Medical Device Interoperability Market Size, Share, and Trends Analysis Report

CAGR :

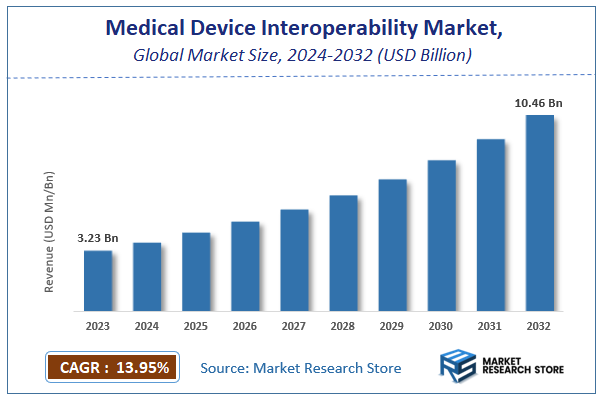

| Market Size 2023 (Base Year) | USD 3.23 Billion |

| Market Size 2032 (Forecast Year) | USD 10.46 Billion |

| CAGR | 13.95% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Medical Device Interoperability Market Insights

According to Market Research Store, the global medical device interoperability market size was valued at around USD 3.23 billion in 2023 and is estimated to reach USD 10.46 billion by 2032, to register a CAGR of approximately 13.95% in terms of revenue during the forecast period 2024-2032.

The medical device interoperability report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Medical Device Interoperability Market: Overview

Medical device interoperability refers to the ability of medical devices and systems to seamlessly exchange, interpret, and use data with other healthcare technologies within and across care settings. This capability enables different devices like patient monitors, infusion pumps, ventilators, imaging systems, and electronic health records (EHRs) to communicate and operate in a coordinated manner, enhancing clinical efficiency and decision-making. Interoperable devices adhere to standardized communication protocols and data formats, such as HL7, FHIR, and IEEE 11073, to ensure compatibility and consistency across various manufacturers and platforms.

The growth of medical device interoperability is driven by the increasing complexity of healthcare delivery, the proliferation of connected devices, and the need for accurate, real-time data to support clinical workflows. Interoperability reduces the likelihood of manual data entry errors, improves patient safety, and facilitates more holistic and personalized care. It also enables more effective remote monitoring, data-driven diagnostics, and automation of documentation processes. With the rise of digital health, regulatory initiatives promoting integration, and the demand for cost-effective healthcare solutions, medical device interoperability is becoming essential for advancing smart hospital infrastructure and achieving better patient outcomes.

Key Highlights

- The medical device interoperability market is anticipated to grow at a CAGR of 13.95% during the forecast period.

- The global medical device interoperability market was estimated to be worth approximately USD 3.23 billion in 2023 and is projected to reach a value of USD 10.46 billion by 2032.

- The growth of the medical device interoperability market is being driven by the rising need for seamless data exchange between healthcare devices, the push toward integrated healthcare systems, and the demand for improved patient outcomes through real-time, data-driven decision-making.

- Based on the industry participants, the clinical IT system vendors segment is growing at a high rate and is projected to dominate the market.

- On the basis of end-user, the hospitals segment is projected to swipe the largest market share.

- In terms of application, the acute care settings segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Medical Device Interoperability Market: Dynamics

Key Growth Drivers:

- Growing Need for Patient-Centric and Coordinated Care: The shift towards value-based care and the need for personalized medicine are driving the demand for interoperability. By integrating data from various medical devices, EHRs, and remote monitoring systems, clinicians can get a holistic view of a patient's health. This leads to better-informed decisions, improved care coordination, and a more positive patient experience.

- Technological Advancements in Connected Health: The proliferation of IoT-enabled medical devices, wearable sensors, and remote patient monitoring solutions is a major driver. These devices generate a massive amount of real-time data. Interoperability is essential to collect, analyze, and integrate this data into a meaningful and usable format for healthcare providers.

- Regulatory Support and Government Initiatives: Governments and regulatory bodies are actively promoting interoperability to improve healthcare quality and safety. Initiatives like the Health Information Technology for Economic and Clinical Health (HITECH) Act in the U.S. and various eHealth funding programs worldwide are providing incentives and mandates for healthcare organizations to adopt interoperable systems.

