3D Printing Materials Market Size, Share, and Trends Analysis Report

CAGR :

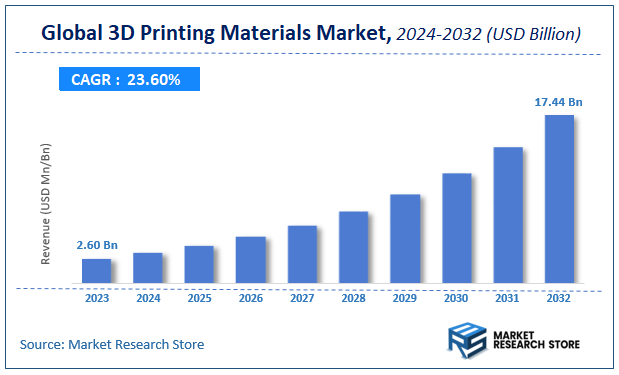

| Market Size 2023 (Base Year) | USD 2.60 Billion |

| Market Size 2032 (Forecast Year) | USD 17.44 Billion |

| CAGR | 23.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

3D Printing Materials Market Insights

According to Market Research Store, the global 3D printing materials market size was valued at around USD 2.60 billion in 2023 and is estimated to reach USD 17.44 billion by 2032, to register a CAGR of approximately 23.6% in terms of revenue during the forecast period 2024-2032.

The 3D printing materials report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global 3D Printing Materials Market: Overview

3D printing materials are specialized substances used as feedstock in additive manufacturing processes to create three-dimensional objects layer by layer from digital models. These materials come in various forms—such as filaments, powders, resins, and pellets—and are selected based on the printing technology (e.g., FDM, SLA, SLS, or DMLS) and the desired mechanical, thermal, and aesthetic properties of the final product. Common categories of 3D printing materials include thermoplastics (like PLA, ABS, PETG, and nylon), photopolymers, metals (such as titanium, aluminum, and stainless steel), ceramics, and composites infused with carbon fiber or glass.

The growth of the 3D printing materials market is driven by the rapid adoption of additive manufacturing across industries including aerospace, automotive, healthcare, consumer goods, and construction. The demand for customized, lightweight, and high-performance parts has led to significant innovation in material development, including bio-based polymers, medical-grade biocompatible resins, and high-temperature alloys.

Key Highlights

- The 3D printing materials market is anticipated to grow at a CAGR of 23.6% during the forecast period.

- The global 3D printing materials market was estimated to be worth approximately USD 2.60 billion in 2023 and is projected to reach a value of USD 17.44 billion by 2032.

- The growth of the 3D printing materials market is being driven by rapid advancements in additive manufacturing technologies and increasing adoption across various industries such as aerospace.

- Based on the product, the photopolymers segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the aerospace & defense segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

3D Printing Materials Market: Dynamics

Key Growth Drivers:

- Increasing Adoption of 3D Printing Technology Across Industries: The foundational driver is the growing proliferation of 3D printers in various sectors, including automotive, aerospace & defense, healthcare, consumer goods, and industrial manufacturing. As more industries realize the benefits of additive manufacturing (e.g., rapid prototyping, complex geometries, customized parts, on-demand production), the demand for diverse 3D printing materials naturally increases.

- Demand for Customization and Personalization: 3D printing excels at producing highly customized and personalized parts efficiently. This is particularly critical in industries like healthcare (e.g., patient-specific implants, prosthetics, dental aligners), consumer goods (e.g., custom eyewear, footwear), and luxury goods, driving demand for a wide array of specialized materials.

- Focus on Rapid Prototyping and Product Development: 3D printing significantly accelerates the product development cycle by enabling fast and cost-effective creation of prototypes. This capability is invaluable for R&D departments across virtually all manufacturing sectors, leading to continuous demand for prototyping materials.

- Growth in End-Use Part Production: Beyond prototyping, there's a significant shift towards using 3D printing for producing functional, end-use parts. This requires higher performance materials that can withstand demanding operational conditions, thus expanding the market for industrial-grade polymers, metals, and composites.

Restraints:

- High Cost of Advanced Materials: Many high-performance 3D printing materials, especially specialty resins, advanced polymers, and metal powders, are significantly more expensive than their traditional manufacturing counterparts. This high material cost can be a barrier to widespread adoption for mass production.

