Urinary Tract Infection Therapeutics Market Size, Share, and Trends Analysis Report

CAGR :

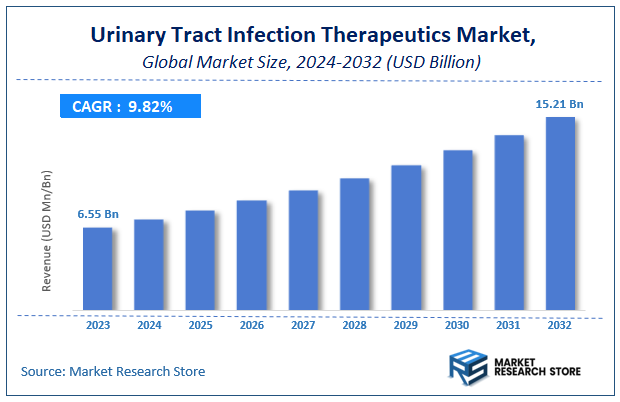

| Market Size 2023 (Base Year) | USD 6.55 Billion |

| Market Size 2032 (Forecast Year) | USD 15.21 Billion |

| CAGR | 9.82% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Urinary Tract Infection Therapeutics Market Insights

According to Market Research Store, the global urinary tract infection therapeutics market size was valued at around USD 6.55 billion in 2023 and is estimated to reach USD 15.21 billion by 2032, to register a CAGR of approximately 9.82% in terms of revenue during the forecast period 2024-2032.

The urinary tract infection therapeutics report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Urinary Tract Infection Therapeutics Market: Overview

Urinary tract infection therapeutics encompass a range of treatments aimed at managing and eliminating infections that affect parts of the urinary system, including the bladder, urethra, ureters, and kidneys. These therapeutics primarily consist of antibiotics, which are the first-line treatment used to target and eradicate the causative bacteria, most commonly Escherichia coli. Depending on the severity and location of the infection, treatment options may include oral antibiotics for uncomplicated UTIs or intravenous antibiotics for more severe or recurrent infections. Adjunctive therapies, such as urinary analgesics and probiotics, may also be used to relieve symptoms and restore microbial balance.

The growth of the urinary tract infection therapeutics market is driven by the high global prevalence of UTIs, especially among women, the elderly, and individuals with underlying health conditions such as diabetes or catheter use. Rising antibiotic resistance is also prompting the development of novel drug formulations and non-antibiotic therapies, such as vaccines, phytotherapeutics, and bacteriophage treatments. Increasing awareness, improvements in diagnostic technologies, and expanding access to healthcare in emerging regions further support market expansion. As the demand for effective, fast-acting, and resistance-combatting UTI treatments rises, ongoing pharmaceutical innovation and public health initiatives are shaping the future of this therapeutic area.

Key Highlights

- The urinary tract infection therapeutics market is anticipated to grow at a CAGR of 9.82% during the forecast period.

- The global urinary tract infection therapeutics market was estimated to be worth approximately USD 6.55 billion in 2023 and is projected to reach a value of USD 15.21 billion by 2032.

- The growth of the urinary tract infection therapeutics market is being driven by the rising prevalence of UTIs globally, particularly among women, the elderly, and individuals with chronic medical conditions such as diabetes.

- Based on the drug class, the antibiotics segment is growing at a high rate and is projected to dominate the market.

- On the basis of route of administration, the oral segment is projected to swipe the largest market share.

- In terms of patient demographics, the gender segment is expected to dominate the market.

- Based on the route of infection, the ascending infection segment is expected to dominate the market.

- In terms of therapeutic approach, the preventive care segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Urinary Tract Infection Therapeutics Market: Dynamics

Key Growth Drivers:

- Rising Global Prevalence of UTIs: The most significant driver is the high and increasing incidence of UTIs worldwide, particularly among women, the elderly, and individuals with chronic conditions like diabetes and kidney stones. As these patient populations grow, so does the demand for effective treatments, which provides a strong, foundational market for therapeutics.

- Growing Antimicrobial Resistance: The widespread use and misuse of antibiotics have led to a critical rise in antibiotic-resistant bacteria, making many standard treatments for UTIs less effective. This alarming trend is a major driver, as it is forcing pharmaceutical companies and researchers to invest heavily in developing novel antibiotics and alternative, non-antibiotic therapies.