- Demand for Operational Efficiency and Cost Reduction: Healthcare providers face pressure to reduce costs and increase operational efficiency. Interoperability automates the flow of data, reducing the need for manual data entry, minimizing human error, and freeing up clinical staff to focus on patient care. This streamlining of workflows and reduction in redundant tests can lead to significant cost savings.

Restraints:

- Data Security and Privacy Concerns: The exchange of sensitive patient health information among multiple devices and systems raises significant data security and privacy concerns. The risk of data breaches, unauthorized access, and cyber-attacks on connected devices is a major restraint. Ensuring compliance with regulations like HIPAA and GDPR adds another layer of complexity and cost.

- Lack of Standardization and Technical Incompatibility: The market is fragmented, with a wide variety of medical devices and IT systems from different manufacturers. A lack of universal standards for data formats, communication protocols, and terminologies creates a major barrier to seamless interoperability. This forces healthcare providers to spend time and money on custom integrations, often with limited success.

- High Implementation Costs and Legacy Systems: The high cost of implementing interoperability solutions, which includes software, hardware, and the labor required for integration, can be prohibitive for many healthcare organizations, especially smaller clinics. Many institutions still rely on outdated legacy systems that were not designed for interoperability, making it difficult and expensive to connect them to modern devices.

- Resistance to Change: Despite the benefits, there can be significant resistance to change from healthcare professionals and administrative staff. Clinicians may be hesitant to alter their established workflows, and staff may lack the technical expertise to effectively use new interoperable systems. Overcoming this cultural and educational barrier is a major challenge for market adoption.

Opportunities:

- Expansion of Cloud-Based and SaaS Models: The shift toward cloud-based and Software-as-a-Service (SaaS) models offers a major opportunity. These solutions are more scalable, cost-effective, and easier to deploy and maintain than traditional on-premise systems. They lower the barrier to entry for smaller healthcare facilities and enable real-time data access from any location.

- Integration of AI and Machine Learning: The integration of AI and machine learning into interoperability platforms presents a significant opportunity. AI can analyze the massive datasets generated by connected devices to provide predictive insights, automate clinical workflows, and even assist in diagnosis. This moves the market from just data exchange to data-driven decision-making.

- Growth in Home Healthcare and Remote Patient Monitoring: The growing trend of home healthcare and remote patient monitoring, especially for managing chronic diseases, creates a vast opportunity for interoperability. Solutions that can seamlessly connect in-home medical devices with a patient's EHR and their care team are critical for the long-term success of these care models.

- Strategic Partnerships and Acquisitions: The market is ripe for strategic partnerships between medical device manufacturers, health IT vendors, and technology companies. These collaborations can lead to the development of more standardized, integrated, and comprehensive solutions. Larger companies may also acquire smaller, innovative players to gain a competitive edge and expand their portfolio of interoperable products.

Challenges:

- Ensuring Data Integrity and Accuracy: A key challenge is ensuring the integrity and accuracy of the data being exchanged between multiple devices and systems. Inaccurate or incomplete data can lead to serious medical errors. The system must be designed with robust data validation and error-checking mechanisms to maintain clinical safety.

- Navigating the Complex Regulatory Landscape: The market faces the challenge of navigating a complex and evolving regulatory landscape. Different countries and regions have varying laws and standards for data privacy, device certification, and data exchange. Ensuring compliance across all these jurisdictions is a continuous and resource-intensive challenge for providers.

- Managing the "Black Box" of Algorithmic Decisions: As AI becomes more integrated, there is a challenge related to the "black box" problem, where the reasoning behind an AI-driven decision or recommendation is not transparent. Clinicians need to understand and trust the data and insights provided by the system before they can fully rely on it for patient care.

- Interoperability vs. Connectivity: A major challenge is to differentiate between simple connectivity and true interoperability. While many devices can connect, true interoperability requires a shared understanding of data—its context, meaning, and purpose—which is far more complex to achieve and to explain to potential customers.

