Treasury Software Market Size, Share, and Trends Analysis Report

CAGR :

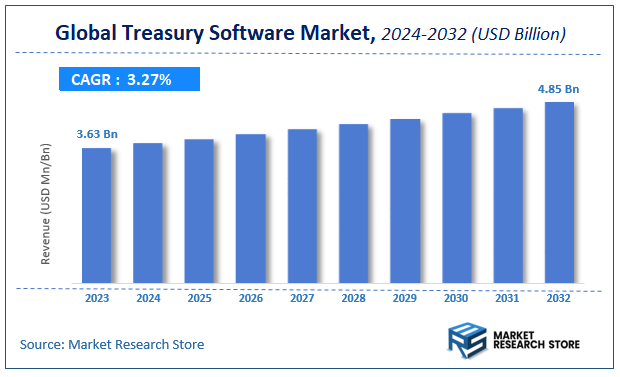

| Market Size 2023 (Base Year) | USD 3.63 Billion |

| Market Size 2032 (Forecast Year) | USD 4.85 Billion |

| CAGR | 3.27% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Treasury Software Market Insights

According to Market Research Store, the global treasury software market size was valued at around USD 3.63 billion in 2023 and is estimated to reach USD 4.85 billion by 2032, to register a CAGR of approximately 3.27% in terms of revenue during the forecast period 2024-2032.

The treasury software report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Treasury Software Market: Overview

Treasury software is a specialized financial management solution designed to help organizations efficiently manage their cash, liquidity, risk, banking transactions, and investment activities. It provides tools for automating and optimizing core treasury functions such as cash forecasting, bank reconciliation, debt and investment tracking, financial risk management (including currency and interest rate risks), and compliance with regulatory and internal reporting requirements. Treasury software systems are often integrated with enterprise resource planning (ERP) platforms to enable real-time visibility into global cash positions and streamline decision-making processes.

The growth of the treasury software market is driven by the increasing complexity of corporate finance operations, rising demand for real-time data analytics, and the need for robust risk mitigation strategies in volatile financial environments. Companies across industries are adopting advanced treasury solutions to improve financial control, ensure regulatory compliance, and enhance operational efficiency. Cloud-based deployment, AI-powered forecasting, and blockchain-enabled transparency are among the key innovations propelling the adoption of modern treasury systems. As global enterprises face growing pressure to optimize liquidity and manage financial risks proactively, treasury software continues to play a critical role in supporting strategic financial planning and enterprise-wide governance.

Key Highlights

- The treasury software market is anticipated to grow at a CAGR of 3.27% during the forecast period.

- The global treasury software market was estimated to be worth approximately USD 3.63 billion in 2023 and is projected to reach a value of USD 4.85 billion by 2032.

- The growth of the treasury software market is being driven by the increasing need for efficient financial risk management, real-time visibility into cash positions, and streamlined treasury operations across organizations.

- On the basis of deployment type, the on-premise solutions segment is projected to swipe the largest market share.

- In terms of functionality, the cash management systems segment is expected to dominate the market.

- Based on the industry, the banking and financial services segment is expected to dominate the market.

- In terms of user type, the treasury managers segment is expected to dominate the market.

- Based on the business size, the small enterprises segment is growing at a high rate and is projected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Treasury Software Market: Dynamics

Key Growth Drivers:

- Growing Demand for Automation and Operational Efficiency: Organizations are under continuous pressure to streamline financial processes, reduce manual errors, and cut operational costs. Treasury software automates routine tasks such as cash reconciliation, payment processing, and reporting, freeing up treasury professionals to focus on more strategic, value-added activities. This push for automation is a primary driver of market growth.

- Increasing Complexity of Global Financial Operations: As businesses expand their operations internationally, they face a multitude of currencies, banking systems, and regulatory environments. Treasury software provides a centralized platform for managing cash flow, liquidity, and risk across multiple banks and subsidiaries, offering real-time visibility and control that is nearly impossible to achieve with manual systems or spreadsheets.

