aerospace & Defense Fluid Conveyance Systems Market – Attractiveness Analysis

- 10.6.1. By Aircraft

- 10.6.2. By Fluid

- 10.6.3. By Component

- 10.6.4. By Distribution Channel

- 10.6.5. By Application

- 10.6.6. By Region

- Chapter 11 Industrial Chain, Sourcing Strategy, and Downstream Buyers

- 11.1. Aerospace & Defense Fluid Conveyance Systems Industrial Chain Analysis

- 11.2. Downstream Buyers

- 11.3. Distributors/Traders List

- Chapter 12 Marketing Strategy Analysis

- 12.1. Marketing Channel

- 12.2. Direct Marketing

- 12.3. Indirect Marketing

- 12.4. Marketing Channel Development Trends

- 12.5. Economic/Pulitical Environmental Change

- Chapter 13 Report Conclusion & Key Insights

- 13.1. Key Insights from Primary Interviews & Surveys Respondents

- 13.2. Key Takeaways from Analysts, Consultants, and Industry Leaders

- Chapter 14 Research Approach & Methodulogy

- 14.1. Report Description

- 14.2. Research Scope

- 14.3. Research Methodulogy

- 14.3.1. Secondary Research

- 14.3.2. Primary Research

- 14.3.3. Statistical Models

- 14.3.3.1. Company Share Analysis Model

- 14.3.3.2. Revenue Based Modeling

- 14.3.4. Research Limitations

Inquiry For Buying

Aerospace & Defense Fluid Conveyance Systems

Request Sample

Aerospace & Defense Fluid Conveyance Systems