Truck Video Safety Solutions Market Size, Share, and Trends Analysis Report

CAGR :

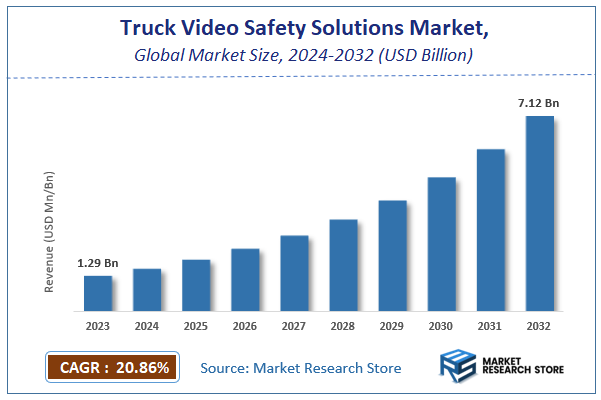

| Market Size 2023 (Base Year) | USD 1.29 Billion |

| Market Size 2032 (Forecast Year) | USD 7.12 Billion |

| CAGR | 20.86% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Truck Video Safety Solutions Market Insights

According to Market Research Store, the global truck video safety solutions market size was valued at around USD 1.29 billion in 2023 and is estimated to reach USD 7.12 billion by 2032, to register a CAGR of approximately 20.86% in terms of revenue during the forecast period 2024-2032.

The truck video safety solutions report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Truck Video Safety Solutions Market: Overview

Truck video safety solutions are advanced systems that utilize video-based technologies to enhance the safety, monitoring, and operational efficiency of commercial trucking fleets. These solutions typically include dashboard cameras (dashcams), rear-view and side-view cameras, in-cab driver-facing cameras, and integrated video telematics platforms. They provide real-time or recorded footage that helps in monitoring driver behavior, documenting road incidents, improving training, and supporting insurance claims. Some systems also incorporate AI-powered features such as lane departure warnings, collision detection, fatigue monitoring, and distracted driving alerts to proactively prevent accidents.

The growth of truck video safety solutions is driven by increasing concerns over road safety, the need to reduce liability in the event of accidents, and the rising demand for fleet visibility and operational accountability. Regulatory pressure and rising insurance premiums are also prompting fleet operators to adopt video safety systems as a means of compliance and cost control. Additionally, advancements in cloud storage, mobile connectivity, and data analytics are enhancing the scalability and effectiveness of these solutions. As commercial transportation continues to digitize and prioritize safety, video-based monitoring systems are becoming essential tools for fleet management, risk mitigation, and driver performance optimization.

Key Highlights

- The truck video safety solutions market is anticipated to grow at a CAGR of 20.86% during the forecast period.

- The global truck video safety solutions market was estimated to be worth approximately USD 1.29 billion in 2023 and is projected to reach a value of USD 7.12 billion by 2032.

- The growth of the truck video safety solutions market is being driven by the increasing focus on road safety, regulatory mandates for commercial fleet monitoring, and the rising adoption of advanced driver assistance systems (ADAS) in logistics and transportation.

- Based on the fleet size, the small fleet segment is growing at a high rate and is projected to dominate the market.

- On the basis of vehicle type, the light commercial vehicle segment is projected to swipe the largest market share.

- In terms of recording view type, the drivers & forward segment is expected to dominate the market.

- Based on the business model, the upfront segment is expected to dominate the market.

- In terms of application, the logistics segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Truck Video Safety Solutions Market: Dynamics

Key Growth Drivers:

- Increasing Emphasis on Fleet Safety and Driver Monitoring: The primary driver is the growing focus on improving safety and reducing accidents in the transportation industry. Video safety solutions provide irrefutable evidence in the event of an accident, which can exonerate drivers from false claims and reduce liability costs for fleets. They also enable fleet managers to monitor driver behavior, identify risky habits like distracted driving or harsh braking, and provide targeted coaching to improve overall safety.

- Stringent Regulatory Mandates and Compliance Requirements: Governments and regulatory bodies worldwide are implementing stricter safety standards for commercial vehicles. For instance, some mandates require the use of electronic logging devices (ELDs) and other safety technologies to ensure compliance with hours-of-service regulations. Video safety solutions are becoming a critical tool for meeting these requirements and demonstrating a commitment to safety, which in turn can lead to lower insurance premiums and avoid fines.