Medical Device Interoperability Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Medical Device Interoperability Market |

| Market Size in 2023 | USD 3.23 Billion |

| Market Forecast in 2032 | USD 10.46 Billion |

| Growth Rate | CAGR of 13.95% |

| Number of Pages | 180 |

| Key Companies Covered | Masimo, Boston Scientific Corporation, Koninklijke Philips N.V., Nihon Kohden Corporation, NantHealth, Inc., Abbott, Siemens Healthcare Private Limited, Infosys Limited, Bernoulli, Spacelabs Healthcare, Cerner Corporation, InvivCorporation, Medtronic, GENERAL ELECTRIC COMPANY, Drägerwerk AG & Co. KGaA, Qualcomm Life, Inc., iHealth Labs Inc., FUKUDA DENSHI, and True Process |

| Segments Covered | By Device, By Industry Participants, By End-User, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 t2023 |

| Forecast Year | 2024 t2032 |

| Customization Scope | Avail customized purchase options tmeet your exact research needs. Request For Customization |

Medical Device Interoperability Market: Segmentation Insights

The global medical device interoperability market is divided by industry participants, end-user, application, and region.

Based on industry participants, the global medical device interoperability market is divided into clinical it system vendors, healthcare system integrators, vendor-agnostic connectivity vendors, and medical device OEMs. Clinical IT System Vendors represent the dominant segment in the Medical Device Interoperability Market due to their foundational role in integrating medical devices with electronic health records (EHRs), clinical decision support systems, and other digital infrastructures within healthcare facilities. These vendors facilitate seamless data exchange across disparate systems, enabling better patient monitoring, diagnostics, and care coordination. Their solutions are crucial in ensuring interoperability compliance, particularly with regulatory frameworks like HL7 and FHIR, which are increasingly becoming mandatory in many countries. The growing emphasis on digital healthcare transformation and real-time patient data analytics significantly strengthens the demand for Clinical IT System Vendors.

On the basis of end-user, the global medical device interoperability market is bifurcated into hospitals, ambulatory cares, and clinics & imaging centres. Hospitals dominate the Medical Device Interoperability Market, primarily due to their complex infrastructure and high patient volumes, which necessitate seamless communication among a wide range of medical devices and IT systems. Hospitals typically deploy a large number of interconnected diagnostic, monitoring, and therapeutic devices, all of which must integrate efficiently with electronic health records (EHRs), laboratory systems, and clinical workflows. The need for real-time patient data, improved clinical decision-making, and compliance with interoperability standards like HL7 and FHIR further accelerates hospital investments in interoperable technologies. Additionally, the increasing adoption of smart ICUs and surgical automation in tertiary care settings reinforces hospitals as the leading end-user segment.

In terms of application, the global medical device interoperability market is bifurcated into acute care settings, patient data repositories, and remote patient monitoring. Acute Care Settings constitute the dominant application segment in the Medical Device Interoperability Market due to the critical nature of care delivered in environments such as intensive care units (ICUs), emergency departments, and surgical suites. In these settings, the ability to seamlessly integrate monitoring devices, ventilators, infusion pumps, and other life-support systems with clinical information systems is essential for real-time decision-making and patient safety. Interoperability ensures continuous data flow to electronic health records (EHRs) and centralized monitoring systems, reducing clinical errors and enabling faster response times. As healthcare institutions increasingly focus on critical care modernization and patient outcome optimization, the demand for interoperable solutions in acute care continues to rise sharply.

Medical Device Interoperability Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the medical device interoperability market owing to its advanced healthcare infrastructure, high adoption of digital health technologies, and robust regulatory support for data integration and health IT standards. The United States leads the region due to federal initiatives such as the 21st Century Cures Act and the Office of the National Coordinator for Health Information Technology (ONC)’s interoperability rules, which mandate open APIs and standardized health data exchange. A strong presence of major electronic health record (EHR) vendors, medical device manufacturers, and health tech innovators further accelerates adoption. Moreover, the growing demand for integrated care, increasing deployment of remote patient monitoring systems, and emphasis on reducing hospital readmissions and medical errors drive continuous investment in interoperable solutions across hospital systems, outpatient centers, and telehealth platforms.

Asia-Pacific region is experiencing rapid growth in the medical device interoperability market, driven by healthcare digitization, rising chronic disease burden, and government initiatives supporting health IT integration. Countries such as China, Japan, South Korea, and Australia are investing in health data infrastructure and encouraging interoperability between connected medical devices and electronic medical records. Japan’s efforts to implement interoperable health information exchange networks, combined with China’s national health IT strategy, are fostering strong momentum. The region’s expanding telemedicine usage, increasing deployment of wearable medical devices, and shift toward value-based care models are key drivers for greater interoperability adoption across both public and private healthcare sectors.

