Si (Li) Detector Market Size, Share, and Trends Analysis Report

CAGR :

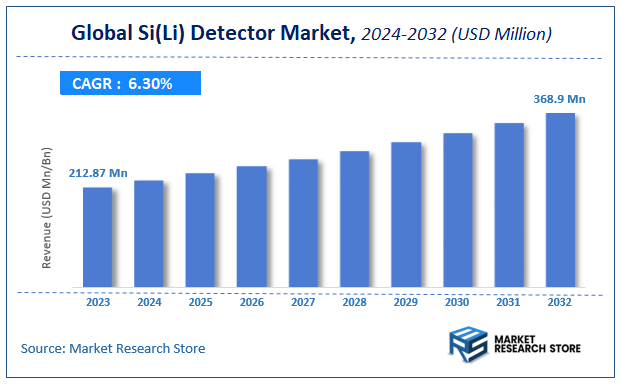

| Market Size 2023 (Base Year) | USD 212.87 Million |

| Market Size 2032 (Forecast Year) | USD 368.9 Million |

| CAGR | 6.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Si(Li) Detector Market Insights

According to Market Research Store, the global si (li) detector market size was valued at around USD 212.87 million in 2023 and is estimated to reach USD 368.9 million by 2032, to register a CAGR of approximately 6.3% in terms of revenue during the forecast period 2024-2032.

The si (li) detector report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

Global Si (Li) Detector Market: Overview

Si (Li) detector, or silicon lithium-drifted detector, is a type of semiconductor radiation detector specifically designed for the precise measurement of X-rays and low-energy gamma rays. It is made by diffusing lithium into high-purity silicon to compensate for impurity charges and create a sensitive detection region with high energy resolution. When ionizing radiation interacts with the silicon, it generates electron-hole pairs that are collected under an electric field, producing a measurable electrical signal proportional to the energy of the incident radiation. Si(Li) detectors are typically operated at cryogenic temperatures using liquid nitrogen to reduce electronic noise and maintain performance.

The demand for Si (Li) detectors is driven by their exceptional energy resolution and sensitivity in the low-energy range, making them ideal for applications such as energy-dispersive X-ray spectroscopy (EDS), environmental monitoring, nuclear research, and quality control in industrial materials analysis. These detectors are especially valued in laboratories and research institutions where accurate elemental identification and trace-level detection are critical. Though newer detector technologies like silicon drift detectors (SDDs) offer advantages in speed and cooling, Si(Li) detectors remain relevant in settings that prioritize ultra-high resolution and established analytical protocols. Ongoing advances in detector electronics and cooling systems are further supporting their continued use in specialized scientific and analytical fields.

Key Highlights

- The si (li) detector market is anticipated to grow at a CAGR of 6.3% during the forecast period.

- The global si (li) detector market was estimated to be worth approximately USD 212.87 million in 2023 and is projected to reach a value of USD 368.9 million by 2032.

- The growth of the si (li) detector market is being driven by the escalating demand for high-resolution spectroscopic analysis across diverse sectors.

- Based on the type, the planar Si (Li) detectors segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the medical imaging segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Si (Li) Detector Market: Dynamics

Key Growth Drivers:

- Demand for High-Resolution X-ray Spectroscopy: Si(Li) detectors offer superior energy resolution, making them essential for applications requiring precise elemental analysis, such as X-ray Fluorescence (XRF) spectroscopy, Electron Dispersive Spectroscopy (EDS) in electron microscopy, and X-ray Diffraction (XRD).

- Applications in Materials Science and Research: Their ability to accurately identify and quantify elements makes them crucial in materials research, failure analysis, geological surveys, and quality control in various industries.

- Continued Use in Specific Scientific and Medical Research: While HPGe detectors are dominant for higher energy gamma rays, Si(Li) detectors retain importance in specific nuclear physics experiments, astrophysics, and certain medical imaging applications where their specific characteristics (e.g., lower escape peaks for certain energies) are advantageous.

- Cost-Effectiveness in Certain Energy Ranges Compared to HPGe: For specific X-ray and low-energy gamma applications, Si(Li) detectors can offer a more cost-effective solution compared to HPGe detectors, which typically require more complex cryogenics for optimal performance across a broader energy range.