- Technological Advancements in Diagnostics: The market is being driven by the development of faster and more accurate diagnostic tools. Advanced point-of-care tests and molecular diagnostics can quickly identify the specific bacteria causing the infection and determine their resistance patterns. This allows for more targeted and effective treatment, which not only improves patient outcomes but also helps in the fight against antibiotic resistance.

- Increasing Awareness and Healthcare Expenditure: A growing awareness among the public about the symptoms and risks of UTIs is leading to higher diagnosis and treatment rates. In addition, increasing healthcare expenditure, particularly in emerging economies, is making advanced diagnostics and novel therapeutics more accessible to a wider patient base, further fueling market growth.

Restraints:

- Rise of Self-Medication and Over-the-Counter (OTC) Use: The easy availability of antibiotics in some regions, combined with a lack of awareness about proper dosage and treatment duration, has led to a high rate of self-medication. This practice contributes significantly to antibiotic resistance and can lead to incomplete treatment, which is a major restraint on the market's long-term health.

- Side Effects Associated with Current Treatments: Many existing UTI therapeutics, particularly older-generation antibiotics like fluoroquinolones, are associated with a range of side effects, from gastrointestinal issues to more severe problems. These adverse effects can lead to patient non-compliance, a discontinuation of the medication, and a general hesitation among both patients and physicians to use these drugs.

- Lack of Novel Antibiotics and Limited Pipeline: Despite the urgent need for new treatments, the development pipeline for novel antibiotics has been historically limited. The high cost of R&D, coupled with a relatively low return on investment for antibiotics, has discouraged many pharmaceutical companies from investing in this area. This lack of new options is a significant restraint that complicates the treatment of drug-resistant infections.

- High Cost of Novel and Combination Therapies: While new, more effective combination drugs and alternative therapies are being developed, they often come with a high price tag. This can limit their accessibility, particularly in low- and middle-income countries, and can create a financial burden for healthcare systems and patients without robust insurance coverage.

Opportunities:

- Development of Non-Antibiotic and Alternative Therapies: The urgent need to combat antibiotic resistance has opened up a significant opportunity for non-antibiotic treatments. This includes the development of vaccines, bacteriophage therapy, immune-boosting treatments, and therapies that prevent bacteria from adhering to the urinary tract. These innovative approaches can offer long-term solutions without contributing to the resistance problem.

- Focus on Personalized Medicine: Advancements in diagnostics and genomics are creating an opportunity to develop personalized treatment plans for UTI patients. By understanding the specific strain of bacteria and the patient's genetic predisposition, healthcare providers can tailor therapy to maximize effectiveness and minimize side effects, leading to better patient outcomes.

- Expansion into Emerging Markets: Emerging economies in the Asia-Pacific and Latin America regions, with their large populations and rising healthcare investments, present a vast, untapped market. As these regions experience a rise in healthcare awareness and improve their medical infrastructure, there is a significant opportunity for pharmaceutical companies to introduce their UTI therapeutics.

- Leveraging Digital Health and Telemedicine: The market can be enhanced by integrating digital health solutions. Telemedicine platforms and mobile apps can be used for remote consultations, patient monitoring, and medication reminders. This not only improves patient adherence but also provides a more convenient way for people to seek timely treatment and manage their condition.

Challenges:

- Ensuring Patient Adherence and Completing the Full Course of Treatment: A major challenge is to ensure that patients complete the full course of their antibiotic treatment, even after their symptoms have subsided. The tendency to stop early is a key factor driving antibiotic resistance. Educating patients on this issue and providing easy-to-follow treatment regimens are critical challenges.

- Balancing Efficacy with Safety: The continuous challenge for drug developers is to create new therapies that are highly effective at combating drug-resistant bacteria while also having a favorable safety profile. Any new drug must undergo rigorous testing to ensure its long-term safety, and any unexpected side effects can derail a product's success.

- The "Black Box" of Asymptomatic UTIs: Asymptomatic UTIs, which show no symptoms but involve bacterial colonization, present a diagnostic and treatment challenge. The unnecessary use of antibiotics in these cases can contribute to resistance, while failing to treat them in high-risk patients can lead to more serious complications. The challenge is to develop clear guidelines and better diagnostic tools to manage these cases effectively.

- Complex and Lengthy Regulatory Approval Processes: The development of a new therapeutic, especially a novel antibiotic, is a long, costly, and complex process. Navigating the stringent regulatory approval processes of bodies like the FDA and EMA can delay the introduction of much-needed treatments to the market, which is a major challenge given the urgency of the antibiotic resistance crisis.