- Limited Availability of Materials for Specific Applications: While the material range is expanding, there are still limitations in the types and grades of materials available that meet the specific performance, regulatory, or certification requirements for certain highly demanding industries (e.g., aerospace, medical implants).

- Complex Material Characterization and Qualification: Qualifying 3D printed parts and their materials for critical applications (e.g., aerospace, automotive safety parts) is a complex, time-consuming, and expensive process. Ensuring consistent material properties and repeatability across different prints and machines is a significant hurdle.

Opportunities:

- Development of Novel and High-Performance Materials: The largest opportunity lies in continuous R&D to develop entirely new 3D printing materials with enhanced properties (e.g., multi-material capabilities, self-healing, smart functionalities, extreme temperature resistance) that unlock new applications previously impossible.

- Bio-based and Sustainable Materials: The growing demand for sustainable manufacturing creates a significant opportunity for developing bio-based, biodegradable, and recyclable 3D printing materials derived from renewable resources, reducing the environmental footprint of additive manufacturing.

- Customized Materials for Specific Printer Technologies: Opportunities exist in tailoring materials specifically for optimal performance with particular 3D printing technologies (e.g., binder jetting, SLA, FDM, DMLS), leading to improved print quality, speed, and part integrity.

Challenges:

- Cost Reduction of High-Performance Materials: A critical challenge is to significantly reduce the cost of advanced 3D printing materials to make them more economically viable for large-scale production, without compromising performance.

- Ensuring Material Consistency and Quality Control: Maintaining consistent material properties, batch-to-batch, and ensuring reliable print outcomes across different machines and environments is a major challenge, especially for regulated industries.

3D Printing Materials Market: Report Scope

This report thoroughly analyzes the 3D Printing Materials Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | 3D Printing Materials Market |

| Market Size in 2023 | USD 2.60 Billion |

| Market Forecast in 2032 | USD 17.44 Billion |

| Growth Rate | CAGR of 23.6% |

| Number of Pages | 150 |

| Key Companies Covered | Stratasys Ltd. (U.S.), ExOne Gmbh (Germany), SLM Solutions GmbH, Voxeljet AG, Concept Laser GmbH, Arcam AB, and 3D Systems, Inc |

| Segments Covered | By Product, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

3D Printing Materials Market: Segmentation Insights

The global 3D printing materials market is divided by product, application, and region.

Based on product, the global 3D printing materials market is divided into photopolymers, thermoplastics, metals, and others. Photopolymers dominate the 3D printing materials market due to their high precision, excellent surface finish, and compatibility with a variety of additive manufacturing technologies, particularly stereolithography (SLA) and digital light processing (DLP). These materials are widely used in applications that demand intricate detailing, such as dental models, jewelry prototypes, medical devices, and concept modeling in consumer goods. Photopolymers are ideal for creating complex geometries with smooth finishes and thin walls, making them indispensable in design validation and small-batch production. Their dominance is further supported by advancements in resin formulations, including bio-compatible and engineering-grade variants that expand their use in healthcare and functional prototyping. Additionally, the ability to rapidly cure under UV light enables faster production cycles, which is critical for industries requiring high-speed and high-accuracy outputs.

On the basis of application, the global 3D printing materials market is bifurcated into aerospace & defense, medical, automotive, consumer products & industrial, and others. Aerospace & Defense is the dominant application segment in the 3D printing materials market, primarily due to the industry's continuous demand for lightweight, high-strength, and geometrically complex components. Additive manufacturing enables the production of parts with intricate internal structures, reducing both weight and material usage—key requirements for fuel efficiency and payload optimization in aircraft and spacecraft. 3D printing also allows for the customization and on-demand manufacturing of replacement parts, which streamlines maintenance operations and reduces inventory costs. Materials such as high-performance thermoplastics (e.g., ULTEM) and metal powders (e.g., titanium and Inconel) are widely used in this sector for applications ranging from engine components to cabin interior parts. The stringent standards for mechanical performance and reliability in aerospace and defense have driven technological advancements in both materials and additive processes, solidifying this segment's leading position.

