Clinical Trial Imaging Market Size, Share, and Trends Analysis Report

CAGR :

| Market Size 2023 (Base Year) | USD 2.32 Billion |

| Market Size 2032 (Forecast Year) | USD 4.80 Billion |

| CAGR | 8.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Clinical Trial Imaging By Technology Market Insights

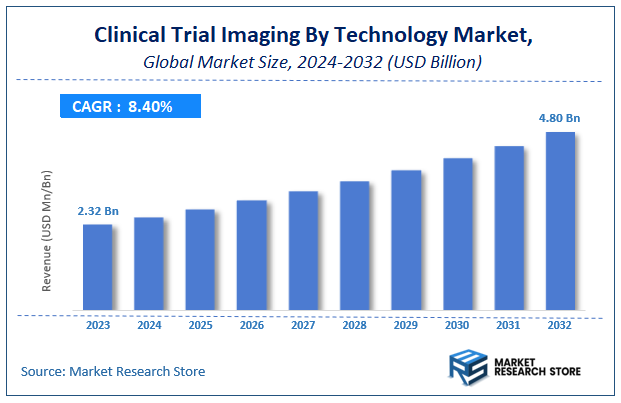

According to Market Research Store, the global clinical trial imaging market size was valued at around USD 2.32 billion in 2023 and is estimated to reach USD 4.80 billion by 2032, to register a CAGR of approximately 8.4% in terms of revenue during the forecast period 2024-2032.

The clinical trial imaging report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Clinical Trial Imaging Market: Overview

Clinical trial imaging refers to the use of medical imaging technologies—such as MRI, CT scans, PET, ultrasound, and X-ray—in the design, conduct, and analysis of clinical trials, particularly in drug development and medical device evaluations. Imaging plays a crucial role in providing objective, quantifiable, and reproducible data for assessing the efficacy and safety of investigational treatments. It is often used to monitor disease progression, evaluate tumor response in oncology trials, identify biomarkers, and support regulatory submissions with visual evidence. These images are typically read by trained radiologists or imaging core labs to ensure consistency and compliance with trial protocols.

The clinical trial imaging market is witnessing significant growth driven by the increasing number of clinical trials globally, particularly in oncology, neurology, and cardiology. Key growth factors include rising demand for precise and early diagnosis, advancements in imaging technologies, and greater emphasis on evidence-based decision-making in drug development.

Key Highlights

- The clinical trial imaging market is anticipated to grow at a CAGR of 8.4% during the forecast period.

- The global clinical trial imaging market was estimated to be worth approximately USD 2.32 billion in 2023 and is projected to reach a value of USD 4.80 billion by 2032.

- The growth of the clinical trial imaging market is being driven by the increasing complexity of clinical trials, the rising demand for advanced imaging biomarkers, and the growing focus on precision medicine and personalized drug development.

- Based on the modality, the computed tomography scan segment is growing at a high rate and is projected to dominate the market.

- On the basis of therapeutic area, the neurovascular diseases segment is projected to swipe the largest market share.

- In terms of services, the clinical trial design and consultation services segment is expected to dominate the market.

- Based on the end use, the biotechnology and pharmaceutical companies segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Clinical Trial Imaging Market: Dynamics

Key Growth Drivers:

- Increasing R&D Spending and Number of Clinical Trials: A significant driver is the continuous and increasing investment by pharmaceutical and biotechnology companies in research and development (R&D) for new drugs and therapies. This leads to a rising number of clinical trials, many of which rely heavily on imaging endpoints for precise assessment of treatment response, disease progression, and patient eligibility, thereby boosting demand for imaging services.

- Growing Prevalence of Chronic Diseases: The increasing global burden of chronic diseases such as cancer, neurological disorders (e.g., Alzheimer's, Parkinson's), cardiovascular diseases, and metabolic disorders necessitates the development of new treatments. Clinical trial imaging is crucial for monitoring these complex diseases and evaluating novel therapeutics, directly expanding its market.

- Advancements in Imaging Technologies and AI Integration: Continuous innovation in imaging modalities (e.g., higher resolution MRI, faster CT scans, advanced PET tracers) and the integration of Artificial Intelligence (AI) and Machine Learning (ML) for image analysis are revolutionizing the market. AI enhances accuracy, efficiency, and speed of data interpretation, enabling faster trial completion times and more reliable results, making imaging more valuable in trials.

