Petrochemical Market Size, Share, and Trends Analysis Report

CAGR :

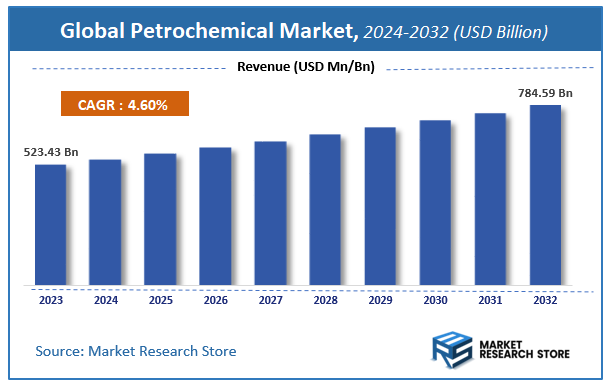

| Market Size 2023 (Base Year) | USD 523.43 Billion |

| Market Size 2032 (Forecast Year) | USD 784.59 Billion |

| CAGR | 4.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Petrochemical Market Insights

According to Market Research Store, the global petrochemical market size was valued at around USD 523.43 billion in 2023 and is estimated to reach USD 784.59 billion by 2032, to register a CAGR of approximately 4.6% in terms of revenue during the forecast period 2024-2032.

The petrochemical report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

According to Market Research Store, the global petrochemical market size was valued at around USD 523.43 billion in 2023 and is estimated to reach USD 784.59 billion by 2032, to register a CAGR of approximately 4.6% in terms of revenue during the forecast period 2024-2032.

The petrochemical report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Petrochemical Market: Overview

Petrochemicals are a category of chemical compounds derived primarily from petroleum and natural gas, serving as the foundational building blocks for a wide array of industrial and consumer products. These chemicals are typically produced through processes such as steam cracking and catalytic reforming in refineries or chemical plants. The most common base petrochemicals include ethylene, propylene, benzene, toluene, xylene, methanol, and butadiene, which are further processed into plastics, synthetic rubber, fibers, detergents, solvents, adhesives, and countless other materials used in packaging, construction, automotive, electronics, and textiles.

The growth of the petrochemical industry is driven by expanding demand for plastic products, urbanization, industrial development, and the proliferation of lightweight and durable synthetic materials. Innovations in chemical engineering, along with shale gas discoveries and advancements in feedstock flexibility, have improved production efficiency and cost competitiveness.

Key Highlights

- The petrochemical market is anticipated to grow at a CAGR of 4.6% during the forecast period.

- The global petrochemical market was estimated to be worth approximately USD 523.43 billion in 2023 and is projected to reach a value of USD 784.59 billion by 2032.

- The growth of the petrochemical market is being driven by the surging demand from a wide array of downstream industries, including packaging, automotive, construction.

- Based on the type, the ethylene segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the polymers segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Petrochemical Market: Dynamics

Key Growth Drivers:

- Growing Demand for Plastics and Packaging: The rapid increase in demand for plastics across various end-use industries, particularly packaging (food, consumer goods, e-commerce), automotive, construction, and electronics, is the most significant driver. Petrochemicals like polyethylene, polypropylene, and PVC are essential for producing these plastics.

- Expansion of the Automotive Industry: Petrochemicals are vital for manufacturing numerous automotive components, including lightweight plastics for vehicle bodies, synthetic rubbers for tires, and various fluids and coatings. The growth in vehicle production, especially electric vehicles (EVs) which also use specialized polymers, fuels demand.

- Rising Consumption in Construction and Infrastructure: Petrochemicals are extensively used in the construction sector for pipes (PVC), insulation materials (polystyrene, polyurethane), paints and coatings, adhesives, and various synthetic fibers. Global urbanization and infrastructure development projects drive this demand.

Restraints:

- Volatility of Crude Oil and Natural Gas Prices: Petrochemical production is highly dependent on crude oil and natural gas as feedstocks. Fluctuations in the prices of these commodities directly impact the production costs of petrochemicals, leading to price instability and affecting profit margins for manufacturers.

- Stringent Environmental Regulations and Sustainability Pressure: The petrochemical industry faces intense scrutiny and increasingly stringent environmental regulations concerning greenhouse gas emissions, waste management, and pollution. Compliance with these regulations often requires significant capital investment and can increase operational costs.