Europe holds a significant share of the medical device interoperability market, supported by harmonized digital health strategies across EU nations and increasing investments in eHealth infrastructure. Countries such as Germany, the United Kingdom, the Netherlands, and France are at the forefront of integrating medical devices with health IT systems. The European Commission’s efforts to enhance cross-border health data exchange and implement interoperability frameworks such as the European Electronic Health Record Exchange Format have contributed to market development. Additionally, the region’s focus on chronic disease management, remote diagnostics, and population health analytics is encouraging healthcare providers to adopt interoperable devices that can seamlessly communicate with clinical information systems.

Latin America represents an emerging market for medical device interoperability, with countries like Brazil, Mexico, and Argentina gradually modernizing their healthcare systems through digital transformation. The adoption of EHRs and connected medical devices is growing in urban hospitals, with a strong push for improved care coordination and patient safety. However, the market faces challenges such as infrastructure limitations, fragmented IT systems, and limited regulatory mandates around interoperability. Despite this, regional governments are exploring policies to integrate health systems and support medical device connectivity, which will gradually enhance interoperability, especially in large metropolitan healthcare networks and private healthcare institutions.

Middle East & Africa region is in the early stages of adopting medical device interoperability, with promising developments in countries like the UAE, Saudi Arabia, and South Africa. In the Middle East, national health transformation programs and smart hospital initiatives are driving the implementation of connected devices and integrated health IT platforms. Countries such as the UAE and Saudi Arabia are making notable investments in health informatics and interoperability standards to support digital health ecosystems. Meanwhile, in Africa, the adoption is slower due to infrastructure challenges and limited access to advanced medical technology. However, growing investment in healthcare modernization and international collaboration on digital health projects indicate potential for future growth.

Medical Device Interoperability Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the medical device interoperability market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global medical device interoperability market include:

- Masimo

- Boston Scientific Corporation

- Koninklijke Philips N.V.

- Nihon Kohden Corporation

- NantHealth Inc.

- Abbott

- Siemens Healthcare Private Limited

- Infosys Limited

- Bernoulli

- Spacelabs Healthcare

- Cerner Corporation

- InvivCorporation

- Medtronic

- GENERAL ELECTRIC COMPANY

- Drägerwerk AG & Co. KGaA

- Qualcomm Life Inc.

- iHealth Labs Inc.

- FUKUDA DENSHI

- True Process

The global medical device interoperability market is segmented as follows:

By Industry Participants

- Clinical IT System Vendors

- Healthcare System Integrators

- Vendor-Agnostic Connectivity Vendors

- Medical Device OEMs

By End-User

- Hospitals

- Ambulatory Cares

- Clinics & Imaging Centres

By Application

- Acute Care Settings

- Patient Data Repositories

- Remote Patient Monitoring

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Who are the leading players functioning in the global medical device interoperability market growth?

