Modular Automation Market Size, Share, and Trends Analysis Report

CAGR :

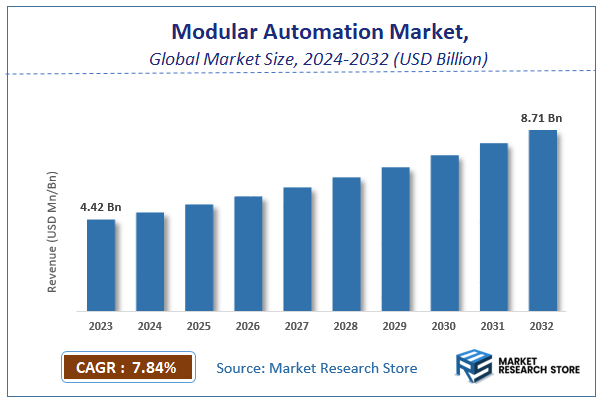

| Market Size 2023 (Base Year) | USD 4.42 Billion |

| Market Size 2032 (Forecast Year) | USD 8.71 Billion |

| CAGR | 7.84% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Modular Automation Market Insights

According to Market Research Store, the global modular automation market size was valued at around USD 4.42 billion in 2023 and is estimated to reach USD 8.71 billion by 2032, to register a CAGR of approximately 7.84% in terms of revenue during the forecast period 2024-2032.

The modular automation report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Modular Automation Market: Overview

Modular automation is a design approach that breaks down industrial automation systems into smaller, self-contained, and interchangeable modules. Each module performs a specific function, such as control, sensing, or actuation, and can be easily integrated, replaced, or reconfigured as needed. This flexibility allows for scalability, reduced downtime, and cost efficiency, making it ideal for industries with evolving production needs, such as manufacturing, automotive, and pharmaceuticals. Modular automation leverages standardized hardware and software components, enabling seamless communication and interoperability across systems.

Key Highlights

- The modular automation market is anticipated to grow at a CAGR of 7.84% during the forecast period.

- The global modular automation market was estimated to be worth approximately USD 4.42 billion in 2023 and is projected to reach a value of USD 8.71 billion by 2032.

- The growth of the modular automation market is being driven by the increasing demand for flexible and efficient production systems, particularly in industries adopting Industry 4.0 and smart manufacturing practices.

- Based on the type, the distributed control system segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the medical segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

Modular Automation Market: Dynamics

Key Growth Drivers:

- Increased Need for Flexibility and Scalability: Modern manufacturing and other industries require flexible production systems that can be easily adapted to changing product demands and volumes. Modular automation offers this scalability.

- Rising Labor Costs and Shortages: Automation, including modular solutions, helps reduce reliance on manual labor, addressing rising labor costs and the increasing shortage of skilled workers.

- Technological Advancements: Advancements in robotics, sensors, and control systems are enabling more sophisticated and efficient modular automation solutions.

- Growing Adoption of Industry 4.0: The push towards smart factories and interconnected systems is driving the adoption of modular automation, which integrates well with these concepts.

- Reduced Downtime and Increased Productivity: Modular systems can be quickly reconfigured or repaired, minimizing downtime and maximizing production output.

Restraints:

- High Initial Investment Costs: Implementing modular automation solutions can require significant upfront investment, which may be a barrier for smaller businesses.

- Complexity of Integration: Integrating modular components from different vendors can be complex and require specialized expertise.

- Need for Skilled Personnel: Designing, implementing, and maintaining modular automation systems requires skilled engineers and technicians.

- Concerns about Job Displacement: The automation trend, including modular solutions, can raise concerns about potential job losses in certain sectors.

- Limited Standardization: Lack of complete standardization in modular components can sometimes hinder seamless integration.

Opportunities:

- Growing Demand from SMEs: Small and medium-sized enterprises are increasingly adopting modular automation to improve efficiency and competitiveness.

- Expansion in Emerging Markets: Developing economies are investing in automation technologies to boost manufacturing and other industries, creating new market opportunities.

- Development of Collaborative Robots (Cobots): Cobots are designed to work alongside humans, making modular automation more accessible and adaptable in various settings.

- Focus on Customization: Modular solutions can be tailored to specific customer needs and applications, offering a competitive advantage.

- Cloud-Based Monitoring and Control: Cloud technologies are enabling remote monitoring and control of modular automation systems, improving efficiency and maintenance.

Challenges:

- Maintaining Flexibility and Adaptability: While modular systems offer flexibility, ensuring they can be easily reconfigured for future needs can be a challenge.