Urinary Tract Infection Therapeutics Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Urinary Tract Infection Therapeutics Market |

| Market Size in 2023 | USD 6.55 Billion |

| Market Forecast in 2032 | USD 15.21 Billion |

| Growth Rate | CAGR of 9.82% |

| Number of Pages | 238 |

| Key Companies Covered | Zavante Therapeutics, Urigen, Shionogi, Novo Nordisk, Mylan, MerLion Pharmaceuticals, MediciNova, Lipella Pharmaceuticals, Dr. Reddy’s Laboratories, Bayer, Cipla, AstraZeneca, Aquinox, ALLERGAN, Achaogen, C.H. Boehringer Sohn, F. Hoffmann-La Roche, Pfizer, Sun Pharmaceutical Industries, Teva Pharmaceutical Industries, Novartis, GlaxoSmithKline, and Johnson & Johnson |

| Segments Covered | By Age Group, By Indication, By Distribution Channel, By Drug Type, And By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Urinary Tract Infection Therapeutics Market: Segmentation Insights

The global urinary tract infection therapeutics market is divided by drug class, route of administration, patient demographics, route of infection, therapeutic approach, and region.

Based on drug class, the global urinary tract infection therapeutics market is divided into antibiotics, antiseptics, non-steroidal anti-inflammatory drugs (NSAIDS), urinary analgesics, and probiotics. Antibiotics dominate the urinary tract infection therapeutics Market as the primary and most widely prescribed treatment option for both uncomplicated and complicated UTIs. Common antibiotic classes used include fluoroquinolones, cephalosporins, penicillins, and sulfonamides. These drugs are highly effective in eliminating the bacteria responsible for infections, such as Escherichia coli. The widespread availability, rapid relief of symptoms, and physician preference for antibiotics contribute to their dominance. However, rising concerns over antibiotic resistance and recurrent UTIs have led to growing research into alternative treatment strategies.

On the basis of route of administration, the global urinary tract infection therapeutics market is bifurcated into oral, intravenous, topical, inhalation, and intravesical. Oral administration is the dominating route in the urinary tract infection therapeutics Market and is the first line of treatment for both uncomplicated and recurrent UTIs. This route includes a wide variety of antibiotics such as nitrofurantoin, trimethoprim-sulfamethoxazole, and fluoroquinolones, along with urinary analgesics and NSAIDs. Oral drugs are easy to administer, making them highly preferred in outpatient settings and among the general population. The high compliance rate, convenience, non-invasive nature, and broad availability of generic formulations contribute to the dominant market share of this route. Additionally, oral therapies are cost-effective and suitable for home-based treatment, reducing the need for hospitalization. Healthcare providers commonly prescribe oral medications for women, who are more prone to UTIs, further reinforcing the demand for this route.

In terms of patient demographics, the global urinary tract infection therapeutics market is bifurcated into gender, age group, and pregnancy status. Gender is the dominating segment in the Urinary Tract Infection Therapeutics Market, with females representing the largest patient population affected by UTIs. Anatomical differences such as a shorter urethra and its proximity to the anus make women significantly more susceptible to bacterial infections, especially during reproductive years. The recurrence rate of UTIs is also notably higher in females, contributing to repeated therapeutic demand. Women often experience UTIs related to sexual activity, hormonal changes, or postmenopausal factors, which drive the need for continuous and varied treatment strategies. As a result, pharmaceutical interventions, preventive care, and diagnostic attention are heavily focused on this demographic. In comparison, men are less frequently affected but tend to suffer from more complex or chronic infections, particularly in older age due to prostate enlargement. Despite this, the vast clinical burden and high frequency among women firmly position the gender demographic as the dominant market driver.

On the basis of route of infection, the global urinary tract infection therapeutics market is bifurcated into ascending infection, hematogenous infection, and contiguous spread. Ascending Infection is the most dominant and prevalent route of infection in the urinary tract infection therapeutics market. This pathway typically begins when pathogens, most commonly Escherichia coli, enter the urethra and travel upward into the bladder, potentially progressing further to the ureters and kidneys. Ascending infections are particularly common in women due to their shorter urethra and are often triggered by poor hygiene, sexual activity, or catheter use. As this route accounts for the majority of uncomplicated and recurrent UTIs, therapeutic demand for antibiotics, urinary analgesics, and prophylactic treatments is highest in this segment. Moreover, ascending infections are often the focus of clinical guidelines and public health interventions, reinforcing its dominance in the market.