3D Printing Materials Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the 3D printing materials market due to its strong technological infrastructure, well-established additive manufacturing ecosystem, and high investment in aerospace, healthcare, automotive, and defense applications. The United States leads regional demand with a significant concentration of key players such as Stratasys, 3D Systems, and HP. The region benefits from robust R&D funding, government support for advanced manufacturing, and early adoption of 3D printing in industrial prototyping and production. Materials such as photopolymers, thermoplastics (like ABS and PLA), metal powders (such as titanium and stainless steel), and advanced composites are widely used across industries. The medical sector, in particular, drives demand for biocompatible resins and polymers for prosthetics, implants, and dental devices. Additionally, aerospace manufacturers are rapidly adopting high-performance metal alloys and carbon fiber-reinforced materials to improve part strength and reduce weight. Strong supply chain infrastructure and increasing investment in material innovation solidify North America's dominant position.

Europe holds a significant share in the 3D printing materials market, with Germany, the UK, France, and Italy leading adoption. Germany, as a major hub for engineering and automotive manufacturing, uses advanced materials like nylon, aluminum, and metal composites in both prototyping and end-use parts. Europe is also at the forefront of sustainable 3D printing practices, with growing demand for recyclable and bio-based materials. The medical and dental sectors in the UK and France are increasing their reliance on 3D printed resins and ceramics for patient-specific solutions. Research institutions and government initiatives under the Horizon Europe program are promoting the development of next-generation materials for additive manufacturing. Stringent quality standards and certifications ensure high material reliability, which supports their use in critical aerospace and industrial applications. Europe's focus on precision, durability, and environmental responsibility continues to drive material innovation.

Asia-Pacific is the fastest-growing region in the 3D printing materials market, driven by rapid industrialization, expanding electronics and consumer goods manufacturing, and increasing government support for advanced manufacturing. China and Japan are major contributors, with strong demand for thermoplastics, photopolymers, and metal powders in automotive, tooling, and consumer electronics applications. South Korea and India are also emerging players, investing in material R&D and establishing regional supply chains. China's large-scale manufacturing capabilities support high-volume use of PLA and ABS in consumer-grade 3D printers, while high-performance metals are increasingly used in aerospace and medical implants. Japan focuses on high-precision ceramic and resin-based materials used in optics and dental devices. The region faces challenges such as varying material standards and intellectual property concerns but benefits from cost-effective production and strong innovation pipelines.

Latin America is an emerging market for 3D printing materials, with Brazil and Mexico leading regional development. The demand is primarily driven by prototyping, tooling, and small-batch production in automotive, healthcare, and consumer product sectors. Brazil has a growing interest in PLA, ABS, and resin materials used in desktop 3D printing and education, while Mexico’s automotive supply chain increasingly adopts metal powders and composites for tooling applications. Material availability is gradually improving through partnerships with global manufacturers, although local production remains limited. Challenges such as high material costs, lack of standardization, and limited access to high-end industrial equipment persist, but ongoing investment in education and technical infrastructure supports gradual market development.

Middle East & Africa represent a developing but promising market for 3D printing materials, with the UAE, Saudi Arabia, and South Africa leading adoption. In the Middle East, government-backed smart city and digital manufacturing initiatives are driving demand for construction-grade materials, thermoplastics, and photopolymers in architectural and industrial applications. The UAE has demonstrated the use of cementitious materials in large-scale 3D printed buildings. In Africa, South Africa is investing in local material production, especially for titanium powders and polymers used in aerospace and healthcare. Despite infrastructure and knowledge limitations, interest in localized manufacturing and sustainable material alternatives is growing. International collaborations and rising adoption in education and prototyping are expected to support long-term material demand across both public and private sectors.

3D Printing Materials Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the 3D printing materials market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global 3D printing materials market include:

- ATI

- CNPC Powder

- Colibrium Additive

- GKN Powder Metallurgy

- Höganäs AB

- Kennametal Inc.

- Arkema Inc.

- CRP Technology

- Stratasys Ltd.

- Saudi Basic Industries Corporation (SABIC)

- Polyone Corporation

- Koninklijke DSM N.V.

- ExOne

- Sandvik AB

- 3D Systems, Inc

- Evonik Industries AG

- CeramTec GmbH

- BASF SE

- DuPont

- Materialise NV

The global 3D printing materials market is segmented as follows:

By Product

- Photopolymers

- Thermoplastics

- Metals

- Others

By Application

- Aerospace & Defense

- Medical

- Automotive

- Consumer Products & Industrial

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global 3D printing materials market volume and revenue, 2014 - 2020 (Tons) (USD Million)

- 2.2. Global 3D printing materials market: Snapshot

- Chapter 3. 3D Printing Materials Market – Market Dynamics

- 3.1. Introduction

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Global 3D printing materials market: Impact analysis