- Need for Enhanced Risk Management and Compliance: In today's volatile financial environment, companies face significant risks from currency fluctuations, interest rate changes, and commodity price variations. Treasury software includes sophisticated risk management modules that help treasurers monitor, analyze, and mitigate these financial risks. Additionally, these systems ensure compliance with a growing number of complex financial regulations, such as the European Markets Infrastructure Regulation (EMIR).

- Shift Towards Cloud-Based and SaaS Solutions: The transition from on-premise to cloud-based and Software-as-a-Service (SaaS) treasury solutions is a major driver. Cloud-based systems offer greater flexibility, scalability, and lower upfront costs, making them more accessible to small and medium-sized enterprises (SMEs) that previously couldn't afford traditional TMS. This has significantly expanded the potential customer base for the market.

Restraints:

- High Implementation Costs and Integration Challenges: The initial cost of implementing a comprehensive treasury software solution, particularly for large enterprises, can be substantial. This includes software licensing, hardware upgrades, and extensive training. Furthermore, integrating a new TMS with a company's existing Enterprise Resource Planning (ERP) systems, banking portals, and other financial software can be a complex, time-consuming, and expensive process.

- Data Security and Privacy Concerns: Treasury software handles some of a company's most sensitive financial data, making it a prime target for cyberattacks. The risk of data breaches, financial fraud, and unauthorized access is a major concern for organizations, particularly those in highly regulated industries like banking and healthcare. Ensuring the security and integrity of this data is a significant restraint on adoption.

- Resistance to Change and Lack of Skilled Professionals: Many organizations, especially those with legacy systems and a long history of manual processes, may be resistant to adopting new technology that fundamentally alters their workflow. There is also a shortage of skilled professionals who are trained to implement, manage, and optimize modern treasury software, which can slow down the adoption and full utilization of these systems.

- Lack of Awareness in Developing Regions: In many developing countries, there is still a lack of awareness about the benefits of treasury software over traditional methods. This, combined with a lower level of technological maturity and smaller IT budgets, can limit the market's growth and lead to a reliance on outdated and inefficient financial management practices.

Opportunities:

- Integration of AI, Machine Learning, and Predictive Analytics: The integration of artificial intelligence (AI) and machine learning (ML) into treasury software presents a major opportunity. AI-powered systems can provide more accurate cash flow forecasting, automate complex risk assessments, and detect fraudulent activities in real time. This move towards predictive analytics will significantly increase the strategic value of TMS.

- Expansion into the Small and Medium-Sized Enterprise (SME) Segment: With the rise of affordable, cloud-based solutions, there is a vast, untapped market for treasury software among SMEs. Platforms that can offer scalable, user-friendly, and cost-effective solutions tailored to the specific needs of smaller businesses can capture a significant new customer base and drive market expansion.

- Leveraging API-Based Connectivity and Open Banking: The shift towards open banking and API (Application Programming Interface) connectivity is a huge opportunity. API-based TMS can provide real-time, bidirectional communication with multiple banks and financial systems, offering a level of data accuracy and speed that was previously unattainable. This enhanced connectivity can help treasurers achieve true real-time visibility and control.

- Development of Specialized and Niche Solutions: The market can expand by developing specialized software for niche industries with unique treasury requirements, such as the energy sector with its complex commodity trading, or the biotechnology industry with its unique cash management needs. By offering tailored solutions, vendors can differentiate themselves in a competitive market.

Challenges:

- Ensuring Data Integrity and Standardization: A key challenge is to ensure the integrity and accuracy of data coming from disparate systems and banks. The lack of a universal standard for data formats and communication protocols makes it difficult to achieve a single, unified view of a company's finances without extensive customization and data normalization efforts.

- Navigating a Fragmented Vendor Landscape: The treasury software market is highly fragmented, with many vendors offering a wide range of solutions. The challenge for buyers is to navigate this complex landscape and find a solution that not only meets their current needs but is also scalable and future-proof. For vendors, the challenge is to differentiate their product in a crowded market.