In terms of patient therapeutic approach, the global urinary tract infection therapeutics market is bifurcated into preventive care, symptomatic treatment, curative treatment, and post-antibiotic care. Preventive Care dominates the urinary tract infection therapeutics market as the emphasis on reducing recurrent infections and minimizing antibiotic resistance becomes more prominent. This approach includes the use of probiotics, immunoactive prophylactic agents, lifestyle modification guidance, hygiene education, and in some cases, low-dose prophylactic antibiotics. Preventive measures are especially important among populations prone to recurrent UTIs, such as women, elderly individuals, and catheterized patients. Growing awareness about the adverse effects of repeated antibiotic use and the increasing availability of preventive supplements have contributed to the dominance of this segment. Preventive care also aligns with global healthcare strategies focused on infection control and sustainable therapeutic outcomes.

Urinary Tract Infection Therapeutics Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Urinary Tract Infection Therapeutics Market due to its advanced healthcare infrastructure, strong presence of leading pharmaceutical companies, and widespread awareness of early diagnosis and treatment of UTIs. In both the United States and Canada, high public health standards, along with frequent screening and treatment of UTIs among vulnerable populations—such as elderly adults, pregnant women, and individuals with chronic health conditions—have supported consistent demand for therapeutics. The region also benefits from regular updates to clinical treatment guidelines and extensive research into new antibiotic formulations, urinary antiseptics, and adjunct therapies to manage resistant bacterial strains. Moreover, robust investment in biotechnology and pharmaceutical innovation has facilitated the development and commercialization of novel treatments, including vaccines and non-antibiotic-based therapies, further reinforcing North America’s leading position in the global market.

Asia-Pacific is experiencing accelerated growth in the Urinary Tract Infection Therapeutics Market, driven by increasing awareness of personal hygiene, growing healthcare access, and a rising burden of urological infections. Countries such as China, India, Japan, and South Korea are witnessing higher UTI incidence rates due to factors such as population density, aging demographics, and expanding chronic disease profiles. While diagnostic capabilities are still uneven across urban and rural settings, rapid improvement in public health infrastructure is enabling more effective identification and treatment of UTIs. Pharmaceutical companies in the region are also expanding the availability of generic antibiotic formulations, making treatment more accessible to large patient populations. At the same time, rising investment in R&D and international clinical trials is encouraging the development of new therapies tailored to regional pathogen resistance patterns and treatment protocols.

Europe represents a mature and well-regulated market for urinary tract infection therapeutics, supported by consistent surveillance systems, government-backed antibiotic stewardship programs, and coordinated cross-border research into antimicrobial resistance. Countries such as Germany, France, the United Kingdom, and the Netherlands have implemented national strategies to improve antibiotic use, promote early diagnosis, and reduce the rate of recurrent infections. This has contributed to increased demand for more targeted and efficient therapeutics, including single-dose antibiotics, herbal formulations, and urinary pH regulators. European healthcare providers are also emphasizing non-antibiotic approaches, such as probiotics and vaccines, particularly in patients with recurrent infections or resistance to conventional therapies. Furthermore, the presence of structured reimbursement policies and a strong network of hospital-based infection control programs ensures broad patient access to standard and advanced treatment regimens across the continent.

Latin America is gradually expanding its presence in the urinary tract infection therapeutics market, with rising awareness and healthcare access helping to improve diagnosis and treatment rates. Countries such as Brazil, Mexico, Chile, and Argentina are making strides in public health education related to UTIs, particularly among women, children, and elderly patients who are more susceptible to such infections. While over-the-counter medication and self-treatment remain common in parts of the region, increasing involvement of healthcare professionals in primary and community settings is shifting treatment protocols toward evidence-based therapies. In addition, partnerships between local distributors and multinational pharmaceutical companies are enhancing the availability of high-quality antibiotics and herbal alternatives across urban centers. Despite challenges related to healthcare funding and regional disparities, the overall outlook for Latin America’s UTI therapeutics market is improving, with greater emphasis now placed on infection prevention, diagnostic accuracy, and antimicrobial stewardship.