- Ensuring System Reliability: Integrating multiple modules from different vendors can sometimes pose challenges in ensuring overall system reliability.

- Cybersecurity Risks: As automation systems become more connected, cybersecurity risks become a concern, requiring robust security measures.

- Return on Investment (ROI) Justification: Demonstrating a clear return on investment for modular automation projects can be crucial for securing funding.

- Competition: The modular automation market is becoming increasingly competitive, with several established players and new entrants.

Modular Automation Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | Modular Automation Market |

| Market Size in 2023 | USD 4.42 Billion |

| Market Forecast in 2032 | USD 8.71 Billion |

| Growth Rate | CAGR of 7.84% |

| Number of Pages | 140 |

| Key Companies Covered | ABB (Switzerland), Festo Inc. (Germany), Yokogawa Electric Corporation (Japan), Siemens (Germany), HIMA (Germany), Bosch Rexroth AG (Germany), Modular Automation (Ireland), Ascential Technologies (US), Ginolis OY (Finland), Inniti (Denmark) are the major |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Modular Automation Market: Segmentation Insights

The global modular automation market is divided by type, application, and region.

Segmentation Insights by Type

Based on type, the global modular automation market is divided into distributed control system and module type packages.

The Distributed Control System (DCS) segment dominates the modular automation market due to its widespread adoption in large-scale industrial operations. DCS is preferred in industries such as oil & gas, chemical processing, power generation, and pharmaceuticals, where complex processes require centralized control with high reliability and scalability. These systems allow seamless integration of multiple subsystems while offering real-time monitoring, advanced analytics, and remote-control capabilities. The ability to enhance operational efficiency, reduce downtime, and improve safety standards makes DCS the preferred choice for industries with extensive automation needs.

The Module Type Packages segment, while less dominant, plays a crucial role in industries that require flexible and scalable automation solutions. These packages are designed for smaller-scale applications and modular production environments, such as food & beverage, automotive, and electronics manufacturing. They provide cost-effective and easy-to-deploy solutions, making them ideal for businesses that need adaptable automation without investing in large-scale infrastructure. Though growing in adoption, Module Type Packages are more commonly used in applications where rapid reconfiguration and customization are necessary, but they do not yet match the extensive implementation of DCS in heavy industries.

Segmentation Insights by Application

On the basis of application, the global modular automation market is bifurcated into medical, cosmetics, FMCG, and energy.

The Medical segment is the most dominant in the modular automation market, driven by the increasing demand for precision, efficiency, and regulatory compliance in pharmaceutical and medical device manufacturing. Modular automation enables seamless adaptation to new drug formulations, personalized medicine, and stringent safety standards. The pharmaceutical industry, in particular, benefits from modular automation to streamline production, minimize contamination risks, and ensure consistent quality. With the growing emphasis on automation in healthcare, this segment continues to see significant investment and expansion.

The Cosmetics industry follows closely, leveraging modular automation for efficient and flexible production of skincare, makeup, and personal care products. The need for quick adaptation to changing consumer trends and product formulations makes modular automation a valuable asset for cosmetic manufacturers. Automated systems help maintain consistency, enhance productivity, and reduce operational costs while enabling companies to scale production based on demand.

The Fast-Moving Consumer Goods (FMCG) sector is another major adopter of modular automation, particularly in the packaging and processing of food, beverages, and household products. As consumer preferences shift toward sustainability and customized packaging, modular automation offers companies the agility to modify production lines efficiently. However, compared to the medical and cosmetics industries, FMCG faces fewer regulatory constraints, which affects the urgency of automation adoption in some cases.

The Energy sector, while the least dominant in this market, is gradually incorporating modular automation, particularly in renewable energy production and industrial energy management. Automation is being used to optimize processes in battery manufacturing, solar panel production, and smart grid management. However, the adoption rate remains slower due to the high initial costs and the traditionally slower pace of technological change in energy infrastructure. Nonetheless, as the energy sector moves toward digital transformation and sustainability, modular automation is expected to gain traction in the long term.

Modular Automation Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the modular automation market, driven by the widespread adoption of advanced manufacturing technologies and Industry 4.0 practices. The region benefits from a strong industrial base, particularly in the automotive, aerospace, and pharmaceutical sectors, which heavily rely on flexible and scalable automation solutions. The presence of major market players and significant investments in research and development further solidify North America's leading position. Additionally, the push for smart factories and the integration of IoT and AI in manufacturing processes have accelerated the demand for modular automation systems, making it the most advanced and mature market globally.