- Balancing Functionality with User-Friendliness: Treasury software needs to be highly functional and capable of handling complex financial tasks. However, it also needs to be intuitive and easy for end-users to navigate. A key challenge is to design a system that can manage all the necessary complexities while still offering a clean, user-friendly interface that doesn't require extensive training.

- The "Black Box" of Automated Decisions: As AI and ML are integrated into TMS, there is a challenge related to the "black box" problem, where the reasoning behind an automated decision is not transparent. Treasurers need to be able to trust the system and understand how it arrived at a particular forecast or recommendation, which requires a focus on explainable AI and robust validation processes.

Treasury Software Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Treasury Software Market |

| Market Size in 2023 | USD 3.63 Billion |

| Market Forecast in 2032 | USD 4.85 Billion |

| Growth Rate | CAGR of 3.27% |

| Number of Pages | 222 |

| Key Companies Covered | CRM Treasury Systems, DataLog Finance, Financial Sciences Corp., Finastra, Cash Analytics Limited, ION., Gtreasury, FIS, Kyriba Corp., Salmon Software Ltd., TreasuryXpress, Eurobase International, Calypso, BELLIN, Access Systems (UK) Limited, CAPIX, ABM CLOUD, Oracle Corporation, and SAP SE among others |

| Segments Covered | By Deployment Mode, By Organization Size, By Vertical, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Treasury Software Market: Segmentation Insights

The global treasury software market is divided by deployment type, functionality, industry, user type, business size, and region.

On the basis of deployment type, the global treasury software market is bifurcated into on-premise solutions, cloud-based solutions, and hybrid solutions. On-Premise Solutions dominate the Treasury Software Market, particularly among large enterprises and financial institutions that prioritize data security, regulatory compliance, and control over system customization. These solutions are installed locally on the organization’s servers and managed by internal IT teams, offering maximum autonomy over sensitive financial data and integration with legacy systems. On-premise deployments are often favored by organizations operating in highly regulated sectors or regions with strict data residency laws. Although they require higher upfront investment and maintenance, the long-term stability and bespoke configuration options continue to make on-premise treasury systems the preferred choice for enterprises with complex treasury operations.

In terms of functionality, the global treasury software market is bifurcated into cash management systems, risk management tools, forecasting and analytics software, and compliance management solutions. Cash Management Systems dominate the Treasury Software Market due to their critical role in overseeing and optimizing an organization’s liquidity. These systems provide real-time visibility into cash positions across multiple bank accounts and geographies, allowing businesses to efficiently manage working capital, process payments, and reduce idle balances. They also support automated reconciliation, fund transfers, and centralized treasury operations. Large enterprises and multinational corporations particularly rely on robust cash management tools to ensure optimal liquidity and prevent overdrafts or unnecessary borrowing. The increasing need for accurate and immediate cash flow insights across global operations continues to drive strong adoption in this segment.

On the basis of industry, the global treasury software market is bifurcated into banking and financial services, manufacturing, retail, govement and public sector, and healthcare. Banking and Financial Services dominate the Treasury Software Market due to their highly complex financial structures, large-scale cash transactions, and stringent regulatory requirements. These institutions require robust treasury solutions to manage liquidity, conduct interbank transfers, monitor risks, ensure compliance, and support multi-currency operations. Real-time data processing, high-level security features, and integration with core banking systems are essential capabilities in this sector. Treasury software also plays a vital role in optimizing investment portfolios, managing interest rate risk, and generating detailed financial reports for audit and compliance. As digital transformation continues in the financial sector, demand for intelligent, AI-enabled treasury solutions remains strong.