Middle East & Africa (MEA) represents an emerging but underserved market for urinary tract infection therapeutics, with wide variations in access to care, diagnostic capabilities, and pharmaceutical availability. In the Middle East, countries like Saudi Arabia, the United Arab Emirates, and Qatar are investing in modern healthcare infrastructure, which is supporting improved detection and treatment of urinary tract infections in both outpatient and hospital settings. These developments are particularly focused on high-risk populations, including diabetics and immunocompromised patients, who require effective management of recurrent infections. In Africa, however, limited access to healthcare facilities and diagnostic laboratories hampers early detection, leading to higher complication rates and inappropriate antibiotic use. Nevertheless, ongoing efforts by health ministries and global health organizations are helping to spread awareness and expand access to essential medicines. As regional supply chains improve and digital health initiatives take root, the MEA region is expected to see gradual but meaningful growth in its capacity to treat UTIs effectively.

Urinary Tract Infection Therapeutics Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the urinary tract infection therapeutics market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global urinary tract infection therapeutics market include:

- Pfizer

- AstraZeneca

- Novartis International

- Johnson & Johnson

- F. Hoffmann La Roche

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

- Cipla

- Zavante Therapeutics

- Urigen

- Shionogi

- Novo Nordisk

- Mylan

- MerLion Pharmaceuticals

- MediciNova

- Lipella Pharmaceuticals

- Dr. Reddy’s Laboratories

- Bayer

- Aquinox

- ALLERGAN

- Achaogen

- Sun Pharmaceutical Industries

- GlaxoSmithKline

The global urinary tract infection therapeutics market is segmented as follows:

By Drug Class

- Antibiotics

- Antiseptics

- Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Urinary Analgesics

- Probiotics

By Route of Administration

- Oral

- Intravenous

- Topical

- Inhalation

- Intravesical

By Patient Demographics

- Gender

- Age Group

- Pregnancy Status

By Route of Infection

- Ascending Infection

- Hematogenous Infection

- Contiguous Spread

By Therapeutic Approach

- Preventive Care

- Symptomatic Treatment

- Curative Treatment

- Post-Antibiotic Care

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

CHAPTER 1. Executive Summary 26 CHAPTER 2. Urinary Tract Infection Therapeutics market – Age Group Analysis 28 2.1. Global Urinary Tract Infection Therapeutics Market – Age Group Overview 28 2.2. Global Urinary Tract Infection Therapeutics Market Share, by Age Group, 2018 & 2025 (USD Million) 28 2.3. Adults 30 2.3.1. Global Adults Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 30 2.4. Elderly 31 2.4.1. Global Elderly Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 31 2.5. Children 32 2.5.1. Global Children Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 32 CHAPTER 3. Urinary Tract Infection Therapeutics market – Indication Analysis 32 3.1. Global Urinary Tract Infection Therapeutics Market – Indication Overview 32 3.2. Global Urinary Tract Infection Therapeutics Market Share, by Indication, 2018 & 2025 (USD Million) 33 3.3. Uncomplicated UTI 34 3.3.1. Global Uncomplicated UTI Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 34 3.4. Recurrent UTI 35 3.4.1. Global Recurrent UTI Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 35 3.5. Complicated UTI 36 3.5.1. Global Complicated UTI Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 36 3.6. CA (Catheter Associated) UTI 37 3.6.1. Global CA (Catheter Associated) UTI Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 37 CHAPTER 4. Urinary Tract Infection Therapeutics market – Drug Type Analysis 37 4.1. Global Urinary Tract Infection Therapeutics Market – Drug Type Overview 37 4.2. Global Urinary Tract Infection Therapeutics Market Share, by Drug Type, 2018 & 2025 (USD Million) 38 4.3. Quinolones 40 4.3.1. Global Quinolones Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 40 4.4. Azoles & Amphotericin B 41 4.4.1. Global Azoles & Amphotericin B Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 41 4.5. Aminoglycoside 42 4.5.1. Global Aminoglycoside Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 42 4.6. Penicillin & Combinations 43 4.6.1. Global Penicillin & Combinations Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 43 4.7. Cephalosporin 44 4.7.1. Global Cephalosporin Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 44 4.8. Nitrofurans 45 4.8.1. Global Nitrofurans Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 45 4.9. Others 46 4.9.1. Global Others Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 46 CHAPTER 5. Urinary Tract Infection Therapeutics market – Distribution Channel Analysis 46 5.1. Global Urinary Tract Infection Therapeutics Market – Distribution Channel Overview 46 5.2. Global Urinary Tract Infection Therapeutics Market Share, by Distribution Channel, 2018 & 2025 (USD Million) 47 5.3. Hospital Pharmacies 48 5.3.1. Global Hospital Pharmacies Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 48 5.4. Retail Pharmacies 49 5.4.1. Global Retail Pharmacies Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 49 5.5. E-commerce 50 5.5.1. Global E-commerce Urinary Tract Infection Therapeutics Market, 2016-2026 (USD Million) 50 CHAPTER 6. Urinary Tract Infection Therapeutics market – Regional Analysis 51 6.1. Global Urinary Tract Infection Therapeutics Market Regional Overview 51 6.2. Global Urinary Tract Infection Therapeutics Market Share, by Region, 2018 & 2025 (Value) 51 6.3. North America 53 6.3.1. North America Urinary Tract Infection Therapeutics Market size and forecast, 2016-2026 53 6.3.2. North America Urinary Tract Infection Therapeutics Market, by Country, 2018 & 2025 (USD Million) 53 6.3.3. North America Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 55 6.3.3.1. North America Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 (USD Million) 55 6.3.4. North America Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 56 6.3.4.1. North America Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 (USD Million) 56 6.3.5. North America Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 57 6.3.5.1. North America Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 (USD Million) 57 6.3.6. North America Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 58 6.3.6.1. North America Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 (USD Million) 58 6.3.7. U.S. 59 6.3.7.1. U.S. Market size and forecast, 2016-2026 (USD Million) 59 6.3.8. Rest of North America 60 6.3.8.1. Rest of North America Market size and forecast, 2016-2026 (USD Million) 60 6.4. Europe 61 6.4.1. Europe Urinary Tract Infection Therapeutics Market size and forecast, 2016-2026 61 6.4.2. Europe Urinary Tract Infection Therapeutics Market, by Country, 2018 & 2025 (USD Million) 61 6.4.3. Europe Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 63 