Restraints:

- High Costs Associated with Imaging Technologies and Services: The implementation of advanced imaging systems, specialized equipment, and the cost of skilled personnel for image acquisition, reading, and analysis represent a substantial financial burden. These high costs can limit accessibility, particularly for smaller pharmaceutical companies, research institutions, and in developing regions with budget constraints.

- Complexity of Data Management and Integration: Clinical trials generate vast amounts of complex imaging data, alongside other clinical and genomic data. Managing, standardizing, integrating, and securely storing this heterogeneous data across multiple sites and regulatory frameworks is a significant challenge, requiring sophisticated and costly data management systems.

Opportunities:

- Expansion of Decentralized Clinical Trials (DCTs): The growing adoption of decentralized clinical trials, driven by the need for increased patient access and reduced site burden, presents an opportunity for remote imaging solutions, teleimaging, and cloud-based platforms. This allows for image acquisition closer to patients' homes, improving recruitment and retention.

- Growing Role of Contract Research Organizations (CROs): The increasing trend of outsourcing clinical trial activities to CROs is a significant opportunity. CROs often provide comprehensive imaging services, including trial design, operational imaging, and image analysis, allowing pharmaceutical companies to streamline their R&D processes and leverage specialized expertise.

Challenges:

- Shortage of Skilled Radiologists and Image Analysts: There is a persistent global shortage of highly specialized radiologists and image analysts with expertise in interpreting complex clinical trial imaging data and adhering to specific trial protocols. This talent gap can lead to delays in data analysis and potentially impact the efficiency and timelines of trials.

- Interoperability and Data Exchange Issues: Ensuring seamless interoperability between different imaging systems, data platforms, and clinical trial management systems (CTMS) is a complex challenge. Lack of standardized data formats and robust exchange protocols can hinder efficient data flow and analysis across disparate systems.

Clinical Trial Imaging By Technology Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Clinical Trial Imaging By Technology Market |

| Market Size in 2023 | USD 2.32 Billion |

| Market Forecast in 2032 | USD 4.80 Billion |

| Growth Rate | CAGR of 8.4% |

| Number of Pages | 145 |

| Key Companies Covered | Cardiovascular Imaging Technologies, VirtualScopic, Biomedical Systems, BioClinica, Intrinsic Imaging LLC, Prism Clinical Imaging, PAREXEL International Corporation, and ICON |

| Segments Covered | By Product Type, By Technology, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Clinical Trial Imaging Market: Segmentation Insights

The global clinical trial imaging market is divided by modality, therapeutic area, services, end use, and region.

Based on modality, the global clinical trial imaging market is divided into computed tomography scan, magnetic resonance imaging, x-ray, ultrasound, optical coherence tomography (OCT), and other modalities. Computed Tomography (CT) Scan dominates the clinical trial imaging market by modality due to its widespread usage, high-resolution imaging capabilities, and rapid image acquisition, which are essential for evaluating disease progression and treatment efficacy in oncology, cardiovascular, and neurological trials. CT scans provide detailed cross-sectional images, enabling precise measurement of tumor size and organ morphology. Their integration with advanced contrast agents further enhances visualization, making them ideal for multicenter clinical trials requiring standardized and reproducible data.

On the basis of therapeutic area, the global clinical trial imaging market is bifurcated into neurovascular diseases, cardiovascular diseases, orthopedics & msk disorders, oncology, ophthalmology, nephrology, and other therapeutic areas. Neurovascular Diseases dominate the clinical trial imaging market by therapeutic area due to the critical role imaging plays in evaluating neurological conditions such as stroke, multiple sclerosis, Alzheimer’s disease, and brain tumors. Advanced imaging modalities like MRI and CT are essential for detecting structural and functional brain changes, tracking disease progression, and assessing therapeutic efficacy. Functional MRI (fMRI), diffusion tensor imaging (DTI), and perfusion imaging are particularly valuable in neuroscience trials for monitoring neural connectivity and perfusion abnormalities. The rising incidence of neurodegenerative diseases and the growing pipeline of CNS-targeted therapies continue to drive demand for imaging in this segment.

Based on services, the global clinical trial imaging market is divided into clinical trial design and consultation services, reading and analytical services, operational imaging services, system and technology support services, and project and data management. Clinical Trial Design and Consultation Services dominate the clinical trial imaging services segment due to their crucial role in setting the foundation for imaging protocols and trial efficiency. These services include strategic planning, endpoint definition, imaging modality selection, regulatory guidance, and protocol development tailored to therapeutic areas such as oncology, neurology, or cardiology. Sponsors increasingly rely on expert consultation early in the trial design process to mitigate imaging variability, ensure regulatory compliance (e.g., FDA, EMA), and optimize timelines. The growing complexity of clinical trials and the demand for precise, image-based biomarkers underscore the importance of consultation services in accelerating drug development.