Table Of Content

CHAPTER 1. Executive Summary 26 CHAPTER 2. Medical Device Interoperability market – Device Type Analysis 28 2.1. Global Medical Device Interoperability Market – Device Type Overview 28 2.2. Global Medical Device Interoperability Market Share, by Device Type, 2018 & 2025 (USD Million) 28 2.3. Monitoring Devices 30 2.3.1. Global Monitoring Devices Medical Device Interoperability Market, 2016-2026 (USD Million) 30 2.4. Imaging Devices and Information Systems 31 2.4.1. Global Imaging Devices and Information Systems Medical Device Interoperability Market, 2016-2026 (USD Million) 31 2.5. Diagnostic Devices 32 2.5.1. Global Diagnostic Devices Medical Device Interoperability Market, 2016-2026 (USD Million) 32 2.6. Surgical Devices 33 2.6.1. Global Surgical Devices Medical Device Interoperability Market, 2016-2026 (USD Million) 33 2.7. Therapeutic Devices 34 2.7.1. Global Therapeutic Devices Medical Device Interoperability Market, 2016-2026 (USD Million) 34 CHAPTER 3. Medical Device Interoperability market – Application Analysis 34 3.1. Global Medical Device Interoperability Market – Application Overview 34 3.2. Global Medical Device Interoperability Market Share, by Application, 2018 & 2025 (USD Million) 35 3.3. Acute Care Settings 36 3.3.1. Global Acute Care Settings Medical Device Interoperability Market, 2016-2026 (USD Million) 36 3.4. Remote Patient Monitoring 37 3.4.1. Global Remote Patient Monitoring Medical Device Interoperability Market, 2016-2026 (USD Million) 37 3.5. Patient Data Repositories 38 3.5.1. Global Patient Data Repositories Medical Device Interoperability Market, 2016-2026 (USD Million) 38 CHAPTER 4. Medical Device Interoperability market – Industry Participant Analysis 38 4.1. Global Medical Device Interoperability Market – Industry Participant Overview 38 4.2. Global Medical Device Interoperability Market Share, by Industry Participant, 2018 & 2025 (USD Million) 39 4.3. Clinical IT System Vendors 40 4.3.1. Global Clinical IT System Vendors Medical Device Interoperability Market, 2016-2026 (USD Million) 40 4.4. Medical Device OEMs 41 4.4.1. Global Medical Device OEMs Medical Device Interoperability Market, 2016-2026 (USD Million) 41 4.5. Vendor-Agnostic Connectivity Vendors 42 4.5.1. Global Vendor-Agnostic Connectivity Vendors Medical Device Interoperability Market, 2016-2026 (USD Million) 42 4.6. Healthcare System Integrators 43 4.6.1. Global Healthcare System Integrators Medical Device Interoperability Market, 2016-2026 (USD Million) 43 CHAPTER 5. Medical Device Interoperability market – End User Analysis 43 5.1. Global Medical Device Interoperability Market – End User Overview 43 5.2. Global Medical Device Interoperability Market Share, by End User, 2018 & 2025 (USD Million) 44 5.3. Hospitals 45 5.3.1. Global Hospitals Medical Device Interoperability Market, 2016-2026 (USD Million) 45 5.4. Clinics and Imaging Centers 46 5.4.1. Global Clinics and Imaging Centers Medical Device Interoperability Market, 2016-2026 (USD Million) 46 5.5. Ambulatory Cares 47 5.5.1. Global Ambulatory Cares Medical Device Interoperability Market, 2016-2026 (USD Million) 47 CHAPTER 6. Medical Device Interoperability market – Regional Analysis 48 6.1. Global Medical Device Interoperability Market Regional Overview 48 6.2. Global Medical Device Interoperability Market Share, by Region, 2018 & 2025 (Value) 48 6.3. North America 50 6.3.1. North America Medical Device Interoperability Market size and forecast, 2016-2026 50 6.3.2. North America Medical Device Interoperability Market, by Country, 2018 & 2025 (USD Million) 50 6.3.3. North America Medical Device Interoperability Market, by Device Type, 2016-2026 52 6.3.3.1. North America Medical Device Interoperability Market, by Device Type, 2016-2026 (USD Million) 52 6.3.4. North