Grade II Polysilicon for Electronics Market Size, Share, and Trends Analysis Report

CAGR :

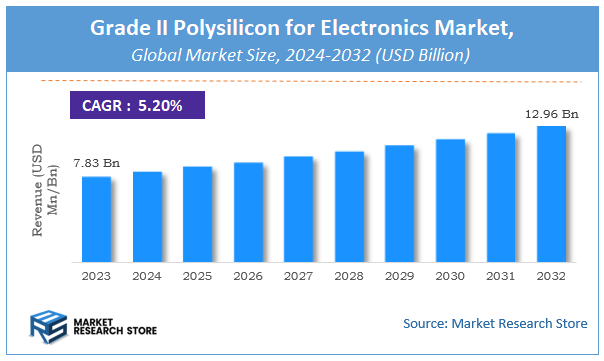

| Market Size 2023 (Base Year) | USD 7.83 Billion |

| Market Size 2032 (Forecast Year) | USD 12.96 Billion |

| CAGR | 5.2% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Grade II Polysilicon for Electronics Market Insights

According to Market Research Store, the global grade II polysilicon for electronics market size was valued at around USD 7.83 billion in 2023 and is estimated to reach USD 12.96 billion by 2032, to register a CAGR of approximately 5.20% in terms of revenue during the forecast period 2024-2032.

The grade II polysilicon for electronics report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Grade II Polysilicon for Electronics Market: Overview

Grade II polysilicon for electronics is a high-purity form of silicon used primarily in the manufacturing of semiconductor devices and solar cells. It is typically refined to meet specific quality standards, ensuring it meets the stringent requirements for electronic applications. This material plays a crucial role in the production of integrated circuits, transistors, and photovoltaic cells. The primary characteristics of grade II polysilicon include low levels of impurities and high crystallinity, which are essential for optimizing the performance of electronic components.

Key Highlights

- The grade II polysilicon for electronics market is anticipated to grow at a CAGR of 5.20% during the forecast period.

- The global grade II polysilicon for electronics market was estimated to be worth approximately USD 7.83 billion in 2023 and is projected to reach a value of USD 12.96 billion by 2032.

- The growth of the grade II polysilicon for electronics market is being driven by the increasing demand for advanced semiconductors in various sectors, including consumer electronics, automotive, and telecommunications.

- Based on the type, the trichlorosilane method segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the 300mm Wafer segment is projected to swipe the largest market share.

- By region, Asia-Pacific is expected to dominate the global market during the forecast period.

Grade II Polysilicon for Electronics Market: Dynamics

Key Growth Drivers:

- Rising Demand for Electronics: The ever-increasing demand for electronic devices like smartphones, laptops, and IoT devices is a major driver for the Grade II polysilicon market. These devices require advanced semiconductors, which rely heavily on high-purity polysilicon.

- Advancements in Semiconductor Technology: The continuous evolution of semiconductor technology, such as the development of smaller and more powerful chips, necessitates the use of higher-quality polysilicon with improved purity levels.

- Growth of Renewable Energy: The expanding solar energy sector is also driving demand for Grade II polysilicon, as it is a crucial component in the manufacturing of solar cells and panels.

- Increasing Government Support: Many governments are actively promoting the development of the semiconductor industry through various incentives and subsidies, which is expected to further boost the demand for Grade II polysilicon.

Restraints:

- High Production Costs: The production of high-purity polysilicon is an energy-intensive and complex process, leading to high production costs.

- Supply Chain Disruptions: The global supply chain has been facing disruptions due to various factors, including geopolitical tensions and natural disasters. These disruptions can impact the availability and pricing of raw materials, including polysilicon.

- Price Fluctuations: The price of polysilicon can fluctuate significantly due to factors such as supply and demand imbalances, changes in energy costs, and geopolitical events.

- Environmental Concerns: The production of polysilicon can have environmental impacts, such as greenhouse gas emissions and water pollution.