- Shift Towards Renewable Energy and Decarbonization: The global push towards renewable energy sources and decarbonization efforts poses a long-term threat to the traditional petrochemical industry, as it relies on fossil fuels. This shift could lead to decreased demand for traditional feedstocks in the distant future.

Opportunities:

- Growing Investment in Bio-based Petrochemicals: Significant opportunities exist in the research, development, and commercialization of petrochemicals derived from biomass (e.g., bio-ethylene, bio-propylene). This aligns with sustainability goals and reduces reliance on fossil feedstocks.

- Chemical Recycling and Advanced Recycling Technologies: Developing and scaling up advanced chemical recycling technologies that can convert plastic waste back into virgin-quality feedstocks for petrochemical production presents a massive opportunity for a circular economy and sustainable growth.

- Focus on High-Value Specialty Chemicals: Shifting focus from commodity petrochemicals to higher-value specialty chemicals, which command better profit margins and cater to niche applications (e.g., advanced polymers for electronics, medical-grade plastics), offers strategic growth.

- Carbon Capture, Utilization, and Storage (CCUS): Implementing CCUS technologies to capture CO2 emissions from petrochemical plants and either store them or convert them into useful products (e.g., new chemicals) can significantly improve the industry's environmental footprint and create new revenue streams.

Challenges:

- Achieving Sustainability and Decarbonization Goals: The most significant long-term challenge is for the petrochemical industry to transition towards a more sustainable and low-carbon future, reducing its reliance on fossil fuels, cutting emissions, and addressing plastic waste concerns. This requires massive investment and technological breakthroughs.

- Managing Public Perception and "Plastic Phobia": The industry faces a significant challenge in managing negative public perception surrounding plastics and their environmental impact. Educating consumers and demonstrating tangible commitments to sustainability and circularity are crucial.

- Intense Competition and Oversupply in Key Regions: The market, especially for commodity petrochemicals, often faces challenges of oversupply, particularly from new capacities coming online in regions with abundant and cheap feedstock (e.g., Middle East, US shale gas). This can lead to downward pressure on prices and margins.

Petrochemical Market: Report Scope

This report thoroughly analyzes the Petrochemical Market exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Petrochemical Market |

| Market Size in 2023 | USD 523.43 Billion |

| Market Forecast in 2032 | USD 784.59 Billion |

| Growth Rate | CAGR of 4.6% |

| Number of Pages | 140 |

| Key Companies Covered | BASF SE, ExxonMobil, The Dow Chemical Company, Shell Chemical Company, SABIC, Sinopec Limited, LyondellBasell Industries, Total S.A., Sumitomo Chemical Co. Ltd., Chevron Phillips Chemical Company LLC and E. I. du Pont de Nemours and Company |

| Segments Covered | By Product Type, By Manufacturing Processes, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Petrochemical Market: Segmentation Insights

The global petrochemical market is divided by type, application, and region.

Based on type, the global petrochemical market is divided into ethylene, propylene, butadiene, benzene, toluene, xylene, and methanol. Ethylene is the dominant type in the global petrochemical market, accounting for the largest share due to its extensive use as a key building block in the production of a wide range of products such as polyethylene, ethylene oxide, ethylene dichloride, and styrene. It plays a central role in industries such as packaging, construction, automotive, and textiles. The massive global demand for polyethylene, particularly for plastic packaging and film applications, directly drives ethylene consumption. Ethylene is produced primarily through steam cracking of hydrocarbons like naphtha and ethane.

On the basis of application, the global petrochemical market is bifurcated into polymers, paints and coatings, solvents, rubber, adhesives and sealants, surfactants, dyes, and other. Polymers are the dominant application segment in the petrochemical market, accounting for the highest consumption of base chemicals like ethylene, propylene, and benzene. Petrochemical-derived polymers such as polyethylene, polypropylene, polystyrene, and PET are essential materials used in packaging, automotive parts, textiles, construction materials, and consumer goods. The demand is primarily fueled by the rapid expansion of the packaging industry especially flexible packaging and increased use of lightweight plastics in the automotive and electronics sectors.