In terms of user type, the global treasury software market is bifurcated into treasury managers, finance departments, compliance officers, risk managers, and IT departments. Treasury Managers are the dominant users in the Treasury Software Market as they are directly responsible for overseeing an organization’s cash flow, liquidity, investments, and financial risk. Treasury managers depend on these solutions for real-time visibility into bank positions, efficient fund transfers, and managing short-term borrowing or surplus investments. The software helps them in making data-driven decisions, handling currency exposures, and ensuring the company maintains optimal working capital. With growing complexity in global finance and increased pressure to drive efficiency, treasury managers prioritize solutions with automation, analytics, and centralized dashboards.

Based on business size, the global treasury software market is divided into small enterprises, medium enterprises, and large enterprises. Large Enterprises dominate the Treasury Software Market due to their complex financial structures, extensive global operations, and higher transaction volumes that necessitate robust and scalable treasury management solutions. These enterprises require advanced features such as cash and liquidity management, risk and compliance monitoring, investment tracking, and real-time reporting across multiple currencies and subsidiaries. Their substantial IT budgets allow for customized solutions, integration with ERP systems, and support for automation and artificial intelligence capabilities. The need to maintain financial visibility and mitigate operational risks on a global scale continues to drive the strong adoption of comprehensive treasury software platforms among large corporations.

Treasury Software Market: Regional Insights

- North America is expected to dominate the global market

North America leads the treasury software market, anchored by its sophisticated financial infrastructure, early adoption of cutting-edge technology, and strong institutional presence among both financial firms and technology vendors. Organizations rely heavily on cloud-based platforms and AI-driven analytics to enhance liquidity management, compliance, and risk mitigation. Industry giants like Oracle, SAP, and Kyriba are deeply entrenched here, offering comprehensive solutions that integrate with enterprise systems. The region’s regulatory environment drives demand for advanced treasury capabilities, and continuous innovation from fintechs and incumbents solidifies North America's stronghold.

Asia-Pacific is the fastest-growing region in the market, driven by rapid digitalization, economic expansion, and diversity in enterprise needs. Countries such as China, India, and Japan are embracing treasury software to support automation, cash visibility, and risk analytics. The SME segment is fueling demand for agile and scalable cloud solutions, and governments are encouraging fintech adoption through financial infrastructure modernization. Regional platforms are diversifying to offer multi-currency capabilities and predictive analytics to meet the growing complexity of cross-border trade and enterprise financial planning.

Europe stands as a robust market for treasury software, characterized by a high level of regulatory complexity and demand for cross-border financial operations. Companies in the UK, Germany, and France increasingly adopt automated treasury solutions to manage multi-currency workflows, comply with frameworks like GDPR and SEPA, and support real-time payments. Digital transformation is a major theme, with increasing adoption of cloud-based systems that deliver data security and integration with enterprise platforms. Treasury solutions in this region often incorporate sustainability features and governance modules to align with evolving corporate responsibility standards.

Latin America is an emerging but increasingly active market for treasury solutions, driven by a growing emphasis on financial modernization and stronger governance. Businesses in Brazil, Mexico, and neighbouring countries are deploying treasury platforms to enhance financial efficiency and manage currency volatility. Implementation follows a progressive trend toward multi-enterprise and regulatory-resilient systems. While adoption is currently more gradual, ongoing reforms and expanding trade activities are elevating demand for robust treasury tools that offer comprehensive visibility and liquidity optimization.

Middle East & Africa, treasury software adoption is nascent but gaining momentum through smart globalization and public sector reforms. Countries like UAE and South Africa are spearheading deployment of treasury systems integrated with ERP tools to improve cash visibility and financial control. Broader economic transformation plans encourage digital financial infrastructure enhancement, and there is growing appreciation for the role of treasury automation in risk management. Although infrastructure constraints and regulatory diversity pose challenges, expanding cross-border trade and investment incentivize increased treasury software usage across the region.

Treasury Software Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the treasury software market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global treasury software market include:

- BankSense

- CAPIX

- SAP

- Financial Sciences

- TreasuryXpress

- Calypso Technology

- Misys

- Broadridge Financial Solutions

- Indus Valley Partners

- Oracle Treasury

- Reval

- Salmon Software

- Kyriba

- Bellin Treasury Services

- Emphasys Software

- FIS

- DataLog Finance

- Visual Risk

- CRM Treasury Systems

- Finastra

- Cash Analytics Limited

- ION.