America Medical Device Interoperability Market, by Application, 2016-2026 53 6.3.4.1. North America Medical Device Interoperability Market, by Application, 2016-2026 (USD Million) 53 6.3.5. North America Medical Device Interoperability Market, by Industry Participant, 2016-2026 54 6.3.5.1. North America Medical Device Interoperability Market, by Industry Participant, 2016-2026 (USD Million) 54 6.3.6. North America Medical Device Interoperability Market, by End User, 2016-2026 55 6.3.6.1. North America Medical Device Interoperability Market, by End User, 2016-2026 (USD Million) 55 6.3.7. U.S. 56 6.3.7.1. U.S. Market size and forecast, 2016-2026 (USD Million) 56 6.3.8. Canada 57 6.3.8.1. Canada Market size and forecast, 2016-2026 (USD Million) 57 6.4. Europe 58 6.4.1. Europe Medical Device Interoperability Market size and forecast, 2016-2026 58 6.4.2. Europe Medical Device Interoperability Market, by Country, 2018 & 2025 (USD Million) 58 6.4.3. Europe Medical Device Interoperability Market, by Device Type, 2016-2026 60 6.4.3.1. Europe Medical Device Interoperability Market, by Device Type, 2016-2026 (USD Million) 60 6.4.4. Europe Medical Device Interoperability Market, by Application, 2016-2026 61 6.4.4.1. Europe Medical Device Interoperability Market, by Application, 2016-2026 (USD Million) 61 6.4.5. Europe Medical Device Interoperability Market, by Industry Participant, 2016-2026 62 6.4.5.1. Europe Medical Device Interoperability Market, by Industry Participant, 2016-2026 (USD Million) 62 6.4.6. Europe Medical Device Interoperability Market, by End User, 2016-2026 63 6.4.6.1. Europe Medical Device Interoperability Market, by End User, 2016-2026 (USD Million) 63 6.4.7. Germany 64 6.4.7.1. Germany Market size and forecast, 2016-2026 (USD Million) 64 6.4.8. France 65 6.4.8.1. France Market size and forecast, 2016-2026 (USD Million) 65 6.4.9. U.K. 66 6.4.9.1. U.K. Market size and forecast, 2016-2026 (USD Million) 66 6.4.10. Italy 67 6.4.10.1. Italy Market size and forecast, 2016-2026 (USD Million) 67 6.4.11. Spain 68 6.4.11.1. Spain Market size and forecast, 2016-2026 (USD Million) 68 6.4.12. Rest of Europe 69 6.4.12.1. Rest of Europe Market size and forecast, 2016-2026 (USD Million) 69 6.5. Asia Pacific 70 6.5.1. Asia Pacific Medical Device Interoperability Market size and forecast, 2016-2026 70 6.5.2. Asia Pacific Medical Device Interoperability Market, by Country, 2018 & 2025 (USD Million) 70 6.5.3. Asia Pacific Medical Device Interoperability Market, by Device Type, 2016-2026 72 6.5.3.1. Asia Pacific Medical Device Interoperability Market, by Device Type, 2016-2026 (USD Million) 72 6.5.4. Asia Pacific Medical Device Interoperability Market, by Application, 2016-2026 73 6.5.4.1. Asia Pacific Medical Device Interoperability Market, by Application, 2016-2026 (USD Million) 73 6.5.5. Asia Pacific Medical Device Interoperability Market, by Industry Participant, 2016-2026 74 6.5.5.1. Asia Pacific Medical Device Interoperability Market, by Industry Participant, 2016-2026 (USD Million) 74 6.5.6. Asia Pacific Medical Device Interoperability Market, by End User, 2016-2026 75 6.5.6.1. Asia Pacific Medical Device Interoperability Market, by End User, 2016-2026 (USD Million) 75 6.5.7. China 76 6.5.7.1. China Market size and forecast, 2016-2026 (USD Million) 76 6.5.8. Japan 77 6.5.8.1. Japan Market size and forecast, 2016-2026 (USD Million) 77 6.5.9. India 78 6.5.9.1. India Market size and forecast, 2016-2026 (USD Million) 78 6.5.10. South Korea 79 6.5.10.1. South Korea Market size and forecast, 2016-2026 (USD Million) 79 6.5.11. South-East Asia 80 6.5.11.1. South-East Asia Market size and forecast, 2016-2026 (USD Million) 80 6.5.12. Rest of Asia Pacific 81 6.5.12.1. Rest of Asia Pacific Market size and forecast, 2016-2026 (USD Million) 