- Integration of AI and Machine Learning for Advanced Analytics: The market is being propelled by the integration of AI and machine learning into video systems. AI-powered cameras can analyze video footage in real-time to detect unsafe behaviors, such as drowsy or distracted driving, and provide immediate alerts. This moves the technology beyond simple recording to proactive risk management and predictive analytics, making it a more valuable tool for fleet managers.

- Need for Operational Efficiency and Cost Reduction: Beyond safety, video solutions are also being used to improve operational efficiency. The data collected can be used to optimize routes, reduce fuel consumption by coaching drivers on efficient habits, and streamline the claims process after an accident. By reducing accidents and improving overall fleet performance, these solutions offer a clear return on investment (ROI) that is a major driver for adoption.

Restraints:

- High Initial Implementation and Infrastructure Costs: The upfront cost of purchasing and installing a comprehensive truck video safety system, particularly one with multiple cameras and advanced AI capabilities, can be a significant barrier for many fleets, especially smaller operators. Additionally, there are costs associated with data storage, connectivity, and ongoing software subscriptions, which can be prohibitive for businesses with limited budgets.

- Driver Privacy Concerns and Resistance to Monitoring: The use of in-cab, driver-facing cameras raises significant privacy concerns among truck drivers. Many drivers and labor organizations are resistant to what they perceive as constant surveillance, which can lead to a negative work environment and potential employee turnover. Overcoming this resistance and building trust requires transparent communication and a clear demonstration of how the technology benefits the driver (e.g., through exoneration in accidents).

- Data Overload and Management Challenges: Video safety systems can generate a massive amount of data, which can lead to information overload for fleet managers. The challenge is not just to collect the data but to effectively analyze it and turn it into actionable insights. Without a powerful and user-friendly software platform, the sheer volume of data can be overwhelming and can limit the system's effectiveness.

- Cybersecurity Risks: As these systems become more connected, they also become more vulnerable to cyberattacks. The risk of unauthorized access to sensitive data, including video footage and personal driver information, is a major concern. Protecting this data and ensuring the security of the connected systems is a critical challenge that requires significant investment in cybersecurity infrastructure.

Opportunities:

- Expansion into Small and Medium-Sized Fleets: While large fleets have been the primary adopters, there is a vast, untapped market in the small and medium-sized enterprise (SME) segment. As the cost of technology decreases and cloud-based, subscription models become more prevalent, video safety solutions are becoming more accessible and affordable for a wider range of businesses.

- Integration with Insurance Telematics: The market has a significant opportunity to partner with the insurance industry. Insurers are increasingly offering discounts and incentives to fleets that use video safety solutions, as these systems can demonstrably reduce accident rates and claims costs. This partnership can help drive adoption by making the technology more financially attractive for fleets.

- Development of All-in-One and Integrated Solutions: Fleet managers are seeking integrated solutions that combine video safety with other telematics functions, such as GPS tracking, fuel management, and vehicle diagnostics. Vendors who can offer a comprehensive, all-in-one platform that seamlessly integrates these functions will have a significant competitive advantage.

- Leveraging Data for Predictive Maintenance: The video and sensor data collected by these systems can be used for more than just driver coaching. The data can be analyzed to identify potential vehicle maintenance issues before they cause a breakdown, which can reduce downtime, lower repair costs, and improve overall operational efficiency.

Challenges:

- Ensuring Consistent Data Quality and Reliability: A key challenge is to ensure that the video and sensor data collected is consistently high-quality and reliable, regardless of weather conditions, lighting, or the specific vehicle model. Any inaccuracies in the data can lead to incorrect coaching decisions or fail to provide the necessary evidence in a legal case, which can erode trust in the system.

- Navigating a Fragmented Regulatory Landscape: The regulatory landscape for in-cab monitoring and data privacy varies significantly by country and even by state. The challenge is for vendors to create solutions that can be easily customized to meet these diverse regulations and for fleets to navigate this complexity without falling out of compliance.