Petrochemical Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the global petrochemical market, driven by abundant shale gas reserves, advanced refining infrastructure, and competitive feedstock pricing. The United States, in particular, leads in the production of key petrochemicals such as ethylene, propylene, methanol, and benzene, supported by massive investments in ethane-based steam crackers. The shale gas boom has significantly lowered feedstock costs, enabling North American producers to export competitively to Asia and Europe. Major companies like ExxonMobil, Dow, Chevron Phillips Chemical, and LyondellBasell operate large-scale integrated facilities with downstream capabilities, giving the region an edge in both cost efficiency and product diversification. The petrochemical industry also benefits from robust logistics, pipeline networks, and proximity to export terminals on the Gulf Coast. With continued investment in expansion projects and sustainability initiatives, such as carbon capture and bio-based derivatives, North America remains the global leader in petrochemical production and innovation.

Europe holds a mature but constrained position in the petrochemical market, with key contributors including Germany, the Netherlands, France, and Belgium. The region’s petrochemical output is largely naphtha-based due to limited access to low-cost natural gas, making operations more sensitive to global crude oil price fluctuations. Europe is known for high-quality specialty petrochemicals, with a strong focus on value-added derivatives used in automotive, electronics, and pharmaceutical industries. Environmental regulations under REACH and the EU Green Deal have prompted producers to improve energy efficiency, reduce emissions, and invest in circular economy strategies. Recycling and the development of bio-based feedstocks are gaining importance, especially in Western Europe. While capacity expansion is limited compared to Asia or North America, innovation in sustainable chemicals and advanced polymers remains a regional strength.

Asia-Pacific is the fastest-growing region in the petrochemical market, with China, India, Japan, and South Korea leading both consumption and production. China is the largest petrochemical consumer and increasingly a major producer, with extensive investments in coal-to-olefins (CTO), methanol-to-olefins (MTO), and large refining-chemical integration projects. India is expanding its domestic petrochemical infrastructure with strategic projects such as PCPIR (Petroleum, Chemicals and Petrochemicals Investment Regions), aiming to reduce import dependence. Japan and South Korea focus on high-value petrochemicals for electronics, automotive, and specialty industries. Despite the region's rapid growth, it faces challenges including environmental regulations, volatile feedstock supply, and geopolitical trade tensions. Integration of refining and chemical operations is a growing trend in Asia-Pacific to improve margins and ensure feedstock security. While the region is poised to overtake other markets in volume, North America retains dominance due to superior feedstock economics and integration.

Latin America has a moderate but developing petrochemical market, with Brazil, Mexico, and Argentina as key players. Brazil’s petrochemical sector is supported by domestic oil production and a growing manufacturing base. Mexico’s proximity to the U.S. and its participation in trade agreements like USMCA position it as a strategic export hub for North American companies. Local demand for plastics, fertilizers, and synthetic fibers drives regional consumption, though aging infrastructure and limited new investments restrict production capacity growth. Reliance on imported feedstocks, high operational costs, and political uncertainties hinder long-term competitiveness. However, new refinery-petrochemical integration plans in Brazil and expansion of plastic recycling initiatives are expected to improve the market's outlook.

Middle East & Africa holds a significant and strategically important position in the global petrochemical market, particularly in Saudi Arabia, the UAE, Iran, and Qatar. The region’s access to low-cost natural gas feedstocks, especially ethane, supports the production of competitively priced basic petrochemicals such as ethylene, polyethylene, and methanol. Saudi Arabia’s SABIC and other regional giants are heavily investing in downstream diversification, integrated facilities, and sustainability-focused initiatives, including green hydrogen and CO₂ utilization. The UAE is expanding its chemical production through projects like Borouge, while Iran remains a key regional supplier despite facing international sanctions. Africa, led by South Africa, Nigeria, and Egypt, represents an emerging market with increasing investment in refining and petrochemical capacity. However, the region continues to face challenges related to infrastructure, feedstock security, and regulatory stability. The Middle East remains a key global exporter, particularly to Asia, but lacks the downstream integration and market diversity found in North America.

Petrochemical Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the petrochemical market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global petrochemical market include:

- BASF SE

- Chevron Corporation

- China National Petroleum Corporation (CNPC)

- China Petrochemical Corporation

- ExxonMobil Corporation

- INEOS Group Ltd.

- LyondellBasell Industries Holdings B.V.