- Gtreasury

- Eurobase International

- Access Systems (UK) Limited

- ABM CLOUD

The global treasury software market is segmented as follows:

By Deployment Type

- On-Premise Solutions

- Cloud-Based Solutions

- Hybrid Solutions

By Functionality

- Cash Management Systems

- Risk Management Tools

- Forecasting and Analytics Software

- Compliance Management Solutions

By Industry

- Banking and Financial Services

- Manufacturing

- Retail

- Govement and Public Sector

- Healthcare

By User Type

- Treasury Managers

- Finance Departments

- Compliance Officers

- Risk Managers

- IT Departments

By Business Size

- Small Enterprises

- Medium Enterprises

- Large Enterprises

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

CHAPTER 1. Executive Summary 22 CHAPTER 2. Treasury Software market – Deployment Mode Analysis 25 2.1. Global Treasury Software Market – Deployment Mode Overview 25 2.2. Global Treasury Software Market Share, by Deployment Mode, 2018 & 2025 (USD Million) 25 2.3. On-Premise 27 2.3.1. Global On-Premise Treasury Software Market, 2015-2027 (USD Million) 27 2.4. Cloud-Based 28 2.4.1. Global Cloud-Based Treasury Software Market, 2015-2027 (USD Million) 28 CHAPTER 3. Treasury Software market – Organization Size Analysis 28 3.1. Global Treasury Software Market – Organization Size Overview 28 3.2. Global Treasury Software Market Share, by Organization Size, 2018 & 2025 (USD Million) 29 3.3. Small & Medium-Sized Enterprises 30 3.3.1. Global Small & Medium-Sized Enterprises Treasury Software Market, 2015-2027 (USD Million) 30 3.4. Large Enterprises 31 3.4.1. Global Large Enterprises Treasury Software Market, 2015-2027 (USD Million) 31 CHAPTER 4. Treasury Software market – Vertical Analysis 31 4.1. Global Treasury Software Market – Vertical Overview 31 4.2. Global Treasury Software Market Share, by Vertical, 2018 & 2025 (USD Million) 32 4.3. Banking, Financial Services, & Insurance (BFSI) 33 4.3.1. Global Banking, Financial Services, & Insurance (BFSI) Treasury Software Market, 2015-2027 (USD Million) 33 4.4. Healthcare 34 4.4.1. Global Healthcare Treasury Software Market, 2015-2027 (USD Million) 34 4.5. Manufacturing 35 4.5.1. Global Manufacturing Treasury Software Market, 2015-2027 (USD Million) 35 4.6. Consumer Goods 36 4.6.1. Global Consumer Goods Treasury Software Market, 2015-2027 (USD Million) 36 4.7. Chemicals, Metals, & Energy 37 4.7.1. Global Chemicals, Metals, & Energy Treasury Software Market, 2015-2027 (USD Million) 37 CHAPTER 5. Treasury Software market – Regional Analysis 38 5.1. Global Treasury Software Market Regional Overview 38 5.2. Global Treasury Software Market Share, by Region, 2018 & 2025 (Value) 38 5.3. North America 40 5.3.1. North America Treasury Software Market size and forecast, 2015-2027 40 5.3.2. North America Treasury Software Market, by Country, 2018 & 2025 (USD Million) 40 5.3.3. North America Treasury Software Market, by Deployment Mode, 2015-2027 42 5.3.3.1. North America Treasury Software Market, by Deployment Mode, 2015-2027 (USD Million) 42 5.3.4. North America Treasury Software Market, by Organization Size, 2015-2027 43 5.3.4.1. North America