- Balancing Safety with the Driver's Sense of Autonomy: While video safety solutions are designed to improve safety, they can also be perceived as a tool that reduces a driver's sense of autonomy and trust. The challenge is to implement these systems in a way that is collaborative and supportive, focusing on using the data for positive coaching and rewarding good behavior, rather than for punitive measures.

- The "Black Box" of AI-Driven Insights: As AI becomes more integrated, there is a challenge related to the "black box" problem, where the reasoning behind an AI-driven decision is not transparent. Fleet managers need to be able to trust the system and understand why a particular event was flagged as a risk, which requires a focus on explainable AI and clear reporting.

Truck Video Safety Solutions Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Truck Video Safety Solutions Market |

| Market Size in 2023 | USD 1.29 Billion |

| Market Forecast in 2032 | USD 7.12 Billion |

| Growth Rate | CAGR of 20.86% |

| Number of Pages | 240 |

| Key Companies Covered | MiX Telematics, Ryder System, Inc., Lytx, Inc., Safe Fleet, GreenRoad Technologies, Inc., TeletracNavman US Ltd, SmartDrive Systems, Trimble, AB Volvo, DuPont, Goodyear, Daimler AG, Intertruck, LightMetrics, Netradyne, Knorr-Bremse AG, Omnitracs, Scania, Inc., and Verizon |

| Segments Covered | By Fleet Size, By Vehicle Type, By Recording View Type, By Business Model, By Application, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Truck Video Safety Solutions Market: Segmentation Insights

The global truck video safety solutions market is divided by fleet size, vehicle type, recording view type, business model, application, and region.

Based on fleet size, the global truck video safety solutions market is divided into small fleet and larger fleet. Small Fleet dominates the Truck Video Safety Solutions Market due to the increasing adoption of affordable, scalable video safety technologies among independent truck operators and fleets with fewer than 50 vehicles. Small fleet operators are increasingly investing in dashcams, AI-powered driver monitoring systems, and real-time video analytics to improve driver accountability, reduce liability, and lower insurance premiums. These fleets often operate under tight profit margins and seek cost-effective solutions that enhance safety without requiring extensive infrastructure. The growing availability of plug-and-play video systems and cloud-based platforms tailored to smaller operations has accelerated adoption in this segment, making it the primary contributor to market growth.

On the basis of vehicle type, the global truck video safety solutions market is bifurcated into light commercial vehicle and medium/heavy commercial vehicle. Light Commercial Vehicle (LCV) dominates the Truck Video Safety Solutions Market due to the rapid growth in last-mile delivery services, urban logistics, and e-commerce transportation needs. Operators of LCVs, such as vans and small trucks, are increasingly adopting video safety systems to monitor driving behavior in congested city routes, ensure timely deliveries, and protect against false accident claims. These vehicles often navigate dense urban environments where collision risks are high, making real-time video monitoring, GPS tracking, and AI-based driver assistance crucial. The rising number of small and mid-sized businesses deploying LCVs for business operations has further driven demand in this segment.

In terms of recording view type, the global truck video safety solutions market is bifurcated into drivers & forward and others. Drivers & Forward view dominates the Truck Video Safety Solutions Market as it captures both the road ahead and the driver's behavior, offering the most comprehensive insight into real-time driving conditions and driver performance. This dual-view configuration is highly favored for its ability to reduce liability in case of accidents by providing clear visual evidence of external events as well as internal driver actions such as distraction, fatigue, or mobile phone usage. Insurance companies and fleet managers prefer this setup for claim validation, driver coaching, and compliance purposes. The increasing availability of AI-powered dual-facing dashcams with real-time alerts, facial recognition, and fatigue detection features has made this segment the most adopted recording view type across both small and large fleets.

On the basis of business model, the global truck video safety solutions market is bifurcated into upfront and subscription. Upfront model dominates the Truck Video Safety Solutions Market, especially among fleets that prefer to make a one-time capital investment in hardware and software. In this model, businesses purchase video safety equipment—such as dashcams, recording units, and associated software licenses—directly from vendors or resellers. It is favored by organizations with larger budgets or capital expenditure flexibility, allowing them to own the system outright without recurring payments. The upfront model is also attractive to fleets operating in regions with limited internet connectivity or regulatory constraints that restrict continuous cloud-based data usage. Additionally, some companies prefer having full control over data storage and privacy, which is more feasible with on-premises, upfront solutions.