- Royal Dutch Shell PLC

- SABIC

- Dow

- TOTAL

- Indian Oil Corporation Limited

- BP PLC

- Sumitomo Chemical Company

- Reliance Industries Limited

- DowDuPont

The global petrochemical market is segmented as follows:

By Type

- Ethylene

- Propylene

- Butadiene

- Benzene

- Toluene

- Xylene

- Methanol

By Application

- Polymers

- Paints and Coatings

- Solvents

- Rubber

- Adhesives and Sealants

- Surfactants

- Dyes

- Other

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

- Chapter 1. Introduction

- 1.1. Report description and scope

- 1.2. Research scope

- 1.3. Research methodology

- 1.3.1. Market research process

- 1.3.2. Market research methodology

- Chapter 2. Executive Summary

- 2.1. Global market volume and revenue, 2014 - 2020 (Million Tons) (USD Billion)

- 2.2. Global petrochemicals market: Snapshot

- Chapter 3. Petrochemicals Market – Global and Industry Analysis

- 3.1. Petrochemical: Market dynamics

- 3.2. Value chain analysis

- 3.3. Market drivers

- 3.3.1. Drivers for global petrochemicals market: Impact analysis

- 3.3.2. Growth in demand for petrochemicals products

- 3.3.3. Growing demand from end-use industries and government support in Asia Pacific

- 3.3.4. Government support in Asia Pacific

- 3.3.5. Abundant availability of raw materials in the Middle East

- 3.4. Market restraints

- 3.4.1. Shift towards developing bio-based chemicals

- 3.4.2. Increasing environmental issues

- 3.5. Opportunities

- 3.5.1. Emergence of coal and shale gas as key feedstock for petrochemicals production

- 3.6. Porter’s five forces analysis

- 3.7. Market attractiveness analysis

- 3.7.1. Global petrochemicals market attractiveness, by product type

- 3.7.2. Market attractiveness analysis, by regional segment

- Chapter 4. Global Petrochemicals Market - Competitive Landscape

- 4.1. Company market share

- 4.2. Production capacity (Subject to data availability)

- 4.3. Raw material analysis

- 4.4. Price analysis

- Chapter 5. Global Petrochemicals Market – Product Segment Analysis

- 5.1. Global petrochemicals market: Product overview

- 5.1.1. Global petrochemicals market volume share by application, 2014 and 2020

- 5.2. Ethylene

- 5.2.1. Global ethylene market volume, by region, 2014 – 2020 (Million Tons)

- 5.2.2. Global ethylene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.2.3. Global ethylene market volume, by application, 2014 – 2020 (Million Tons)

- 5.2.4. Global ethylene market revenue, by application, 2014 – 2020 (USD Billion)

- 5.3. Propylene

- 5.3.1. Global propylene market volume, by region, 2014 – 2020 (Million Tons)

- 5.3.2. Global propylene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.3.3. Global propylene market volume, by application, 2014 – 2020 (Million Tons)

- 5.3.4. Global propylene market revenue, by application, 2014 – 2020 (USD Billion))

- 5.4. Butadiene

- 5.4.1. Global butadiene market volume, by region, 2014 – 2020 (Million Tons)

- 5.4.2. Global butadiene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.4.3. Global butadiene market volume, by application, 2014 – 2020 (Million Tons)

- 5.4.4. Global butadiene market revenue, by application, 2014 – 2020 (USD Billion)

- 5.5. Benzene

- 5.5.1. Global benzene market volume, by region, 2014 – 2020 (Million Tons)

- 5.5.2. Global benzene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.5.3. Global benzene market volume, by application, 2014 – 2020 (Million Tons)

- 5.5.4. Global benzene market revenue, by application, 2014 – 2020 (USD Billion)

- 5.6. Xylene

- 5.6.1. Global xylene market volume, by region, 2014 – 2020 (Million Tons)

- 5.6.2. Global xylene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.7. Toluene

- 5.7.1. Global toluene market volume, by region, 2014 – 2020 (Million Tons)

- 5.7.2. Global toluene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.7.3. Global toluene market volume, by application, 2014 – 2020 (Million Tons)

- 5.7.4. Global toluene market revenue, by application, 2014 – 2020 (USD Billion)

- 5.8. Vinyl

- 5.8.1. Global vinyl market volume, by region, 2014 – 2020 (Million Tons)

- 5.8.2. Global vinyl market revenue, by region, 2014 – 2020 (USD Billion)

- 5.9. Styrene

- 5.9.1. Global styrene market volume, by region, 2014 – 2020 (Million Tons)

- 5.9.2. Global styrene market revenue, by region, 2014 – 2020 (USD Billion)