81 6.6. Latin America 82 6.6.1. Latin America Medical Device Interoperability Market size and forecast, 2016-2026 82 6.6.2. Latin America Medical Device Interoperability Market, by Country, 2018 & 2025 (USD Million) 82 6.6.3. Latin America Medical Device Interoperability Market, by Device Type, 2016-2026 84 6.6.3.1. Latin America Medical Device Interoperability Market, by Device Type, 2016-2026 (USD Million) 84 6.6.4. Latin America Medical Device Interoperability Market, by Application, 2016-2026 85 6.6.4.1. Latin America Medical Device Interoperability Market, by Application, 2016-2026 (USD Million) 85 6.6.5. Latin America Medical Device Interoperability Market, by Industry Participant, 2016-2026 86 6.6.5.1. Latin America Medical Device Interoperability Market, by Industry Participant, 2016-2026 (USD Million) 86 6.6.6. Latin America Medical Device Interoperability Market, by End User, 2016-2026 87 6.6.6.1. Latin America Medical Device Interoperability Market, by End User, 2016-2026 (USD Million) 87 6.6.7. Brazil 88 6.6.7.1. Brazil Market size and forecast, 2016-2026 (USD Million) 88 6.6.8. Mexico 89 6.6.8.1. Mexico Market size and forecast, 2016-2026 (USD Million) 89 6.6.9. Rest of Latin America 90 6.6.9.1. Rest of Latin America Market size and forecast, 2016-2026 (USD Million) 90 6.7. The Middle-East and Africa 91 6.7.1. The Middle-East and Africa Medical Device Interoperability Market size and forecast, 2016-2026 91 6.7.2. The Middle-East and Africa Medical Device Interoperability Market, by Country, 2018 & 2025 (USD Million) 91 6.7.3. The Middle-East and Africa Medical Device Interoperability Market, by Device Type, 2016-2026 93 6.7.3.1. The Middle-East and Africa Medical Device Interoperability Market, by Device Type, 2016-2026 (USD Million) 93 6.7.4. The Middle-East and Africa Medical Device Interoperability Market, by Application, 2016-2026 94 6.7.4.1. The Middle-East and Africa Medical Device Interoperability Market, by Application, 2016-2026 (USD Million) 94 6.7.5. The Middle-East and Africa Medical Device Interoperability Market, by Industry Participant, 2016-2026 95 6.7.5.1. The Middle-East and Africa Medical Device Interoperability Market, by Industry Participant, 2016-2026 (USD Million) 95 6.7.6. The Middle-East and Africa Medical Device Interoperability Market, by End User, 2016-2026 96 6.7.6.1. The Middle-East and Africa Medical Device Interoperability Market, by End User, 2016-2026 (USD Million) 96 6.7.7. GCC Countries 97 6.7.7.1. GCC Countries Market size and forecast, 2016-2026 (USD Million) 97 6.7.8. South Africa 98 6.7.8.1. South Africa Market size and forecast, 2016-2026 (USD Million) 98 6.7.9. Rest of Middle-East Africa 99 6.7.9.1. Rest of Middle-East Africa Market size and forecast, 2016-2026 (USD Million) 99 CHAPTER 7. Medical Device Interoperability market – Competitive Landscape 100 7.1. Competitor Market Share – Revenue 100 7.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 102 7.3. Strategic Development 103 7.3.1. Acquisitions and Mergers 103 7.3.2. New Products 103 7.3.3. Research & Development Activities 103 CHAPTER 8. Company Profiles 104 8.1. NantHealth Inc. 104 8.1.1. Company Overview 104 8.1.2. NantHealth Inc. Revenue and Gross Margin 104 8.1.3. Product portfolio 105 8.1.4. Recent initiatives 106 8.2. Abbott 106 8.2.1. Company Overview 106 8.2.2. Abbott Revenue and Gross Margin 106 8.2.3. Product portfolio 107 8.2.4. Recent initiatives 108 8.3. Bernoulli 108 8.3.1. Company Overview 108 8.3.2. Bernoulli Revenue and Gross Margin 108 8.3.3. Product portfolio 109 8.3.4. Recent initiatives 110 8.4. Boston Scientific Corporation 110 8.4.1. Company Overview 110 8.4.2. Boston Scientific Corporation Revenue and Gross Margin 110 8.4.3. Product portfolio 111 8.4.4. Recent initiatives 112 8.5. Cerner