- Advancements in Manufacturing Processes: Ongoing research and development in fabrication techniques aim to improve the performance, reliability, and potentially reduce the manufacturing time of Si(Li) detectors, leading to better and more consistent products.

Restraints

- Competition from Silicon Drift Detectors (SDDs): SDDs often offer comparable or superior energy resolution, higher count rates, and the advantage of Peltier cooling (thermoelectric cooling) instead of liquid nitrogen, making them a preferred choice for many XRF and EDS applications. This has significantly impacted the Si(Li) market share.

- Need for Cryogenic Cooling: Si(Li) detectors require continuous cooling, typically with liquid nitrogen (LN2), to maintain their lithium compensation and achieve optimal resolution. This adds to the operational cost, complexity, and logistical challenges, especially in regions with limited LN2 infrastructure.

- Limited Availability and Standardization: The specialized manufacturing process for Si(Li) detectors means their supply can be limited, and a lack of universal standardization can make integration into various systems challenging.

- Performance Limitations at Higher Energies: While excellent for X-rays, Si(Li) detectors have a lower stopping power for higher energy gamma rays compared to HPGe detectors, limiting their use in such applications.

- Relatively Smaller Active Areas (Historically): Traditionally, producing large active area Si(Li) detectors with uniform compensation has been difficult and time-consuming, limiting their use in applications requiring larger detection volumes.

Opportunities

- Niche Applications Requiring Specific Si(Li) Characteristics: Opportunities exist in specialized applications where the unique properties of Si(Li) detectors (e.g., specific escape peak characteristics, thinner dead layers) offer advantages over alternatives.

- Portable and Handheld XRF Devices: Miniaturization and the development of more compact cooling systems for Si(Li) detectors could open opportunities in portable XRF analyzers for field applications in environmental monitoring, material sorting, and geological analysis.

- Advancements in Cooling Technologies: Research into more efficient and compact cooling solutions that reduce or eliminate the need for liquid nitrogen could significantly enhance the appeal of Si(Li) detectors.

- Improved Mass Production Techniques: New fabrication methods that allow for high-yield, large-area Si(Li) detectors with high operating temperatures could revive their use in larger-scale experiments or industrial applications where they were previously deemed too expensive or impractical.

- Growing Research and Development in Developing Regions: As scientific research infrastructure expands in countries like India, there may be opportunities for Si(Li) detectors in new or expanding research laboratories for materials science and elemental analysis.

Challenges

- Sustained Competition from SDDs and HPGe: The primary challenge is to maintain relevance and market share against the continued technological advancements and broader applicability of SDDs and HPGe detectors.

- Managing Cryogenic Requirements: The logistical and operational challenges associated with continuous cryogenic cooling remain a significant hurdle for widespread adoption, especially for end-users who prefer maintenance-free solutions.

- High Manufacturing Complexity: The lithium drifting process is delicate and time-consuming, requiring highly controlled environments, which contributes to high production costs and can limit scalability.

- Market Education and Awareness: There is a need to clearly articulate the specific advantages of Si(Li) detectors for certain applications where they still outperform alternatives, differentiating them effectively in a competitive landscape.

- Talent Pool for Manufacturing and Maintenance: The specialized nature of Si(Li) detector technology means a limited pool of experts for manufacturing, R&D, and maintenance, posing a challenge for companies in the market.

Si(Li) Detector Market: Report Scope

This report thoroughly analyzes the Si(Li) Detector Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Si(Li) Detector Market |

| Market Size in 2023 | USD 212.87 Million |

| Market Forecast in 2032 | USD 368.9 Million |

| Growth Rate | CAGR of 6.3% |

| Number of Pages | 171 |

| Key Companies Covered | Hamamatsu Photonics, Ketek, Advacam, Centronic, Piezo Systems, Sensors Unlimited, Teledyne DALSA, Xenon InstrumentsJEOL, Mirion Technologies, RMT, e2v Scientific Instruments, Amptek, Thermo Fisher, Shimadzu Corporation, PGT |

| Segments Covered | By Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Si (Li) Detector Market: Segmentation Insights

The global si (li) detector market is divided by type, application, and region.

Segmentation Insights by Type

Based on type, the global si (li) detector market is divided into planar Si (Li) detectors, doped Si(Li) detectors, edge-defined, and post-processed (EPPC) detectors.