Opportunities:

- Development of New Applications: The emergence of new technologies, such as electric vehicles, artificial intelligence, and 5G, is creating new opportunities for the use of Grade II polysilicon in various applications.

- Technological Advancements in Production: Ongoing research and development efforts are focused on improving the efficiency and reducing the environmental impact of polysilicon production processes.

- Regional Market Growth: The demand for electronics and semiconductors is growing rapidly in emerging economies, offering significant growth opportunities for the Grade II polysilicon market.

- Recycling and Reuse: The development of effective recycling and reuse technologies for polysilicon can help to reduce waste and conserve resources.

Challenges:

- Competition: The Grade II polysilicon market is characterized by intense competition among a limited number of major players.

- Technological Advancements: The rapid pace of technological advancements in the semiconductor industry requires continuous innovation and investment to remain competitive.

- Environmental Regulations: Increasingly stringent environmental regulations can pose challenges for polysilicon manufacturers, requiring them to invest in pollution control technologies.

- Intellectual Property Rights: Protecting intellectual property rights related to new production technologies and applications can be a significant challenge for companies operating in the Grade II polysilicon market.

Grade II Polysilicon for Electronics Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Grade II Polysilicon for Electronics Market |

| Market Size in 2023 | USD 7.83 Billion |

| Market Forecast in 2032 | USD 12.96 Billion |

| Growth Rate | CAGR of 5.2% |

| Number of Pages | 140 |

| Key Companies Covered | Tokuyama, Wacker Chemie, Hemlock Semiconductor, Mitsubishi Materials, OSAKA Titanium Technologies, OCI, REC Silicon, GCL-Poly Energy, Huanghe Hydropower, Yichang CSG |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Grade II Polysilicon for Electronics Market: Segmentation Insights

The global grade II polysilicon for electronics market is divided by type, application, and region.

Segmentation Insights by Type

Based on type, the global grade II polysilicon for electronics market is divided into trichlorosilane method, silicon tetrachloride, dichlorodihydro silicon method, silane method, and other.

In the grade II polysilicon for electronics market, the most dominating segment is the Trichlorosilane (TCS) Method, which is the primary method for producing polysilicon used in electronics. This method is widely adopted due to its cost-effectiveness and ability to produce high-purity polysilicon, which is essential for electronic applications. The Trichlorosilane method involves the reduction of silicon tetrachloride (SiCl4) using hydrogen, resulting in high-quality polysilicon suitable for semiconductors and other electronic devices.

The Silicon Tetrachloride method follows as the second most dominant, although it is slightly less prevalent than the TCS method. In this process, silicon tetrachloride is reduced with hydrogen to produce polysilicon. While it offers a comparable level of purity, it is considered less efficient and more expensive than the TCS method, which has limited its widespread adoption in electronics compared to other methods.

Next, the Dichlorodihydro Silicon Method is also used in polysilicon production but is less dominant in the electronics sector. This method involves the reaction of silicon tetrachloride with hydrogen to form polysilicon, similar to the TCS method but with some variations in the intermediate chemicals. While it provides high-quality polysilicon, its complexity and slightly higher production costs make it less attractive for large-scale electronic applications.

The Silane Method is also used for producing polysilicon but is less popular in the grade II segment for electronics. In this method, silane gas (SiH4) is decomposed at high temperatures to deposit polysilicon. While it can produce high-purity polysilicon, the process is typically less efficient and more costly, which has limited its use in the production of grade II polysilicon.

Segmentation Insights by Application

On the basis of application, the global grade II polysilicon for electronics market is bifurcated into 300mm wafer, 200mm wafer, and others.

In the grade II polysilicon for electronics market, the 300mm Wafer application is the most dominant segment. This size is critical in semiconductor manufacturing, particularly for advanced electronics, including microchips and integrated circuits. The 300mm wafer has become the industry standard for high-volume production, offering more efficiency and reduced costs per unit area compared to smaller wafers. This makes it the preferred choice for large-scale manufacturers of semiconductors and electronics, driving the demand for polysilicon suitable for 300mm wafers.