Treasury Software Market, by Organization Size, 2015-2027 (USD Million) 43 5.3.5. North America Treasury Software Market, by Vertical, 2015-2027 44 5.3.5.1. North America Treasury Software Market, by Vertical, 2015-2027 (USD Million) 44 5.3.6. U.S. 45 5.3.6.1. U.S. Market size and forecast, 2015-2027 (USD Million) 45 5.3.7. Canada 46 5.3.7.1. Canada Market size and forecast, 2015-2027 (USD Million) 46 5.4. Europe 47 5.4.1. Europe Treasury Software Market size and forecast, 2015-2027 47 5.4.2. Europe Treasury Software Market, by Country, 2018 & 2025 (USD Million) 47 5.4.3. Europe Treasury Software Market, by Deployment Mode, 2015-2027 49 5.4.3.1. Europe Treasury Software Market, by Deployment Mode, 2015-2027 (USD Million) 49 5.4.4. Europe Treasury Software Market, by Organization Size, 2015-2027 50 5.4.4.1. Europe Treasury Software Market, by Organization Size, 2015-2027 (USD Million) 50 5.4.5. Europe Treasury Software Market, by Vertical, 2015-2027 51 5.4.5.1. Europe Treasury Software Market, by Vertical, 2015-2027 (USD Million) 51 5.4.6. Germany 52 5.4.6.1. Germany Market size and forecast, 2015-2027 (USD Million) 52 5.4.7. France 53 5.4.7.1. France Market size and forecast, 2015-2027 (USD Million) 53 5.4.8. U.K. 54 5.4.8.1. U.K. Market size and forecast, 2015-2027 (USD Million) 54 5.4.9. Italy 55 5.4.9.1. Italy Market size and forecast, 2015-2027 (USD Million) 55 5.4.10. Spain 56 5.4.10.1. Spain Market size and forecast, 2015-2027 (USD Million) 56 5.4.11. Rest of Europe 57 5.4.11.1. Rest of Europe Market size and forecast, 2015-2027 (USD Million) 57 5.5. Asia Pacific 58 5.5.1. Asia Pacific Treasury Software Market size and forecast, 2015-2027 58 5.5.2. Asia Pacific Treasury Software Market, by Country, 2018 & 2025 (USD Million) 58 5.5.3. Asia Pacific Treasury Software Market, by Deployment Mode, 2015-2027 60 5.5.3.1. Asia Pacific Treasury Software Market, by Deployment Mode, 2015-2027 (USD Million) 60 5.5.4. Asia Pacific Treasury Software Market, by Organization Size, 2015-2027 61 5.5.4.1. Asia Pacific Treasury Software Market, by Organization Size, 2015-2027 (USD Million) 61 5.5.5. Asia Pacific Treasury Software Market, by Vertical, 2015-2027 62 5.5.5.1. Asia Pacific Treasury Software Market, by Vertical, 2015-2027 (USD Million) 62 5.5.6. China 63 5.5.6.1. China Market size and forecast, 2015-2027 (USD Million) 63 5.5.7. Japan 64 5.5.7.1. Japan Market size and forecast, 2015-2027 (USD Million) 64 5.5.8. India 65 5.5.8.1. India Market size and forecast, 2015-2027 (USD Million) 65 5.5.9. South Korea 66 5.5.9.1. South Korea Market size and forecast, 2015-2027 (USD Million) 66 5.5.10. South-East Asia 67 5.5.10.1. South-East Asia Market size and forecast, 2015-2027 (USD Million) 67 5.5.11. Rest of Asia Pacific 68 5.5.11.1. Rest of Asia Pacific Market size and forecast, 2015-2027 (USD Million) 68 5.6. Latin America 69 5.6.1. Latin America Treasury Software Market size and forecast, 2015-2027 69 5.6.2. Latin America Treasury Software Market, by Country, 2018 & 2025 (USD Million) 69 5.6.3. Latin America Treasury Software Market, by Deployment Mode, 2015-2027 71 5.6.3.1. Latin America Treasury Software