Planar Si (Li) Detectors dominate the Si (Li) detector market due to their widespread adoption, mature technology, and broad applicability across numerous industries. These detectors feature a flat geometry and offer excellent energy resolution for low-energy X-ray and gamma-ray detection, making them ideal for material analysis, X-ray fluorescence (XRF), and electron spectroscopy. Their simple structure allows for cost-effective manufacturing and integration into both portable and stationary systems. The reliability, performance consistency, and established use in scientific research, environmental monitoring, and industrial quality control contribute significantly to their dominant market share.

Doped Si (Li) Detectors are designed to enhance sensitivity and performance by introducing specific impurities into the detector material. This controlled doping improves carrier mobility and enables better detection of specific energy ranges, which is valuable in high-precision fields like nuclear physics and radiation dosimetry. While these detectors offer technical advantages in specialized applications, their complexity and higher cost limit their broader commercial deployment compared to planar detectors.

Edge-Defined Si (Li) Detectors utilize specialized edge shaping and fabrication techniques to minimize leakage currents and maximize effective detector area. This improves energy resolution and reduces noise, which is beneficial in high-accuracy measurement settings such as synchrotron beamlines and precision X-ray imaging. Despite their technical advantages, the niche nature and higher manufacturing demands of edge-defined detectors restrict their market share relative to planar variants.

Post-Processed (EPPC) Detectors are advanced detectors that undergo additional treatments after fabrication to refine structural integrity and enhance operational performance. These detectors are typically used in demanding environments, such as aerospace applications, particle physics experiments, and other research-intensive fields. Although they offer superior detection capabilities, their high cost and complexity make them less viable for widespread use, especially when compared to the proven efficiency and affordability of planar Si(Li) detectors.

Segmentation Insights by Application

On the basis of application, the global si (li) detector market is bifurcated into medical imaging, industrial applications, and scientific applications.

Medical Imaging dominates the Si (Li) detector market owing to its critical role in providing high-resolution, low-energy X-ray and gamma-ray detection, which is essential for precise diagnostic imaging. Si (Li) detectors offer excellent energy discrimination and low noise performance, making them highly effective in advanced diagnostic tools such as X-ray fluorescence (XRF) imaging, mammography, and bone densitometry. Their ability to deliver clear, detailed images with reduced radiation dosage makes them particularly valuable in modern healthcare environments, where patient safety and diagnostic accuracy are paramount. The continuous growth of imaging procedures and technological advancements in radiology systems further reinforce the leading position of Si(Li) detectors in this segment.

Industrial Applications utilize Si (Li) detectors in various quality control, inspection, and process monitoring systems. These detectors are widely implemented in material identification, elemental analysis, and coating thickness measurement through techniques like X-ray fluorescence (XRF). Industries such as metallurgy, electronics, and aerospace benefit from the detectors’ precision in analyzing complex compositions and ensuring manufacturing consistency. While industrial use represents a substantial portion of the market, it remains secondary to the growing healthcare demand that propels the dominance of medical imaging.

Scientific Applications rely on Si (Li) detectors for high-resolution spectroscopy, radiation detection, and particle physics research. Their precise energy resolution is instrumental in experiments conducted in synchrotrons, space research, and academic labs. These applications often require customized detector configurations for specific experimental setups. Despite the technical significance and consistent usage of Si (Li) detectors in the scientific field, this segment is smaller in scale compared to the extensive demand and practical deployment found in medical imaging.

Si (Li) Detector Market: Regional Insights

- North America is expected to dominate the global market

North America dominates the Si (Li) Detector Market due to its advanced research infrastructure, strong presence of leading nuclear, semiconductor, and materials science institutions, and significant government funding for scientific instrumentation. The United States, in particular, leads in the adoption of Si (Li) detectors in X-ray spectroscopy, nuclear physics research, and homeland security applications. Government agencies such as the DOE and NASA, along with national laboratories and top-tier universities, contribute to sustained demand. Furthermore, the region benefits from the presence of major detector manufacturers and technology suppliers offering high-purity, cryogenically cooled Si (Li) systems used in both laboratory and field-based research settings.