In terms of end use, the global clinical trial imaging market is bifurcated into biotechnology and pharmaceutical companies, medical devices manufacturers, academic and government research institutes, contract research organizations (CROS), and other end users. Biotechnology and Pharmaceutical Companies segment dominates the Clinical Trial Imaging Market, driven by the growing emphasis on precision medicine and the increasing number of drug candidates in the clinical pipeline. These companies utilize advanced imaging technologies such as MRI, CT, and PET scans to assess drug efficacy, detect early treatment responses, and provide visual evidence for regulatory submissions. Imaging plays a vital role in supporting endpoint evaluation and safety monitoring, particularly in oncology, neurology, and cardiology trials. The rising prevalence of chronic diseases and the demand for accelerated drug development timelines are further propelling the need for imaging integration in clinical research conducted by biopharma companies.

Clinical Trial Imaging Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the clinical trial imaging market due to its highly developed healthcare infrastructure, extensive pharmaceutical R&D activities, and early adoption of advanced imaging modalities in clinical trials. The United States, in particular, is home to major pharmaceutical companies and contract research organizations (CROs) that rely heavily on imaging biomarkers for evaluating drug efficacy and safety. The presence of regulatory frameworks from the FDA and technological expertise in MRI, PET, CT, and ultrasound imaging further supports market leadership. Additionally, increasing investments in precision medicine and oncology trials—where imaging plays a critical role in endpoint validation—fuel demand for centralized imaging services and advanced analytics in this region.

Asia-Pacific region is emerging rapidly as a key growth area in the clinical trial imaging market. Countries including China, India, Japan, and South Korea are seeing an expansion in clinical trial activity due to large patient populations, cost advantages, and improved regulatory pathways. The integration of imaging in trials is gaining momentum, particularly in oncology, rare diseases, and autoimmune disorders. Japan is notable for its advanced imaging technology adoption, while India and China attract multinational pharmaceutical companies looking to conduct large-scale trials with imaging endpoints. Regional growth is further supported by increased investment in medical imaging infrastructure and digital platforms for centralized image analysis.

Europe holds a significant share of the global clinical trial imaging market, driven by robust academic research, government funding for drug development, and a well-established network of research institutions and hospitals. Countries such as Germany, the United Kingdom, France, and Switzerland actively conduct multicenter clinical trials with integrated imaging protocols. Regulatory bodies like the European Medicines Agency (EMA) support the standardization of imaging in clinical trials, enhancing credibility and data quality. The growing need for faster patient recruitment and advanced imaging solutions, especially in neurology and cardiology trials, sustains the demand for imaging services across the region.

Clinical Trial Imaging Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the clinical trial imaging market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global clinical trial imaging market include:

- IXICO plc

- Navitas Life Sciences

- Resonance Health

- ProScan Imaging

- Radiant Sage LLC

- Medpace

- Biomedical Systems Corp

- Cardiovascular Imaging Technologies

- Intrinsic Imaging

- BioTelemetry

- VirtualScopic

- BioClinica

- Prism Clinical Imaging

- PAREXEL International Corporation

- ICON

The global clinical trial imaging market is segmented as follows:

By Modality

- Computed Tomography Scan

- Magnetic Resonance Imaging

- X-Ray

- Ultrasound

- Optical Coherence Tomography (OCT)

- Other Modalities

By Therapeutic Area

- Neurovascular Diseases

- Cardiovascular Diseases

- Orthopedics & MSK Disorders

- Oncology

- Ophthalmology

- Nephrology

- Other Therapeutic Areas

By Services

- Clinical Trial Design and Consultation Services

- Reading and Analytical Services

- Operational Imaging Services

- System and Technology Support Services

- Project and Data Management

By End Use

- Biotechnology and Pharmaceutical Companies

- Medical Devices Manufacturers

- Academic and Government Research Institutes

- Contract Research Organizations (CROs)

- Other End Users

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Preface

- 1.1. Report description

- 1.2. Research scope

- 1.3. Research methodology

- 1.4. Market research process

- 1.5. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global clinical trial imaging market, 2015 - 2021 (USD Million)

- 2.2. Global clinical trial imaging market : Snapshot

- Chapter 3. Clinical Trial Imaging – Industry Analysis

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Drivers for global clinical trial imaging market: Impact analysis