6.4.3.1. Europe Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 (USD Million) 63 6.4.4. Europe Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 64 6.4.4.1. Europe Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 (USD Million) 64 6.4.5. Europe Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 65 6.4.5.1. Europe Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 (USD Million) 65 6.4.6. Europe Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 66 6.4.6.1. Europe Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 (USD Million) 66 6.4.7. Germany 67 6.4.7.1. Germany Market size and forecast, 2016-2026 (USD Million) 67 6.4.8. France 68 6.4.8.1. France Market size and forecast, 2016-2026 (USD Million) 68 6.4.9. U.K. 69 6.4.9.1. U.K. Market size and forecast, 2016-2026 (USD Million) 69 6.4.10. Italy 70 6.4.10.1. Italy Market size and forecast, 2016-2026 (USD Million) 70 6.4.11. Spain 71 6.4.11.1. Spain Market size and forecast, 2016-2026 (USD Million) 71 6.4.12. Rest of Europe 72 6.4.12.1. Rest of Europe Market size and forecast, 2016-2026 (USD Million) 72 6.5. Asia Pacific 73 6.5.1. Asia Pacific Urinary Tract Infection Therapeutics Market size and forecast, 2016-2026 73 6.5.2. Asia Pacific Urinary Tract Infection Therapeutics Market, by Country, 2018 & 2025 (USD Million) 73 6.5.3. Asia Pacific Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 75 6.5.3.1. Asia Pacific Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 (USD Million) 75 6.5.4. Asia Pacific Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 76 6.5.4.1. Asia Pacific Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 (USD Million) 76 6.5.5. Asia Pacific Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 77 6.5.5.1. Asia Pacific Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 (USD Million) 77 6.5.6. Asia Pacific Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 78 6.5.6.1. Asia Pacific Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 (USD Million) 78 6.5.7. China 79 6.5.7.1. China Market size and forecast, 2016-2026 (USD Million) 79 6.5.8. Japan 80 6.5.8.1. Japan Market size and forecast, 2016-2026 (USD Million) 80 6.5.9. India 81 6.5.9.1. India Market size and forecast, 2016-2026 (USD Million) 81 6.5.10. South-East Asia 82 6.5.10.1. South-East Asia Market size and forecast, 2016-2026 (USD Million) 82 6.5.11. Rest of Asia Pacific 83 6.5.11.1. Rest of Asia Pacific Market size and forecast, 2016-2026 (USD Million) 83 6.6. Latin America 84 6.6.1. Latin America Urinary Tract Infection Therapeutics Market size and forecast, 2016-2026 84 6.6.2. Latin America Urinary Tract Infection Therapeutics Market, by Country, 2018 & 2025 (USD Million) 84 6.6.3. Latin America Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 86 6.6.3.1. Latin America Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 (USD Million) 86 6.6.4. Latin America Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 87 6.6.4.1. Latin America Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 (USD Million) 87 6.6.5. Latin America Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 88 6.6.5.1. Latin America Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 (USD Million) 88 6.6.6. Latin America Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 89 6.6.6.1. Latin America Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 (USD Million) 89 6.6.7. Brazil 90 6.6.7.1. Brazil Market size and forecast, 2016-2026 (USD Million) 90 6.6.8. Rest of Latin America 91 6.6.8.1. Rest of Latin America Market size and forecast, 2016-2026 (USD Million) 91 6.7. The Middle-East and Africa 92 6.7.1. The Middle-East and Africa Urinary Tract Infection Therapeutics Market size and forecast, 2016-2026 92 6.7.2. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Country, 2018 & 2025 (USD Million) 92 6.7.3. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 94 6.7.3.1. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Age Group, 2016-2026 (USD Million) 94 6.7.4. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 95 6.7.4.1. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Indication, 2016-2026 (USD Million) 95 6.7.5. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 96 6.7.5.1. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Drug Type, 2016-2026 (USD Million) 96 6.7.6. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 97 6.7.6.1. The Middle-East and Africa Urinary Tract Infection Therapeutics Market, by Distribution Channel, 2016-2026 (USD Million) 97 6.7.7. GCC Countries 98 6.7.7.1. GCC Countries Market size and forecast, 2016-2026 (USD Million) 98 6.7.8. South Africa 99 6.7.8.1. South Africa Market size and forecast, 2016-2026 (USD Million) 99 6.7.9. Rest of Middle-East Africa 100 6.7.9.1. Rest of Middle-East Africa Market size and forecast, 2016-2026 (USD Million) 100 CHAPTER 7. Urinary Tract Infection Therapeutics market – Competitive Landscape 101 7.1. Competitor Market Share – Revenue 101 7.2. Market Concentration Rate Analysis, Top 3 and Top 5 Players 103 7.3. Strategic Development 104 7.3.1. Acquisitions and Mergers 104 7.3.2. New Products 104 7.3.3. Research & Development Activities 104 CHAPTER 8. Company Profiles 105 8.1. Johnson & Johnson