Market, by Deployment Mode, 2015-2027 (USD Million) 71 5.6.4. Latin America Treasury Software Market, by Organization Size, 2015-2027 72 5.6.4.1. Latin America Treasury Software Market, by Organization Size, 2015-2027 (USD Million) 72 5.6.5. Latin America Treasury Software Market, by Vertical, 2015-2027 73 5.6.5.1. Latin America Treasury Software Market, by Vertical, 2015-2027 (USD Million) 73 5.6.6. Brazil 74 5.6.6.1. Brazil Market size and forecast, 2015-2027 (USD Million) 74 5.6.7. Mexico 75 5.6.7.1. Mexico Market size and forecast, 2015-2027 (USD Million) 75 5.6.8. Rest of Latin America 76 5.6.8.1. Rest of Latin America Market size and forecast, 2015-2027 (USD Million) 76 5.7. The Middle-East and Africa 77 5.7.1. The Middle-East and Africa Treasury Software Market size and forecast, 2015-2027 77 5.7.2. The Middle-East and Africa Treasury Software Market, by Country, 2018 & 2025 (USD Million) 77 5.7.3. The Middle-East and Africa Treasury Software Market, by Deployment Mode, 2015-2027 79 5.7.3.1. The Middle-East and Africa Treasury Software Market, by Deployment Mode, 2015-2027 (USD Million) 79 5.7.4. The Middle-East and Africa Treasury Software Market, by Organization Size, 2015-2027 80 5.7.4.1. The Middle-East and Africa Treasury Software Market, by Organization Size, 2015-2027 (USD Million) 80 5.7.5. The Middle-East and Africa Treasury Software Market, by Vertical, 2015-2027 81 5.7.5.1. The Middle-East and Africa Treasury Software Market, by Vertical, 2015-2027 (USD Million) 81 5.7.6. GCC Countries 82 5.7.6.1. GCC Countries Market size and forecast, 2015-2027 (USD Million) 82 5.7.7. South Africa 83 5.7.7.1. South Africa Market size and forecast, 2015-2027 (USD Million) 83 5.7.8. Rest of Middle-East Africa 84 5.7.8.1. Rest of Middle-East Africa Market size and forecast, 2015-2027 (USD Million) 84 CHAPTER 6. Treasury Software market – Competitive Landscape 85 6.1. Competitor Market Share – Revenue 85 6.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 87 6.3. Strategic Development 88 6.3.1. Acquisitions and Mergers 88 6.3.2. New Products 88 6.3.3. Research & Development Activities 88 CHAPTER 7. Company Profiles 89 7.1. CRM Treasury Systems 89 7.1.1. Company Overview 89 7.1.2. CRM Treasury Systems Revenue and Gross Margin 89 7.1.3. Product portfolio 90 7.1.4. Recent initiatives 91 7.2. DataLog Finance 91 7.2.1. Company Overview 91 7.2.2. DataLog Finance Revenue and Gross Margin 91 7.2.3. Product portfolio 92 7.2.4. Recent initiatives 93 7.3. Financial Sciences Corp. 93 7.3.1. Company Overview 93 7.3.2. Financial Sciences Corp. Revenue and Gross Margin 93 7.3.3. Product portfolio 94 7.3.4. Recent initiatives 95 7.4. Finastra 95 7.4.1. Company Overview 95 7.4.2. Finastra Revenue and Gross Margin 95 7.4.3. Product portfolio 96 7.4.4. Recent initiatives 97 7.5. Cash Analytics Limited 97 7.5.1. Company Overview 97 7.5.2. Cash Analytics Limited Revenue and Gross Margin 97 7.5.3. Product portfolio 98 7.5.4. Recent initiatives 99 7.6. ION. 99 7.6.1. Company Overview 99 7.6.2. ION. Revenue and Gross Margin 99 7.6.3. Product portfolio 100 7.6.4. Recent initiatives 101 7.7. Gtreasury 101 7.7.1. Company Overview 