In terms of application, the global truck video safety solutions market is bifurcated into logistics, retail, energy & utilities, construction & mining, oil & petroleum, and finance & banking. Logistics is the dominant application segment in the Truck Video Safety Solutions Market due to the extensive use of commercial vehicles for transporting goods across regional and international routes. Fleet operators in logistics prioritize safety, operational efficiency, and regulatory compliance, making video safety systems essential. These systems help in monitoring driver behavior, reducing accident-related costs, and optimizing route performance. Real-time alerts, AI-based driver coaching, and cloud-connected video analytics have become standard in this sector, especially with the rise in e-commerce and just-in-time delivery demands.

Truck Video Safety Solutions Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Truck Video Safety Solutions Market due to the region’s robust regulatory frameworks, high adoption of safety technologies, and strong insurance-driven incentives for fleet safety enhancement. Federal safety mandates and Department of Transportation (DOT) regulations require the use of rear-view and side-view camera systems in commercial trucks, especially those operating across state lines. Moreover, widespread integration of telematics with AI-based video analytics allows fleet operators to monitor driver behavior, enforce safety protocols, and ensure compliance in real time. Major logistics companies and last-mile delivery services across the United States and Canada utilize dashcams, blind-spot cameras, and in-cab monitoring systems not only for safety, but also for driver training and post-incident investigations. The presence of leading video telematics companies, well-established infrastructure, and a fleet culture focused on risk reduction and operational transparency reinforces North America’s leading position in the global market.

Asia-Pacific is the fastest-growing region in the Truck Video Safety Solutions Market, driven by rapid urbanization, increasing e-commerce activity, and rising concerns over road safety. Countries such as China, India, Japan, and South Korea are investing heavily in digital transportation infrastructure and enforcing new regulations around commercial vehicle safety. In India and Southeast Asia, logistics providers and long-haul freight operators are beginning to equip their fleets with basic camera systems to improve accountability, reduce accidents, and comply with emerging safety standards. Meanwhile, advanced economies like Japan and South Korea are adopting AI-enabled multi-camera solutions that offer lane departure warnings, fatigue detection, and driver scoring based on real-time video analysis. The availability of affordable and scalable cloud-based video solutions, combined with growing demand for fleet visibility and operational efficiency, is accelerating adoption across both domestic and cross-border transportation services in the region.

Europe represents a mature and regulation-driven market for truck video safety solutions, underpinned by stringent European Union mandates that require blind-spot monitoring and rear-view camera systems in commercial vehicles. Key countries including Germany, the United Kingdom, France, and the Netherlands are at the forefront of deploying multi-camera systems to meet Vision Zero goals and reduce pedestrian and cyclist fatalities in urban areas. European fleets are not only focused on regulatory compliance but also on using advanced video analytics to enhance driver performance and reduce insurance claims. Fleets operating in environmentally conscious regions also adopt these systems to minimize accident-related downtime and emissions. Furthermore, collaboration between technology providers, OEMs, and fleet operators is fostering a well-integrated safety ecosystem that combines ADAS, AI-powered dashcams, and remote fleet monitoring in real-time. This structured approach to safety and sustainability ensures Europe remains one of the most sophisticated regional markets for truck video safety solutions.

Latin America is an emerging market with growing potential in the adoption of truck video safety solutions technologies, especially in urban logistics and cross-border transportation. Countries such as Brazil, Mexico, Argentina, and Chile are beginning to enforce safety standards that encourage the use of onboard cameras and visual monitoring systems in commercial vehicles. Urban areas plagued by high accident rates and theft—particularly in cities like São Paulo and Mexico City—are driving the demand for fleet surveillance, real-time tracking, and video documentation. Local logistics operators and government agencies are increasingly recognizing the value of video safety systems in mitigating legal disputes, improving delivery reliability, and enhancing driver accountability. Although infrastructure limitations and upfront equipment costs still challenge widespread deployment, collaborations with international technology providers and regional initiatives to modernize fleet operations are gradually transforming Latin America into a growth-ready market for video safety adoption in the trucking industry.