Services, Inc. 105 8.1.1. Company Overview 105 8.1.2. Johnson & Johnson Services, Inc. Revenue and Gross Margin 105 8.1.3. Product portfolio 106 8.1.4. Recent initiatives 107 8.2. GlaxoSmithKline 107 8.2.1. Company Overview 107 8.2.2. GlaxoSmithKline Revenue and Gross Margin 107 8.2.3. Product portfolio 108 8.2.4. Recent initiatives 109 8.3. Novartis AG 109 8.3.1. Company Overview 109 8.3.2. Novartis AG Revenue and Gross Margin 109 8.3.3. Product portfolio 110 8.3.4. Recent initiatives 111 8.4. Teva Pharmaceutical Industries Ltd. 111 8.4.1. Company Overview 111 8.4.2. Teva Pharmaceutical Industries Ltd. Revenue and Gross Margin 111 8.4.3. Product portfolio 112 8.4.4. Recent initiatives 113 8.5. Sun Pharmaceutical Industries Ltd. 113 8.5.1. Company Overview 113 8.5.2. Sun Pharmaceutical Industries Ltd. Revenue and Gross Margin 113 8.5.3. Product portfolio 114 8.5.4. Recent initiatives 115 8.6. Pfizer Inc. 115 8.6.1. Company Overview 115 8.6.2. Pfizer Inc. Revenue and Gross Margin 115 8.6.3. Product portfolio 116 8.6.4. Recent initiatives 117 8.7. F. Hoffmann-La Roche Ltd 117 8.7.1. Company Overview 117 8.7.2. F. Hoffmann-La Roche Ltd Revenue and Gross Margin 117 8.7.3. Product portfolio 118 8.7.4. Recent initiatives 119 8.8. C.H. Boehringer Sohn AG & Co.KG 119 8.8.1. Company Overview 119 8.8.2. C.H. Boehringer Sohn AG & Co.KG Revenue and Gross Margin 119 8.8.3. Product portfolio 120 8.8.4. Recent initiatives 121 8.9. Achaogen, Inc. 121 8.9.1. Company Overview 121 8.9.2. Achaogen, Inc. Revenue and Gross Margin 121 8.9.3. Product portfolio 122 8.9.4. Recent initiatives 123 8.10. ALLERGAN 123 8.10.1. Company Overview 123 8.10.2. ALLERGAN Revenue and Gross Margin 123 8.10.3. Product portfolio 124 8.10.4. Recent initiatives 125 8.11. Aquinox 125 8.11.1. Company Overview 125 8.11.2. Aquinox Revenue and Gross Margin 125 8.11.3. Product portfolio 126 8.11.4. Recent initiatives 127 8.12. AstraZeneca 127 8.12.1. Company Overview 127 8.12.2. AstraZeneca Revenue and Gross Margin 127 8.12.3. Product portfolio 128 8.12.4. Recent initiatives 129 8.13. Cipla Inc. 129 8.13.1. Company Overview 129 8.13.2. Cipla Inc. Revenue and Gross Margin 129 8.13.3. Product portfolio 130 8.13.4. Recent initiatives 131 8.14. Bayer AG 131 8.14.1. Company Overview 131 8.14.2. Bayer AG Revenue and Gross Margin 131 8.14.3. Product portfolio 132 8.14.4. Recent initiatives 133 8.15. Dr. Reddy's Laboratories Ltd. 133 8.15.1. Company Overview 133 8.15.2. Dr. Reddy's Laboratories Ltd. Revenue and Gross Margin 133 8.15.3. Product portfolio 134 8.15.4. Recent initiatives 135 8.16. Lipella Pharmaceuticals Inc. 135 8.16.1. Company Overview 135 8.16.2. Lipella Pharmaceuticals Inc. Revenue and Gross Margin 135 8.16.3. Product portfolio 136 8.16.4. Recent initiatives 137 8.17. MediciNova, Inc. 137 8.17.1. Company Overview 137 8.17.2. MediciNova, Inc. Revenue and Gross Margin 137 8.17.3. Product portfolio 138 8.17.4. Recent initiatives 139 8.18. MerLion Pharmaceuticals GmbH 139 8.18.1. Company Overview 139 8.18.2. MerLion Pharmaceuticals GmbH Revenue and Gross Margin 139 8.18.3. Product portfolio 140 8.18.4. Recent initiatives 141 8.19. Mylan N.V. 141 8.19.1. Company Overview 141 8.19.2. Mylan N.V. Revenue and Gross Margin 141 8.19.3. Product portfolio 142 8.19.4. Recent initiatives 143 8.20. Novo Nordisk A/S 143 8.20.1. Company Overview 143 8.20.2. Novo Nordisk A/S Revenue and Gross Margin 143 8.20.3. Product portfolio 144 8.20.4. Recent initiatives 145 8.21. Shionogi Inc. 145 8.21.1. Company Overview 145 8.21.2. Shionogi Inc. Revenue and Gross Margin 145 8.21.3. Product portfolio 146 8.21.4. Recent initiatives 147 8.22. Urigen 147 8.22.1. Company Overview 147 8.22.2. Urigen Revenue and Gross Margin 147 8.22.3. Product portfolio 148 8.22.4. Recent initiatives 149 8.23. Zavante Therapeutics, Inc. 149 8.23.1. Company Overview 149 8.23.2. Zavante Therapeutics, Inc. Revenue and Gross Margin 149 8.23.3. Product portfolio 150 8.23.4. Recent initiatives 151 CHAPTER 9. Urinary Tract Infection Therapeutics — Industry Analysis 152 9.1. Urinary Tract Infection Therapeutics Market – Key Trends 152 9.1.1. Market Drivers 153 9.1.2. Market Restraints 153 9.1.3. Market Opportunities 154 9.2. Value Chain Analysis 155 9.3. Technology Roadmap and Timeline 156 9.4. Urinary Tract Infection Therapeutics Market – Attractiveness Analysis 157 9.4.1. By Age Group 157 9.4.2. By Indication 157 9.4.3. By Drug Type 158 9.4.4. By Distribution Channel 159 9.4.5. By Region 160 CHAPTER 10. Marketing Strategy Analysis, Distributors 161 10.1. Marketing Channel 161 10.2. Direct Marketing 162 10.3. Indirect Marketing 162 10.4. Marketing Channel Development Trend 162 10.5. Economic/Political Environmental Change 163 CHAPTER 11. Report Conclusion 164 CHAPTER 12. Research Approach & Methodology 165 12.1. Report Description 165 12.2. Research Scope 166 12.3. Research Methodology 166 12.3.1. Secondary Research 167 12.3.2. Primary Research 168 12.3.3. Models 169 12.3.3.1. Company Share Analysis Model 169 12.3.3.2. Revenue Based Modeling 170 12.3.3.3. Research Limitations 170

Inquiry For Buying

Urinary Tract Infection Therapeutics

Request Sample

Urinary Tract Infection Therapeutics