- 3.2.1.1. Rising geriatric population and growing occurrences of chronic diseases

- 3.2.1.2. Growth in pharmaceutical & biotechnology industries

- 3.2.1. Drivers for global clinical trial imaging market: Impact analysis

- 3.3. Market Restraints

- 3.3.1. Restraints for Global Clinical Trial Imaging Market: Impact Analysis

- 3.3.1.1. High cost of machinery

- 3.3.1. Restraints for Global Clinical Trial Imaging Market: Impact Analysis

- 3.4. Opportunities

- 3.4.1. Porter’s Five Forces Analysis

- 3.5. Clinical Trial Imaging : Market Attractiveness Analysis

- 3.5.1. Market Attractiveness Analysis by Product Segment

- 3.5.2. Market Attractiveness Analysis by Technology Segment

- 3.5.3. Market Attractiveness Analysis by End-User Segment

- 3.5.4. Market Attractiveness Analysis by Regional Segment

- Chapter 4. Clinical Trail Imaging Market – Competitive Landscape

- 4.1. Company Market Share Analysis, 2014

- 4.2. Patent Analysis (2001 – 2016)

- 4.2.1. Number of Patents (2001 – 2016)

- 4.2.2. Patent Share, by Geography

- 4.2.3. Patent Share by Company

- 4.2.4. U.S. (U.S. Patent)

- 4.2.5. Europe (EP Documents)

- 4.2.6. Japan (Abstract of Japan)

- 4.2.7. Global (WIPO (PCT))

- Chapter 5. Clinical Trial Imaging Market – Product Segment Analysis

- 5.1.1. Global clinical trial imaging market overview: by product

- 5.1.1.1. Global clinical trial imaging market revenue share, by product, 2015 & 2021

- 5.2. Service

- 5.2.1. Global clinical trial imaging market for service, 2015 – 2021 (USD Million)

- 5.3. Software

- 5.3.1. Global clinical trial imaging market for software, 2015 – 2021 (USD Million)

- 5.1.1. Global clinical trial imaging market overview: by product

- Chapter 6. Clinical Trial Imaging Market – Technology Segment Analysis

- 6.1. Global clinical trial imaging market overview: by technology

- 6.1.1. Global clinical trial imaging market revenue share, by technology, 2015 & 2021

- 6.2. X-ray

- 6.2.1. Global clinical trial imaging market for X-ray, 2015 – 2021 (USD Million)

- 6.3. CT

- 6.3.1. Global clinical trial imaging market for CT, 2015 – 2021 (USD Million)

- 6.4. MRI

- 6.4.1. Global clinical trial imaging market for MRI, 2015 – 2021 (USD Million)

- 6.5. PET

- 6.5.1. Global clinical trial imaging market for PET, 2015 – 2021 (USD Million)

- 6.6. Echo

- 6.6.1. Global clinical trial imaging market for echo, 2015 – 2021 (USD Million)

- 6.7. Ultrasound

- 6.7.1. Global clinical trial imaging market for ultrasound, 2015 – 2021 (USD Million)

- 6.8. Others

- 6.8.1. Global clinical trial imaging market for others, 2015 – 2021 (USD Million)

- 6.1. Global clinical trial imaging market overview: by technology

- Chapter 7. Clinical Trial Imaging Market – End User Segment Analysis

- 7.1. Global clinical trial imaging market overview: by end user

- 7.1.1. Global clinical trial imaging market revenue share, by end user, 2015 & 2021

- 7.2. Biotech Companies

- 7.2.1. Global clinical trial imaging market for biotech companies, 2015 – 2021 (USD Million)

- 7.3. Pharmaceutical

- 7.3.1. Global clinical trial imaging market for pharmaceutical, 2015 – 2021 (USD Million)

- 7.4. Research Centers

- 7.4.1. Global clinical trial imaging market for research centers, 2015 – 2021 (USD Million)

- 7.5. Hospitals

- 7.5.1. Global clinical trial imaging market for hospitals, 2015 – 2021 (USD Million)

- 7.6. Others

- 7.6.1. Global clinical trial imaging market for other end-uses, 2015 – 2021 (USD Million)

- 7.1. Global clinical trial imaging market overview: by end user

- Chapter 8. Clinical Trial Imaging Market – Regional Analysis

- 8.1. Global Clinical Trial Imaging Market : Regional Overview

- 8.1.1. Global clinical trial imaging market revenue share, by region, 2015 & 2021

- 8.2. North America

- 8.2.1. North America clinical trial imaging market, 2015 - 2021 (USD Million)

- 8.3. North America clinical trial imaging market revenue by product, 2014 - 2020 (USD Million)

- 8.3.1. North America clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.4. North America clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.5. U.S.