The 200mm Wafer segment follows as the second-largest application. While it has been largely replaced by 300mm wafers in many modern semiconductor fabs, 200mm wafers are still widely used in niche applications, such as low to medium volume production and legacy products. Polysilicon used for 200mm wafers tends to be less expensive, making it more suitable for applications where cutting-edge technology is not required but reliability and cost-effectiveness are important. Despite the rise of 300mm wafers, 200mm wafers still hold a significant share, especially in mature markets or specific industrial sectors.

Grade II Polysilicon for Electronics Market: Regional Insights

- Asia-Pacific is expected to dominates the global market

Asia-Pacific leads the global market for Grade II polysilicon used in electronics, driven by significant production capacities in countries like China, South Korea, and Taiwan. The region's dominance is largely due to its rapid expansion in solar photovoltaic installations, which has substantially increased the demand for high-purity polysilicon. China, in particular, has emerged as a major producer, with substantial investments in polysilicon manufacturing, contributing to its leading position in the market.

North America holds the second-largest share in the Grade II polysilicon market, with the United States and Canada being key contributors. The region's demand is primarily driven by the growing renewable energy sector, which relies heavily on high-quality polysilicon for solar cell production. Additionally, the presence of several major polysilicon producers in North America supports the region's significant market share.

Europe ranks third in the Grade II polysilicon market, with countries such as Germany and Italy playing pivotal roles. The region's commitment to reducing carbon emissions and transitioning to renewable energy sources has spurred the demand for high-purity polysilicon. Europe's robust renewable energy policies and incentives have further bolstered the market for Grade II polysilicon in the region.

South America, including countries like Brazil and Argentina, has a smaller yet growing presence in the Grade II polysilicon market. The region's demand is influenced by emerging renewable energy projects and a gradual shift towards solar energy adoption. While the market share is currently limited, ongoing investments and supportive policies are expected to drive future growth in the South American market.

The Middle East and Africa region, encompassing nations such as Saudi Arabia, the UAE, and South Africa, has the smallest share in the Grade II polysilicon market. The demand in this region is primarily driven by the early stages of renewable energy development and the implementation of large-scale solar projects. Despite the current modest market size, the region's strategic initiatives to diversify energy sources and invest in renewable technologies indicate potential for future growth in the Grade II polysilicon market.

Grade II Polysilicon for Electronics Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the grade II polysilicon for electronics market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global grade II polysilicon for electronics market include:

- Tokuyama

- Wacker Chemie

- Hemlock Semiconductor

- Mitsubishi Materials

- OSAKA Titanium Technologies

- OCI

- REC Silicon

- GCL-Poly Energy

- Huanghe Hydropower

- Yichang CSG

The global grade II polysilicon for electronics market is segmented as follows:

By Type

- Trichlorosilane Method

- Silicon Tetrachloride

- Dichlorodihydro Silicon Method

- Silane Method

- Other

By Application

- 300mm Wafer

- 200mm Wafer

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global grade II polysilicon for electronics market size was projected at approximately US$ 7.83 billion in 2023. Projections indicate that the market is expected to reach around US$ 12.96 billion in revenue by 2032.

The global grade II polysilicon for electronics market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 5.20% during the forecast period from 2024 to 2032.

Asia-Pacific is expected to dominate the global grade II polysilicon for electronics market.

The global grade II polysilicon for electronics market is driven by the growing demand for advanced semiconductors in consumer electronics, automotive, and telecommunications sectors, as well as the expansion of the renewable energy industry, particularly in solar power production. Additionally, advancements in electronic technologies and miniaturization further contribute to market growth.

Some of the prominent players operating in the global grade II polysilicon for electronics market are; Tokuyama, Wacker Chemie, Hemlock Semiconductor, Mitsubishi Materials, OSAKA Titanium Technologies, OCI, REC Silicon, GCL-Poly Energy, Huanghe Hydropower, Yichang CSG, and others.

Table Of Content

Inquiry For Buying

Grade II Polysilicon for Electronics

Request Sample

Grade II Polysilicon for Electronics