- 3.3.2. Rapid growth in 3D printing technology

- 3.3.3. Increasing use in healthcare market

- 3.4. Market restraints

- 3.4.1. Restraints for Global 3D printing materials market: Impact analysis

- 3.4.2. High cost

- 3.4.3. Complex manufacturing

- 3.5. Opportunities

- 3.5.1. Advancement in scanning and 3D printing

- 3.6. Porter’s five forces analysis

- 3.6.1. Bargaining power of suppliers

- 3.6.2. Bargaining power of buyers

- 3.6.3. Threat from new entrants

- 3.6.4. Threat from new substitutes

- 3.6.5. Degree of competition

- 3.7. Market attractiveness analysis

- 3.7.1. Market attractiveness analysis by application segment

- 3.7.2. Market attractiveness analysis by regional segment

- Chapter 4. Global 3D Printing Materials Market – Competitive Landscape

- 4.1. Global 3D printing materials company market share

- 4.2. Global 3D printing materials market: Production capacity (subject to data availability)

- 4.3. Global 3D printing materials market : Row material analysis

- 4.4. Global 3D printing materials market : Price Analysis

- Chapter 5. Global 3D Printing Materials Market – Product Segment Analysis

- 5.1. Global 3D printing materials market: Product overview

- 5.1.1. Global 3D printing materials market volume share by product, 2014 and 2020

- 5.2. Plastics

- 5.2.1. Global plastics market , 2014 – 2020 (Tons) (USD Million)

- 5.3. Ceramics

- 5.3.1. Global ceramics market, 2014 – 2020 (Tons) (USD Million)

- 5.4. Metals

- 5.4.1. Global metals market, 2014 – 2020 (Tons) (USD Million)

- 5.5. Others

- 5.5.1. Global other materials 3D printing market, 2014 – 2020 ( Tons) (USD Million)

- 5.1. Global 3D printing materials market: Product overview

- Chapter 6. Global 3D Printing Materials Market – Application Segment Analysis

- 6.1. Global 3D printing materials market: Application overview

- 6.1.1. Global 3D printing materials market volume share by application, 2014 and 2020

- 6.2. Electronics & consumer

- 6.2.1. Global 3D printing materials market for electronics & consumer , 2014 – 2020 (Tons) (USD Million)

- 6.3. Automotive

- 6.3.1. Global 3D Printing materials market for automotive, 2014 – 2020 (Tons) (USD Million)

- 6.4. Medical

- 6.4.1. Global 3D printing materials market for medical , 2014 – 2020 (Tons) (USD Million)

- 6.5. Industrial

- 6.5.1. Global 3D printing materials market for industrial, 2014 – 2020 (Tons) (USD Million)

- 6.6. Education

- 6.6.1. Global 3D printing materials market for education, 2014 – 2020 (Tons) (USD Million)

- 6.7. Aerospace

- 6.7.1. Global 3D printing materials market for aerospace, 2014 – 2020 (Tons) (USD Million)

- 6.8. Other

- 6.8.1. Global 3D printing materials market for other applications, 2014 – 2020 (Tons) (USD Million)

- 6.1. Global 3D printing materials market: Application overview

- Chapter 7. Global 3D Printing Materials Market – Regional Segment Analysis

- 7.1. Global 3D printing materials market: Regional overview

- 7.1.1. Global 3D printing materials market volume share, by region, 2014 and 2020

- 7.2. North America

- 7.2.1. North America 3D printing materials market volume, by product, 2014 – 2020, ( Tons)

- 7.2.2. North America 3D printing materials market revenue, by product, 2014 – 2020, (USD Million)

- 7.2.3. North America 3D printing materials market volume, by end- users, 2014 – 2020 ( Tons)

- 7.2.4. North America 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.2.5. U.S.