Middle East & Africa is in the early stages of integrating truck video safety solutions, but selective and strategic growth is underway across key economies in the region. In the Middle East, countries such as the United Arab Emirates, Saudi Arabia, and Qatar are incorporating video monitoring technologies into large-scale logistics and infrastructure development projects. These systems are commonly used in port operations, construction fleets, and government-run transportation services to ensure driver compliance and cargo security. In Africa, particularly in South Africa and Kenya, the use of video safety solutions is gradually expanding among private freight operators and mining fleets, driven by the need for theft prevention, insurance verification, and driver behavior monitoring. Although the broader region still faces challenges such as limited technical infrastructure, high implementation costs, and lack of standardized regulations, the emergence of smart city initiatives, fleet digitization, and international investment in road safety programs is beginning to catalyze market growth for truck video safety technologies across MEA.

Truck Video Safety Solutions Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the truck video safety solutions market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global truck video safety solutions market include:

- AB Volvo

- Daimler AG

- Driverless. global

- DuPont

- Goodyear

- GreenRoad Technologies Inc.

- Intertruck

- Knorr-Bremse AG

- LightMetrics

- Lytx Inc.

- MiX Telematics

- Netradyne

- Omnitracs

- Ryder System Inc.

- Safe Fleet

- Scania

- SmartDrive Systems Inc.

- Teletrac Navman US Ltd

- Trimble

- Verizon

- TeletracNavman US Ltd

The global truck video safety solutions market is segmented as follows:

By Fleet Size Segment Analysis

- Small Fleet

- Larger Fleet

By Vehicle Type Segment Analysis

- Light Commercial Vehicle

- Medium/Heavy Commercial Vehicle

By Recording View Type Segment Analysis

- Drivers & Forward

- Others

By Business Model Segment Analysis

- Upfront

- Subscription

By Application Segment Analysis

- Logistics

- Retail

- Energy & Utilities

- Construction & Mining

- Oil & Petroleum

- Finance & Banking

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

CHAPTER 1. Executive Summary 26 CHAPTER 2. Truck Video Safety Solutions market – Business Model Analysis 29 2.1. Global Truck Video Safety Solutions Market – Business Model Overview 29 2.2. Global Truck Video Safety Solutions Market Share, by Business Model, 2018 & 2025 (USD Million) 29 2.3. Upfront 31 2.3.1. Global Upfront Truck Video Safety Solutions Market, 2016-2026 (USD Million) 31 2.4. Subscription 32 2.4.1. Global Subscription Truck Video Safety Solutions Market, 2016-2026 (USD Million) 32 CHAPTER 3. Truck Video Safety Solutions market – Fleet Size Analysis 32 3.1. Global Truck Video Safety Solutions Market – Fleet Size Overview 32 3.2. Global Truck Video Safety Solutions Market Share, by Fleet Size, 2018 & 2025 (USD Million) 33 3.3. Small Fleet 34 3.3.1. Global Small Fleet Truck Video Safety Solutions Market, 2016-2026 (USD Million) 34 3.4. Larger Fleet 35 3.4.1. Global Larger Fleet Truck Video Safety Solutions Market, 2016-2026 (USD Million) 35 CHAPTER 4. Truck Video Safety Solutions market – Vehicle Type Analysis 35 4.1. Global Truck Video Safety Solutions Market – Vehicle Type Overview 35 4.2. Global Truck Video Safety Solutions Market Share, by Vehicle Type, 2018 & 2025 (USD Million) 36 4.3. Light commercial vehicle 37 4.3.1. Global Light commercial vehicle Truck Video Safety Solutions Market, 2016-2026 (USD Million) 37 4.4. Medium/heavy commercial vehicles 38 4.4.1. Global Medium/heavy commercial vehicles Truck Video Safety Solutions Market, 2016-2026 (USD Million) 38 CHAPTER 5. Truck Video Safety Solutions market – Recording View Type Analysis 38 5.1. Global Truck Video Safety Solutions Market – Recording View Type Overview 38 5.2. Global Truck Video Safety Solutions Market Share, by Recording View Type, 2018 & 2025 (USD Million) 39 5.3. Drivers and Forward 40 5.3.1. Global Drivers and Forward Truck Video Safety Solutions Market, 2016-2026 (USD Million) 40 5.4. Others 41 5.4.1. Global Others Truck Video Safety Solutions Market, 2016-2026 (USD Million) 41 CHAPTER 6. Truck Video Safety Solutions market – Application Analysis 41 6.1. Global Truck Video Safety Solutions Market – Application Overview 41 6.2. Global Truck Video Safety Solutions Market Share, by Application, 2018 & 2025 (USD Million) 42 6.3. Logistics 43 6.3.1. Global Logistics Truck Video Safety Solutions Market, 2016-2026 (USD Million) 43 6.4. Energy and utilities 44 6.4.1. Global Energy and utilities Truck Video Safety Solutions Market, 2016-2026 (USD Million) 44 6.5. Retail 45 6.5.1. Global Retail Truck Video Safety Solutions Market, 2016-2026 (USD Million) 45 6.6. FnB 46 6.6.1. Global FnB Truck Video Safety Solutions Market, 2016-2026 (USD Million) 46 6.7. Oil and Petroleum 47 6.7.1. Global Oil and Petroleum Truck Video Safety Solutions Market, 2016-2026 (USD Million) 47 6.8. Construction and mining 48 6.8.1. Global Construction and mining Truck Video Safety Solutions Market, 2016-2026 (USD Million) 48 6.9. Public Sector 49 6.9.1. Global Public Sector Truck Video Safety Solutions Market, 2016-2026 (USD Million) 49 CHAPTER 7. Truck Video Safety Solutions market – Regional Analysis 50 7.1. Global Truck Video Safety Solutions Market Regional Overview 50 7.2. Global Truck Video Safety Solutions Market Share, by Region, 2018 & 2025 (Value) 50 7.3. North America 52 7.3.1. North America Truck Video Safety Solutions Market size and forecast, 2016-2026 52 7.3.2. North America Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 52 7.3.3. North America Truck Video Safety Solutions Market, by Business Model, 2016-2026 54 7.3.3.1. North America Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 54 7.3.4. North America Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 55 7.3.4.1. North America Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 55 7.3.5. North America Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 56 7.3.5.1. North America Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 56 7.3.6. North America Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 57 7.3.6.1. North America Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 57 7.3.7. North America Truck Video Safety Solutions Market, by Application, 2016-2026 58 7.3.7.1. North America Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 58 7.4. Europe 59 7.4.1. Europe Truck Video Safety Solutions Market size and forecast, 2016-2026 59 7.4.2. Europe Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 59 7.4.3. Europe Truck Video Safety Solutions Market, by Business Model, 2016-2026 60 7.4.3.1. Europe Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 60 