Corporation 112 8.5.1. Company Overview 112 8.5.2. Cerner Corporation Revenue and Gross Margin 112 8.5.3. Product portfolio 113 8.5.4. Recent initiatives 114 8.6. Drägerwerk AG & Co. KGaA 114 8.6.1. Company Overview 114 8.6.2. Drägerwerk AG & Co. KGaA Revenue and Gross Margin 114 8.6.3. Product portfolio 115 8.6.4. Recent initiatives 116 8.7. FUKUDA DENSHI 116 8.7.1. Company Overview 116 8.7.2. FUKUDA DENSHI Revenue and Gross Margin 116 8.7.3. Product portfolio 117 8.7.4. Recent initiatives 118 8.8. GENERAL ELECTRIC COMPANY 118 8.8.1. Company Overview 118 8.8.2. GENERAL ELECTRIC COMPANY Revenue and Gross Margin 118 8.8.3. Product portfolio 119 8.8.4. Recent initiatives 120 8.9. iHealth Labs Inc. 120 8.9.1. Company Overview 120 8.9.2. iHealth Labs Inc. Revenue and Gross Margin 120 8.9.3. Product portfolio 121 8.9.4. Recent initiatives 122 8.10. Infosys Limited 122 8.10.1. Company Overview 122 8.10.2. Infosys Limited Revenue and Gross Margin 122 8.10.3. Product portfolio 123 8.10.4. Recent initiatives 124 8.11. Invivo Corporation 124 8.11.1. Company Overview 124 8.11.2. Invivo Corporation Revenue and Gross Margin 124 8.11.3. Product portfolio 125 8.11.4. Recent initiatives 126 8.12. Koninklijke Philips N.V. 126 8.12.1. Company Overview 126 8.12.2. Koninklijke Philips N.V. Revenue and Gross Margin 126 8.12.3. Product portfolio 127 8.12.4. Recent initiatives 128 8.13. Masimo 128 8.13.1. Company Overview 128 8.13.2. Masimo Revenue and Gross Margin 128 8.13.3. Product portfolio 129 8.13.4. Recent initiatives 130 8.14. Medtronic 130 8.14.1. Company Overview 130 8.14.2. Medtronic Revenue and Gross Margin 130 8.14.3. Product portfolio 131 8.14.4. Recent initiatives 132 8.15. Nihon Kohden Corporation 132 8.15.1. Company Overview 132 8.15.2. Nihon Kohden Corporation Revenue and Gross Margin 132 8.15.3. Product portfolio 133 8.15.4. Recent initiatives 134 8.16. Qualcomm Life Inc. 134 8.16.1. Company Overview 134 8.16.2. Qualcomm Life Inc. Revenue and Gross Margin 134 8.16.3. Product portfolio 135 8.16.4. Recent initiatives 136 8.17. Siemens Healthcare Private Limited 136 8.17.1. Company Overview 136 8.17.2. Siemens Healthcare Private Limited Revenue and Gross Margin 136 8.17.3. Product portfolio 137 8.17.4. Recent initiatives 138 8.18. Spacelabs Healthcare 138 8.18.1. Company Overview 138 8.18.2. Spacelabs Healthcare Revenue and Gross Margin 138 8.18.3. Product portfolio 139 8.18.4. Recent initiatives 140 8.19. True Process 140 8.19.1. Company Overview 140 8.19.2. True Process Revenue and Gross Margin 140 8.19.3. Product portfolio 141 8.19.4. Recent initiatives 142 CHAPTER 9. Medical Device Interoperability — Industry Analysis 143 9.1. Medical Device Interoperability Market – Key Trends 143 9.1.1. Market Drivers 144 9.1.2. Market Restraints 144 9.1.3. Market Opportunities 145 9.2. Value Chain Analysis 146 9.3. Technology Roadmap and Timeline 147 9.4. Medical Device Interoperability Market – Attractiveness Analysis 148 9.4.1. By Device Type 148 9.4.2. By Application 148 9.4.3. By Industry Participant 149 9.4.4. By End User 150 9.4.5. By Region 151 CHAPTER 10. Marketing Strategy Analysis, Distributors 152 10.1. Marketing Channel 152 10.2. Direct Marketing 153 10.3. Indirect Marketing 153 10.4. Marketing Channel Development Trend 153 10.5. Economic/Political Environmental Change 154 CHAPTER 11. Report Conclusion 155 CHAPTER 12. Research Approach & Methodology 156 12.1. Report Description 156 12.2. Research Scope 157 12.3. Research Methodology 157 12.3.1. Secondary Research 158 12.3.2. Primary Research 159 12.3.3. Models 160 12.3.3.1. Company Share Analysis Model 160 12.3.3.2. Revenue Based Modeling 161 12.3.3.3. Research Limitations 161

Inquiry For Buying

Medical Device Interoperability

Request Sample

Medical Device Interoperability