- 7.2.5.1. U.S. 3D printing materials market volume, by Product, 2014 – 2020 ( Tons)

- 7.2.5.2. U.S. 3D printing materials market revenue, by Product, 2014 – 2020 (USD Million)

- 7.2.5.3. U.S. 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.2.5.4. U.S. 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.3. Europe

- 7.3.1. Europe 3D printing materials market volume, by product, 2014 – 2020 (Tons)

- 7.3.2. Europe 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.3. Europe 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.3.4. Europe 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.3.5. Germany

- 7.3.5.1. Germany 3D printing materials market volume, by product, 2014 – 2020, ( Tons)

- 7.3.5.2. Germany 3D printing materials market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.5.3. Germany 3D printing materials market volume, by end-users, 2014 – 2020, ( Tons)

- 7.3.5.4. Germany 3D printing materials market revenue, by end-users, 2014 – 2020, (USD Million)

- 7.3.6. France

- 7.3.6.1. France 3D printing materials market volume, by product, 2014 – 2020, ( Tons)

- 7.3.6.2. France 3D printing materials market revenue, by product, 2014 – 2020, (USD Million)

- 7.3.6.3. France 3D printing materials market volume, by end-users, 2014 – 2020, ( Tons)

- 7.3.6.4. France 3D printing materials market revenue, by end-users, 2014 – 2020, (USD Million)

- 7.3.7. UK

- 7.3.7.1. UK 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.3.7.2. UK 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.3.7.3. UK 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.3.7.4. UK 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.4.2. Asia Pacific 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.3. Asia Pacific 3D printing materials market volume, by end-users, 2014 – 2020, ( Tons)

- 7.4.4. Asia Pacific 3D printing materials market revenue, by end-users, 2014 – 2020, (USD Million)

- 7.4.5. China

- 7.4.5.1. China 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.4.5.2. China 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.5.3. China 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.4.5.4. China 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.4.6. Japan

- 7.4.6.1. Japan 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.4.6.2. Japan 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.6.3. Japan 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.4.6.4. Japan 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.4.7. India

- 7.4.7.1. India 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.4.7.2. India 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.4.7.3. India 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.4.7.4. India 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.5.2. Latin America 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.3. Latin America 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.5.4. Latin America 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.5.5. Brazil

- 7.5.5.1. Brazil 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.5.5.2. Brazil 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.5.5.3. Brazil 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.5.5.4. Brazil 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa 3D printing materials market volume, by product, 2014 – 2020 ( Tons)

- 7.6.2. Middle East and Africa 3D printing materials market revenue, by product, 2014 – 2020 (USD Million)

- 7.6.3. Middle East and Africa 3D printing materials market volume, by end-users, 2014 – 2020 ( Tons)

- 7.6.4. Middle East and Africa 3D printing materials market revenue, by end-users, 2014 – 2020 (USD Million)

- 7.1. Global 3D printing materials market: Regional overview

- Chapter 8. Company Profile

- 8.1. ExOne Gmbh

- 8.1.1. Overview

- 8.1.2. Financials

- 8.1.3. Product portfolio

- 8.1.4. Business strategy

- 8.1.5. Recent developments

- 8.2. Stratasys Ltd

- 8.2.1. Overview

- 8.2.2. Financials

- 8.2.3. Product portfolio

- 8.2.4. Business strategy

- 8.2.5. Recent developments

- 8.3. SLM Solutions GmbH

- 8.3.1. Overview

- 8.3.2. Financials

- 8.3.3. Product portfolio

- 8.3.4. Business strategy

- 8.3.5. Recent developments

- 8.4. Arcam AB

- 8.4.1. Overview

- 8.4.2. Financials

- 8.4.3. Product portfolio

- 8.4.4. Business strategy

- 8.4.5. Recent developments

- 8.5. Concept Laser GmbH

- 8.5.1. Overview

- 8.5.2. Financials

- 8.5.3. Product portfolio

- 8.5.4. Business strategy

- 8.5.5. Recent developments

- 8.6. 3D Systems, Inc.

- 8.6.1. Overview

- 8.6.2. Financials

- 8.6.3. Product portfolio

- 8.6.4. Business strategy

- 8.6.5. Recent developments

- 8.7. Solidscape, Inc.

- 8.7.1. Overview

- 8.7.2. Financials

- 8.7.3. Product portfolio

- 8.7.4. Business strategy

- 8.7.5. Recent developments

- 8.8. Voxeljet AG

- 8.8.1. Overview

- 8.8.2. Financials

- 8.8.3. Product portfolio

- 8.8.4. Business strategy

- 8.8.5. Recent developments

- 8.9. EOS GmbH Electro Optical Systems

- 8.9.1. Overview

- 8.9.2. Financials

- 8.9.3. Product portfolio

- 8.9.4. Business strategy

- 8.9.5. Recent development

- 8.1. ExOne Gmbh

Inquiry For Buying

3D Printing Materials

Request Sample

3D Printing Materials