7.4.4. Europe Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 61 7.4.4.1. Europe Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 61 7.4.5. Europe Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 62 7.4.5.1. Europe Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 62 7.4.6. Europe Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 63 7.4.6.1. Europe Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 63 7.4.7. Europe Truck Video Safety Solutions Market, by Application, 2016-2026 64 7.4.7.1. Europe Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 64 7.5. China 65 7.5.1. China Truck Video Safety Solutions Market size and forecast, 2016-2026 65 7.5.2. China Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 65 7.5.3. China Truck Video Safety Solutions Market, by Business Model, 2016-2026 66 7.5.3.1. China Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 66 7.5.4. China Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 67 7.5.4.1. China Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 67 7.5.5. China Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 68 7.5.5.1. China Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 68 7.5.6. China Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 69 7.5.6.1. China Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 69 7.5.7. China Truck Video Safety Solutions Market, by Application, 2016-2026 70 7.5.7.1. China Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 70 7.6. Japan 71 7.6.1. Japan Truck Video Safety Solutions Market size and forecast, 2016-2026 71 7.6.2. Japan Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 71 7.6.3. Japan Truck Video Safety Solutions Market, by Business Model, 2016-2026 72 7.6.3.1. Japan Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 72 7.6.4. Japan Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 73 7.6.4.1. Japan Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 73 7.6.5. Japan Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 74 7.6.5.1. Japan Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 74 7.6.6. Japan Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 75 7.6.6.1. Japan Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 75 7.6.7. Japan Truck Video Safety Solutions Market, by Application, 2016-2026 76 7.6.7.1. Japan Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 76 7.7. India 77 7.7.1. India Truck Video Safety Solutions Market size and forecast, 2016-2026 77 7.7.2. India Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 77 7.7.3. India Truck Video Safety Solutions Market, by Business Model, 2016-2026 78 7.7.3.1. India Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 78 7.7.4. India Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 79 7.7.4.1. India Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 79 7.7.5. India Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 80 7.7.5.1. India Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 80 7.7.6. India Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 81 7.7.6.1. India Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 81 7.7.7. India Truck Video Safety Solutions Market, by Application, 2016-2026 82 7.7.7.1. India Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 82 7.8. Southeast Asia 83 7.8.1. Southeast Asia Truck Video Safety Solutions Market size and forecast, 2016-2026 83 7.8.2. Southeast Asia Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 83 7.8.3. Southeast Asia Truck Video Safety Solutions Market, by Business Model, 2016-2026 85 7.8.3.1. Southeast Asia Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 85 7.8.4. Southeast Asia Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 86 7.8.4.1. Southeast Asia Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 86 7.8.5. Southeast Asia Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 87 7.8.5.1. Southeast Asia Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 87 7.8.6. Southeast Asia Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 88 7.8.6.1. Southeast Asia Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 88 7.8.7. Southeast Asia Truck Video Safety Solutions Market, by Application, 2016-2026 89 7.8.7.1. Southeast Asia Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 89 7.9. Rest of the World 90 7.9.1. Rest of the World Truck Video Safety Solutions Market size and forecast, 2016-2026 90 7.9.2. Rest of the World Truck Video Safety Solutions Market, by Country, 2018 & 2025 (USD Million) 90 7.9.3. Rest of the World Truck Video Safety Solutions Market, by Business Model, 2016-2026 92 7.9.3.1. Rest of the World Truck Video Safety Solutions Market, by Business Model, 2016-2026 (USD Million) 92 7.9.4. Rest of the World Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 93 7.9.4.1. Rest of the World Truck Video Safety Solutions Market, by Fleet Size, 2016-2026 (USD Million) 93 7.9.5. Rest of the World Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 94 7.9.5.1. Rest of the World Truck Video Safety Solutions Market, by Vehicle Type, 2016-2026 (USD Million) 94 7.9.6. Rest of the World Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 95 7.9.6.1. Rest of the World Truck Video Safety Solutions Market, by Recording View Type, 2016-2026 (USD Million) 95 7.9.7. Rest of the World Truck Video Safety Solutions Market, by Application, 2016-2026 96 7.9.7.1. Rest of the World Truck Video Safety Solutions Market, by Application, 2016-2026 (USD Million) 96 CHAPTER 8. Truck Video Safety Solutions market – Competitive Landscape 97 8.1. Competitor Market Share – Revenue 97 8.