- 5.9.3. Global styrene market volume, by application, 2014 – 2020 (Million Tons)

- 5.9.4. Global styrene market revenue, by application, 2014 – 2020 (USD Billion)

- 5.10. Methanol

- 5.10.1. Global methanol market volume, by region, 2014 – 2020 (Million Tons)

- 5.10.2. Global methanol market revenue, by region, 2014 – 2020 (USD Billion)

- 5.10.3. Global methanol market volume, by application, 2014 – 2020 (Million Tons)

- 5.10.4. Global methanol market revenue, by application, 2014 – 2020 (USD Billion)

- 5.1. Global petrochemicals market: Product overview

- Chapter 6. Global petrochemicals market – Regional segment analysis

- 6.1. Global petrochemicals market: Regional overview

- 6.1.1. Global petrochemicals market volume share by region, 2014 and 2020

- 6.2. North America

- 6.2.1. U.S. petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.3. Europe

- 6.3.1. Germany petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.3.2. France petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.3.3. UK petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.4. Asia Pacific

- 6.4.1. China petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.4.2. Japan petrochemicals market, 2014 - 2020 (Million Tons) (USD Billion)

- 6.4.3. India petrochemicals market, 2014 - 2020 (Million Tons) (USD Billion)

- 6.5. Middle East and Africa

- 6.5.1. Middle East and Africa petrochemicals market, 2014 – 2020 (Million Tons) (USD Billion)

- 6.1. Global petrochemicals market: Regional overview

- Chapter 7. Company Profile

- 7.1. BASF SE

- 7.1.1. Overview

- 7.1.2. Financials

- 7.1.3. Product Portfolio

- 7.1.4. Business Strategy

- 7.1.5. Recent Developments

- 7.2. The Dow Chemical Company

- 7.2.1. Overview

- 7.2.2. Financials

- 7.2.3. Product Portfolio

- 7.2.4. Business Strategy

- 7.2.5. Recent Developments

- 7.3. Qingdao Huadong Calcium Producing Co. Ltd.

- 7.3.1. Overview

- 7.3.2. Financials

- 7.3.3. Product Portfolio

- 7.3.4. Business Strategy

- 7.3.5. Recent Developments

- 7.4. China Petroleum & Chemical Corporation (Sinopec)

- 7.4.1. Overview

- 7.4.2. Financials

- 7.4.3. Product Portfolio

- 7.4.4. Business Strategy

- 7.4.5. Recent Developments

- 7.5. Royal Dutch Shell plc

- 7.5.1. Overview

- 7.5.2. Financials

- 7.5.3. Product Portfolio

- 7.5.4. Business Strategy

- 7.5.5. Recent Developments

- 7.6. Saudi Basic Industries Corporation (SABIC)

- 7.6.1. Overview

- 7.6.2. Financials

- 7.6.3. Product Portfolio

- 7.6.4. Business Strategy

- 7.6.5. Recent Developments

- 7.7. ExxonMobil Corporation

- 7.7.1. Overview

- 7.7.2. Financials

- 7.7.3. Product Portfolio

- 7.7.4. Business Strategy

- 7.7.5. Recent Developments

- 7.8. British Petroleum plc

- 7.8.1. Overview

- 7.8.2. Financials

- 7.8.3. Product Portfolio

- 7.8.4. Business Strategy

- 7.8.5. Recent Developments

- 7.9. Chevron Corporation

- 7.9.1. Overview

- 7.9.2. Financials

- 7.9.3. Product Portfolio

- 7.9.4. Business Strategy

- 7.9.5. Recent Developments

- 7.10. LyondellBasell Industries

- 7.10.1. Overview

- 7.10.2. Financials

- 7.10.3. Product Portfolio

- 7.10.4. Business Strategy

- 7.10.5. Recent Developments

- 7.11. INEOS AG

- 7.11.1. Overview

- 7.11.2. Financials

- 7.11.3. Product Portfolio

- 7.11.4. Business Strategy

- 7.11.5. Recent Developments

- 7.12. China National Petroleum Corporation (CNPC)

- 7.12.1. Overview

- 7.12.2. Financials

- 7.12.3. Product Portfolio

- 7.12.4. Business Strategy

- 7.12.5. Recent Development

Inquiry For Buying

Petrochemical

Request Sample

Petrochemical