- 8.5.1. U.S. clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.5.2. U.S. clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.5.3. U.S. clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.6. Europe

- 8.6.1. Europe clinical trial imaging market, 2015 - 2021 (USD Million)

- 8.6.2. Europe clinical trial imaging market revenue by product, 2014 - 2020 (USD Million)

- 8.6.3. Europe clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.6.4. Europe clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.7. UK

- 8.7.1. UK clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.7.2. UK clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.7.3. UK clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.8. France

- 8.8.1. France clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.8.2. France clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.8.3. France clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.8.4. Germany

- 8.8.4.1. Germany clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.8.4.2. Germany clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.8.4.3. Germany clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.9. Asia Pacific

- 8.9.1. Asia Pacific clinical trial imaging market, 2015 - 2021 (USD Million)

- 8.9.2. Asia Pacific clinical trial imaging market revenue by product, 2014 - 2020 (USD Million)

- 8.9.3. Asia Pacific clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.9.4. Asia Pacific clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.9.5. China

- 8.9.5.1. China clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.9.5.2. China clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.9.5.3. China clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.9.6. Japan

- 8.9.6.1. Japan clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.9.6.2. Japan clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.9.6.3. Japan clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.9.7. India

- 8.9.7.1. India clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.9.7.2. India clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.9.7.3. India clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.10. Latin America

- 8.10.1. Latin America clinical trial imaging market, 2015 - 2021 (USD Million)

- 8.10.2. Latin America clinical trial imaging market revenue by product, 2014 - 2020 (USD Million)

- 8.10.3. Latin America clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.10.4. Latin America clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.10.5. Brazil

- 8.10.5.1. Brazil clinical trial imaging market revenue, by product, 2015 – 2021 (USD Million)

- 8.10.5.2. Brazil clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.10.5.3. Brazil clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.11. Middle East & Africa

- 8.11.1. Middle East & Africa clinical trial imaging market, 2015 - 2021 (USD Million)

- 8.11.2. Middle East & Africa clinical trial imaging market revenue by product, 2014 - 2020 (USD Million)

- 8.11.3. Middle East & Africa clinical trial imaging market revenue, by technology, 2015 – 2021 (USD Million)

- 8.11.4. Middle East & Africa clinical trial imaging market revenue, by end-user, 2015 – 2021 (USD Million)

- 8.1. Global Clinical Trial Imaging Market : Regional Overview

- Chapter 9. Company Profile

- 9.1. ICON plc

- 9.1.1. Overview

- 9.1.2. Financials

- 9.1.3. Product Portfolio

- 9.1.4. Business strategies

- 9.1.5. Recent Developments

- 9.2. PAREXEL International Corporation

- 9.2.1. Overview

- 9.2.2. Financials

- 9.2.3. Product Portfolio

- 9.2.4. Business Strategy

- 9.2.5. Recent developments

- 9.3. Cardiovascular Imaging Technologies, LLC.

- 9.3.1. Company overview

- 9.3.2. Financial

- 9.3.3. Product portfolio

- 9.3.4. Business strategy

- 9.4. Biomedical Systems

- 9.4.1. Overview

- 9.4.2. Financials

- 9.4.3. Product portfolio

- 9.4.4. Business strategies

- 9.4.5. Recent Developments

- 9.5. BioClinica

- 9.5.1. Overview

- 9.5.2. Financials

- 9.5.3. Product portfolio

- 9.5.4. Business strategies

- 9.5.5. Recent Developments

- 9.6. Prism Clinical Imaging

- 9.6.1. Overview

- 9.6.2. Financials

- 9.6.3. Product portfolio

- 9.6.4. Business strategies

- 9.7. VirtualScopics

- 9.7.1. Overview

- 9.7.2. Product portfolio

- 9.7.3. Business strategies

- 9.7.4. Recent Developments

- 9.8. Intrinsic Imaging LLC

- 9.8.1. Overview

- 9.8.2. Financials

- 9.8.3. Product portfolio

- 9.1. ICON plc

Inquiry For Buying

Clinical Trial Imaging

Request Sample

Clinical Trial Imaging