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 99 8.3. Strategic Development 100 8.3.1. Acquisitions and Mergers 100 8.3.2. New Products 100 8.3.3. Research & Development Activities 100 CHAPTER 9. Company Profiles 101 9.1. AB Volvo 101 9.1.1. Company Overview 101 9.1.2. AB Volvo Revenue and Gross Margin 101 9.1.3. Product portfolio 102 9.1.4. Recent initiatives 103 9.2. Daimler AG 103 9.2.1. Company Overview 103 9.2.2. Daimler AG Revenue and Gross Margin 103 9.2.3. Product portfolio 104 9.2.4. Recent initiatives 105 9.3. Driverless.global 105 9.3.1. Company Overview 105 9.3.2. Driverless.global Revenue and Gross Margin 105 9.3.3. Product portfolio 106 9.3.4. Recent initiatives 107 9.4. DuPont 107 9.4.1. Company Overview 107 9.4.2. DuPont Revenue and Gross Margin 107 9.4.3. Product portfolio 108 9.4.4. Recent initiatives 109 9.5. Goodyear 109 9.5.1. Company Overview 109 9.5.2. Goodyear Revenue and Gross Margin 109 9.5.3. Product portfolio 110 9.5.4. Recent initiatives 111 9.6. GreenRoad Technologies, Inc. 111 9.6.1. Company Overview 111 9.6.2. GreenRoad Technologies, Inc. Revenue and Gross Margin 111 9.6.3. Product portfolio 112 9.6.4. Recent initiatives 113 9.7. Intertruck 113 9.7.1. Company Overview 113 9.7.2. Intertruck Revenue and Gross Margin 113 9.7.3. Product portfolio 114 9.7.4. Recent initiatives 115 9.8. Knorr-Bremse AG 115 9.8.1. Company Overview 115 9.8.2. Knorr-Bremse AG Revenue and Gross Margin 115 9.8.3. Product portfolio 116 9.8.4. Recent initiatives 117 9.9. LightMetrics 117 9.9.1. Company Overview 117 9.9.2. LightMetrics Revenue and Gross Margin 117 9.9.3. Product portfolio 118 9.9.4. Recent initiatives 119 9.10. Lytx, Inc. 119 9.10.1. Company Overview 119 9.10.2. Lytx, Inc. Revenue and Gross Margin 119 9.10.3. Product portfolio 120 9.10.4. Recent initiatives 121 9.11. MiX Telematics 121 9.11.1. Company Overview 121 9.11.2. MiX Telematics Revenue and Gross Margin 121 9.11.3. Product portfolio 122 9.11.4. Recent initiatives 123 9.12. Netradyne 123 9.12.1. Company Overview 123 9.12.2. Netradyne Revenue and Gross Margin 123 9.12.3. Product portfolio 124 9.12.4. Recent initiatives 125 9.13. Omnitracs 125 9.13.1. Company Overview 125 9.13.2. Omnitracs Revenue and Gross Margin 125 9.13.3. Product portfolio 126 9.13.4. Recent initiatives 127 9.14. Ryder System, Inc. 127 9.14.1. Company Overview 127 9.14.2. Ryder System, Inc. Revenue and Gross Margin 127 9.14.3. Product portfolio 128 9.14.4. Recent initiatives 129 9.15. Safe Fleet 129 9.15.1. Company Overview 129 9.15.2. Safe Fleet Revenue and Gross Margin 129 9.15.3. Product portfolio 130 9.15.4. Recent initiatives 131 9.16. Scania 131 9.16.1. Company Overview 131 9.16.2. Scania Revenue and Gross Margin 131 9.16.3. Product portfolio 132 9.16.4. Recent initiatives 133 9.17. SmartDrive Systems, Inc. 133 9.17.1. Company Overview 133 9.17.2. SmartDrive Systems, Inc. Revenue and Gross Margin 133 9.17.3. Product portfolio 134 9.17.4. Recent initiatives 135 9.18. Teletrac Navman US Ltd 135 9.18.1. Company Overview 135 9.18.2. Teletrac Navman US Ltd Revenue and Gross Margin 135 9.18.3. Product portfolio 136 9.18.4. Recent initiatives 137 9.19. Trimble 137 9.19.1. Company Overview 137 9.19.2. Trimble Revenue and Gross Margin 137 9.19.3. Product portfolio 138 9.19.4. Recent initiatives 139 9.20. Verizon 139 9.20.1. Company Overview 139 9.20.2. Verizon Revenue and Gross Margin 139 9.20.3. Product portfolio 140 9.20.4. Recent initiatives 141 CHAPTER 10. Truck Video Safety Solutions — Industry Analysis 142 10.1. Truck Video Safety Solutions Market – Key Trends 142 10.1.1. Market Drivers 143 10.1.2. Market Restraints 143 10.1.3. Market Opportunities 144 10.2. Value Chain Analysis 145 10.3. Technology Roadmap and Timeline 146 10.4. Truck Video Safety Solutions Market – Attractiveness Analysis 147 10.4.1. By Business Model 147 10.4.2. By Fleet Size 147 10.4.3. By Vehicle Type 148 10.4.4. By Recording View Type 149 10.4.5. By Application 149 10.4.6. By Region 151 CHAPTER 11. Marketing Strategy Analysis, Distributors 152 11.1. Marketing Channel 152 11.2. Direct Marketing 153 11.3. Indirect Marketing 153 11.4. Marketing Channel Development Trend 153 11.5. Economic/Political Environmental Change 154 CHAPTER 12. Report Conclusion 155 CHAPTER 13. Research Approach & Methodology 156 13.1. Report Description 156 13.2. Research Scope 157 13.3. Research Methodology 157 13.3.1. Secondary Research 158 13.3.2. Primary Research 159 13.3.3. Models 160 13.3.3.1. Company Share Analysis Model 160 13.3.3.2. Revenue Based Modeling 161 13.3.3.3. Research Limitations 161

Inquiry For Buying

Truck Video Safety Solutions

Request Sample

Truck Video Safety Solutions