Europe follows closely, holding a significant share of the modular automation market. The region's emphasis on industrial automation, coupled with stringent regulations promoting energy efficiency and sustainability, has driven the adoption of modular systems. Countries like Germany, France, and Italy are at the forefront, with their strong manufacturing sectors and focus on precision engineering. The automotive industry, in particular, has been a major contributor to the growth of modular automation in Europe. The region's commitment to digital transformation and smart manufacturing initiatives has further bolstered the market, making it a key player in the global landscape.

Asia-Pacific is the fastest-growing region in the modular automation market, fueled by rapid industrialization and increasing investments in automation technologies. Countries like China, Japan, South Korea, and India are leading the charge, with their expanding manufacturing sectors and growing adoption of Industry 4.0 practices. The region's large population and rising labor costs have prompted industries to shift toward automated solutions to enhance productivity and reduce operational expenses. Government initiatives promoting smart manufacturing and the presence of a robust electronics and automotive industry have further accelerated market growth. While still developing compared to North America and Europe, Asia-Pacific is poised to become a major hub for modular automation in the coming years.

The Middle East and Africa represent a smaller but growing segment of the modular automation market. The region's growth is primarily driven by the oil and gas industry, which is increasingly adopting automation technologies to improve efficiency and reduce downtime. Countries like Saudi Arabia, the UAE, and South Africa are investing in industrial automation to diversify their economies and modernize their manufacturing sectors. However, the market is still in its nascent stages compared to other regions, with limited adoption in other industries. Despite this, the region shows potential for growth as awareness of modular automation benefits increases and infrastructure development continues.

Latin America, while having a relatively smaller market share, is gradually adopting modular automation technologies. The region's growth is driven by industries such as food and beverage, automotive, and mining, which are increasingly focusing on improving operational efficiency. Countries like Brazil and Mexico are leading the adoption of automation solutions, supported by government initiatives and foreign investments. However, economic instability and limited technological infrastructure in some areas have slowed the pace of adoption. Nonetheless, the region is expected to witness steady growth as industries recognize the value of modular automation in enhancing productivity and competitiveness.

Recent Developments:

- In January 2024, FANUC America opened a new 461,000-square-foot, $200 million facility in Auburn Hills, Michigan, to expand its modular automation capabilities. The plant focuses on next-generation robotics and flexible manufacturing solutions, featuring advanced testing and demonstration spaces.

- In March 2024, Siemens updated its Digital Enterprise Suite, enhancing modular automation with advanced digital twin technology and improved integration. The update enables 40% faster production line reconfiguration. Siemens also partnered with major automakers to implement these solutions globally.

Modular Automation Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the modular automation market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global modular automation market include:

- Hitachi

- Beckman

- Tecan

- Roche

- Abbot

- Thermo Fisher

- Tomtec

- Mindry

- Siemens AG

- Rockwell Automation

- ABB Ltd.

- Mitsubishi Electric Corporation

- Schneider Electric

- Emerson Electric

- Honeywell International

- Bosch Rexroth

- Festo AG

- Yokogawa Electric Corporation

The global modular automation market is segmented as follows:

By Type

- Distributed Control System

- Module Type Packages

By Application

- Medical

- Cosmetics

- FMCG

- Energy

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Based on statistics from the Market Research Store, the global modular automation market size was projected at approximately US$ 4.42 billion in 2023. Projections indicate that the market is expected to reach around US$ 8.71 billion in revenue by 2032.

The global modular automation market is expected to grow at a Compound Annual Growth Rate (CAGR) of around 7.84% during the forecast period from 2024 to 2032.

North America is expected to dominate the global modular automation market.

The global modular automation market is driven by the increasing adoption of Industry 4.0 and smart manufacturing practices, demand for flexible and scalable production systems, and advancements in IoT, AI, and robotics. Additionally, the need for reduced downtime, cost efficiency, and improved operational productivity across industries like automotive, pharmaceuticals, and electronics further fuels market growth.

Some of the prominent players operating in the global modular automation market are; Hitachi, Beckman, Tecan, Roche, Abbot, Thermo Fisher, Tomtec, Mindry, Siemens AG, Rockwell Automation, ABB Ltd., Mitsubishi Electric Corporation, Schneider Electric, Emerson Electric, Honeywell International, Bosch Rexroth, Festo AG, Yokogawa Electric Corporation, and others.

Table Of Content

Inquiry For Buying

Modular Automation

Request Sample

Modular Automation