Europe holds a substantial share of the Si (Li) Detector Market, driven by a strong scientific community engaged in advanced research at institutions such as CERN, as well as robust applications in industrial quality control and non-destructive testing. Countries like Germany, the UK, France, and Italy exhibit consistent demand across sectors including nuclear energy, aerospace, and materials analysis. The EU’s investment in collaborative scientific projects and precision instrumentation supports the continued expansion of this market. In addition, the European market is increasingly adopting compact, digital Si (Li) detector systems compatible with automated platforms.

Asia-Pacific is the fastest-growing region in the Si (Li) Detector Market, driven by expanding research activities and increasing investments in semiconductor and nuclear technology across China, Japan, South Korea, and India. China, in particular, is heavily investing in spectroscopic research and radiation monitoring, leading to greater deployment of Si (Li) detectors in academic, industrial, and defense applications. Japan and South Korea also exhibit strong demand, particularly in synchrotron radiation facilities and materials science research. With growing emphasis on scientific innovation and local production capabilities, the region is witnessing rapid adoption of high-resolution X-ray detectors and elemental analyzers.

Latin America shows emerging potential in the Si(Li) Detector Market, particularly in Brazil and Mexico, where the growth of nuclear medicine, industrial inspection, and environmental monitoring is driving interest in advanced detector technologies. Although the market remains niche and heavily reliant on imports, rising scientific research funding and regional collaborations with international laboratories are helping expand awareness and application scope of Si (Li) detectors.

Middle East and Africa represent developing regions in the Si (Li) Detector Market. Growth is concentrated in countries such as the UAE, Saudi Arabia, and South Africa, where rising investments in healthcare technology, oil and gas analysis, and academic research are beginning to create demand for high-precision detectors. While market penetration is still limited due to high costs and infrastructure gaps, ongoing efforts in nuclear energy programs and international partnerships in scientific instrumentation are expected to support gradual market development.

Si (Li) Detector Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the si (li) detector market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global si (li) detector market include:

- Hamamatsu Photonics

- Ketek

- Advacam

- Centronic

- Piezo Systems

- Sensors Unlimited

- Teledyne DALSA

- Xenon InstrumentsJEOL

- Mirion Technologies

- RMT

- e2v Scientific Instruments

- Amptek

- Thermo Fisher

- Shimadzu Corporation

- PGT

The global si (li) detector market is segmented as follows:

By Type

- Planar Si(Li) detectors

- Doped Si(Li) detectors

- Edge-defined

- post-processed (EPPC) detectors

By Application

- Medical imaging

- Industrial applications

- Scientific applications

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

1 Introduction to Research & Analysis Reports 1.1 Si(Li) Detector Market Definition 1.2 Market Segments 1.2.1 Market by Type 1.2.2 Market by Application 1.3 Global Si(Li) Detector Market Overview 1.4 Features & Benefits of This Report 1.5 Methodology & Sources of Information 1.5.1 Research Methodology 1.5.2 Research Process 1.5.3 Base Year 1.5.4 Report Assumptions & Caveats 2 Global Si(Li) Detector Overall Market Size 2.1 Global Si(Li) Detector Market Size: 2021 VS 2028 2.2 Global Si(Li) Detector Revenue, Prospects & Forecasts: 2017-2028 2.3 Global Si(Li) Detector Sales: 2017-2028 3 Company Landscape 3.1 Top Si(Li) Detector Players in Global Market 3.2 Top Global Si(Li) Detector Companies Ranked by Revenue 3.3 Global Si(Li) Detector Revenue by Companies 3.4 Global Si(Li) Detector Sales by Companies 3.5 Global Si(Li) Detector Price by Manufacturer (2017-2022) 3.6 Top 3 and Top 5 Si(Li) Detector Companies in Global Market, by Revenue in 2021 3.7 Global Manufacturers Si(Li) Detector Product Type 3.8 Tier 1, Tier 2 and Tier 3 Si(Li) Detector Players in Global Market 3.8.1 List of Global Tier 1 Si(Li) Detector Companies 3.8.2 List of Global Tier 2 and Tier 3 Si(Li) Detector Companies 4 Sights by Product 4.1 Overview 4.1.1 By Type - Global Si(Li) Detector Market Size Markets, 2021 & 2028 4.1.2 Large-area 4.1.3 Small-area 4.2 By Type - Global Si(Li) Detector Revenue & Forecasts 4.2.1 By Type - Global Si(Li) Detector Revenue, 2017-2022 4.2.2 By Type - Global Si(Li) Detector Revenue, 2023-2028 4.2.3 By Type - Global Si(Li) Detector Revenue Market Share, 2017-2028 4.3 By Type - Global Si(Li) Detector Sales & Forecasts 4.3.1 By Type - Global Si(Li) Detector Sales, 2017-2022 4.3.2 By Type - Global Si(Li) Detector Sales, 2023-2028 4.3.3 By Type - Global Si(Li) Detector Sales Market Share, 2017-2028 4.4 By Type - Global Si(Li) Detector Price (Manufacturers Selling Prices), 2017-2028 5 Sights By Application 5.1 Overview 5.1.1 By Application - Global Si(Li) Detector Market Size, 2021 & 2028 5.1.2 Gamma Spectroscopy 5.1.3 X-ray Spectroscopy 5.2 By Application - Global Si(Li) Detector Revenue & Forecasts 5.2.1 By Application - Global Si(Li) Detector Revenue, 2017-2022 5.2.2 By Application - Global Si(Li) Detector Revenue, 2023-2028 5.2.3 By Application - Global Si(Li) Detector Revenue Market Share, 2017-2028 5.3 By Application - Global Si(Li) Detector Sales & Forecasts 5.3.1 By Application - Global Si(Li) Detector Sales, 2017-2022 5.3.2 By Application - Global Si(Li) Detector Sales, 2023-2028 5.3.3 By Application - Global Si(Li) Detector Sales Market Share, 2017-2028 5.4 By Application - Global Si(Li) Detector Price (Manufacturers Selling Prices), 2017-2028 6 Sights by Region 6.1 By Region - Global Si(Li) Detector Market Size, 2021 & 2028 6.2 By Region - Global Si(Li) Detector Revenue & Forecasts 6.2.1 By Region - Global Si(Li) Detector Revenue, 2017-2022 6.2.2 By Region - Global Si(Li) Detector Revenue, 2023-2028 6.2.3 By Region - Global Si(Li) Detector Revenue Market Share, 2017-2028 6.3 By Region - Global Si(Li) Detector Sales & Forecasts 6.3.1 By Region - Global Si(Li) Detector Sales, 2017-2022 6.3.2 By Region - Global Si(Li) Detector Sales, 2023-2028 6.3.3 By Region - Global Si(Li) Detector Sales Market Share, 2017-2028 6.4 North America 6.4.1 By Country - North America Si(Li) Detector Revenue, 2017-2028 6.4.2 By Country - North America Si(Li) Detector Sales, 2017-2028 6.4.3 US Si(Li) Detector Market Size, 2017-2028 6.4.4 Canada Si(Li) Detector Market Size, 2017-2028 6.4.5 Mexico Si(Li) Detector Market Size, 2017-2028 6.5 Europe 6.5.1 By Country - Europe Si(Li) Detector Revenue, 2017-2028 6.5.2 By Country - Europe Si(Li) Detector Sales, 2017-2028 6.5.3 Germany Si(Li) Detector Market Size, 2017-2028 6.5.4 France Si(Li) Detector Market Size, 2017-2028 6.5.5 U.K. Si(Li) Detector