101 7.7.2. Gtreasury Revenue and Gross Margin 101 7.7.3. Product portfolio 102 7.7.4. Recent initiatives 103 7.8. FIS 103 7.8.1. Company Overview 103 7.8.2. FIS Revenue and Gross Margin 103 7.8.3. Product portfolio 104 7.8.4. Recent initiatives 105 7.9. Kyriba Corp. 105 7.9.1. Company Overview 105 7.9.2. Kyriba Corp. Revenue and Gross Margin 105 7.9.3. Product portfolio 106 7.9.4. Recent initiatives 107 7.10. Salmon Software Ltd. 107 7.10.1. Company Overview 107 7.10.2. Salmon Software Ltd. Revenue and Gross Margin 107 7.10.3. Product portfolio 108 7.10.4. Recent initiatives 109 7.11. TreasuryXpress 109 7.11.1. Company Overview 109 7.11.2. TreasuryXpress Revenue and Gross Margin 109 7.11.3. Product portfolio 110 7.11.4. Recent initiatives 111 7.12. Eurobase International 111 7.12.1. Company Overview 111 7.12.2. Eurobase International Revenue and Gross Margin 111 7.12.3. Product portfolio 112 7.12.4. Recent initiatives 113 7.13. Calypso 113 7.13.1. Company Overview 113 7.13.2. Calypso Revenue and Gross Margin 113 7.13.3. Product portfolio 114 7.13.4. Recent initiatives 115 7.14. BELLIN 115 7.14.1. Company Overview 115 7.14.2. BELLIN Revenue and Gross Margin 115 7.14.3. Product portfolio 116 7.14.4. Recent initiatives 117 7.15. Access Systems (UK) Limited 117 7.15.1. Company Overview 117 7.15.2. Access Systems (UK) Limited Revenue and Gross Margin 117 7.15.3. Product portfolio 118 7.15.4. Recent initiatives 119 7.16. CAPIX 119 7.16.1. Company Overview 119 7.16.2. CAPIX Revenue and Gross Margin 119 7.16.3. Product portfolio 120 7.16.4. Recent initiatives 121 7.17. ABM CLOUD 121 7.17.1. Company Overview 121 7.17.2. ABM CLOUD Revenue and Gross Margin 121 7.17.3. Product portfolio 122 7.17.4. Recent initiatives 123 7.18. Oracle Corporation 123 7.18.1. Company Overview 123 7.18.2. Oracle Corporation Revenue and Gross Margin 123 7.18.3. Product portfolio 124 7.18.4. Recent initiatives 125 7.19. SAP SE 125 7.19.1. Company Overview 125 7.19.2. SAP SE Revenue and Gross Margin 125 7.19.3. Product portfolio 126 7.19.4. Recent initiatives 127 CHAPTER 8. Treasury Software — Industry Analysis 128 8.1. Treasury Software Market – Key Trends 128 8.1.1. Market Drivers 129 8.1.2. Market Restraints 129 8.1.3. Market Opportunities 130 8.2. Value Chain Analysis 131 8.3. Technology Roadmap and Timeline 132 8.4. Treasury Software Market – Attractiveness Analysis 133 8.4.1. By Deployment Mode 133 8.4.2. By Organization Size 133 8.4.3. By Vertical 134 8.4.4. By Region 136 CHAPTER 9. Marketing Strategy Analysis, Distributors 137 9.1. Marketing Channel 137 9.2. Direct Marketing 138 9.3. Indirect Marketing 138 9.4. Marketing Channel Development Trend 138 9.5. Economic/Political Environmental Change 139 CHAPTER 10. Report Conclusion 140 CHAPTER 11. Research Approach & Methodology 141 11.1. Report Description 141 11.2. Research Scope 142 11.3. Research Methodology 142 11.3.1. Secondary Research 143 11.3.2. Primary Research 144 11.3.3. Models 145 11.3.3.1. Company Share Analysis Model 145 11.3.3.2. Revenue Based Modeling 146 11.3.3.3. Research Limitations 146

Inquiry For Buying

Treasury Software

Request Sample

Treasury Software