Market Size, 2017-2028 6.5.6 Italy Si(Li) Detector Market Size, 2017-2028 6.5.7 Russia Si(Li) Detector Market Size, 2017-2028 6.5.8 Nordic Countries Si(Li) Detector Market Size, 2017-2028 6.5.9 Benelux Si(Li) Detector Market Size, 2017-2028 6.6 Asia 6.6.1 By Region - Asia Si(Li) Detector Revenue, 2017-2028 6.6.2 By Region - Asia Si(Li) Detector Sales, 2017-2028 6.6.3 China Si(Li) Detector Market Size, 2017-2028 6.6.4 Japan Si(Li) Detector Market Size, 2017-2028 6.6.5 South Korea Si(Li) Detector Market Size, 2017-2028 6.6.6 Southeast Asia Si(Li) Detector Market Size, 2017-2028 6.6.7 India Si(Li) Detector Market Size, 2017-2028 6.7 South America 6.7.1 By Country - South America Si(Li) Detector Revenue, 2017-2028 6.7.2 By Country - South America Si(Li) Detector Sales, 2017-2028 6.7.3 Brazil Si(Li) Detector Market Size, 2017-2028 6.7.4 Argentina Si(Li) Detector Market Size, 2017-2028 6.8 Middle East & Africa 6.8.1 By Country - Middle East & Africa Si(Li) Detector Revenue, 2017-2028 6.8.2 By Country - Middle East & Africa Si(Li) Detector Sales, 2017-2028 6.8.3 Turkey Si(Li) Detector Market Size, 2017-2028 6.8.4 Israel Si(Li) Detector Market Size, 2017-2028 6.8.5 Saudi Arabia Si(Li) Detector Market Size, 2017-2028 6.8.6 UAE Si(Li) Detector Market Size, 2017-2028 7 Manufacturers & Brands Profiles 7.1 JEOL 7.1.1 JEOL Corporate Summary 7.1.2 JEOL Business Overview 7.1.3 JEOL Si(Li) Detector Major Product Offerings 7.1.4 JEOL Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.1.5 JEOL Key News 7.2 Mirion Technologies 7.2.1 Mirion Technologies Corporate Summary 7.2.2 Mirion Technologies Business Overview 7.2.3 Mirion Technologies Si(Li) Detector Major Product Offerings 7.2.4 Mirion Technologies Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.2.5 Mirion Technologies Key News 7.3 RMT 7.3.1 RMT Corporate Summary 7.3.2 RMT Business Overview 7.3.3 RMT Si(Li) Detector Major Product Offerings 7.3.4 RMT Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.3.5 RMT Key News 7.4 e2v Scientific Instruments 7.4.1 e2v Scientific Instruments Corporate Summary 7.4.2 e2v Scientific Instruments Business Overview 7.4.3 e2v Scientific Instruments Si(Li) Detector Major Product Offerings 7.4.4 e2v Scientific Instruments Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.4.5 e2v Scientific Instruments Key News 7.5 Amptek 7.5.1 Amptek Corporate Summary 7.5.2 Amptek Business Overview 7.5.3 Amptek Si(Li) Detector Major Product Offerings 7.5.4 Amptek Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.5.5 Amptek Key News 7.6 Thermo Fisher 7.6.1 Thermo Fisher Corporate Summary 7.6.2 Thermo Fisher Business Overview 7.6.3 Thermo Fisher Si(Li) Detector Major Product Offerings 7.6.4 Thermo Fisher Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.6.5 Thermo Fisher Key News 7.7 Shimadzu Corporation 7.7.1 Shimadzu Corporation Corporate Summary 7.7.2 Shimadzu Corporation Business Overview 7.7.3 Shimadzu Corporation Si(Li) Detector Major Product Offerings 7.7.4 Shimadzu Corporation Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.7.5 Shimadzu Corporation Key News 7.8 PGT 7.8.1 PGT Corporate Summary 7.8.2 PGT Business Overview 7.8.3 PGT Si(Li) Detector Major Product Offerings 7.8.4 PGT Si(Li) Detector Sales and Revenue in Global (2017-2022) 7.8.5 PGT Key News 8 Global Si(Li) Detector Production Capacity, Analysis 8.1 Global Si(Li) Detector Production Capacity, 2017-2028 8.2 Si(Li) Detector Production Capacity of Key Manufacturers in Global Market 8.3 Global Si(Li) Detector Production by Region 9 Key Market Trends, Opportunity, Drivers and Restraints 9.1 Market Opportunities & Trends 9.2 Market Drivers 9.3 Market Restraints 10 Si(Li) Detector Supply Chain Analysis 10.1 Si(Li) Detector Industry Value Chain 10.2 Si(Li) Detector Upstream Market 10.3 Si(Li) Detector Downstream and Clients 10.4 Marketing Channels Analysis 10.4.1 Marketing Channels 10.4.2 Si(Li) Detector Distributors and Sales Agents in Global 11 Conclusion 12 Appendix 12.1 Note 12.2 Examples of Clients 12.3 Disclaimer

Inquiry For Buying

Si (Li) Detector

Request Sample

Si (Li) Detector