PC Films Market Size, Share, and Trends Analysis Report

CAGR :

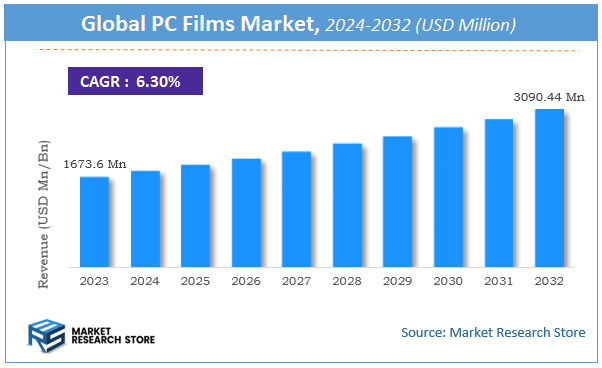

| Market Size 2023 (Base Year) | USD 1673.6 Million |

| Market Size 2032 (Forecast Year) | USD 3090.44 Million |

| CAGR | 6.3% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

PC Films Market Insights

According to Market Research Store, the global pc films market size was valued at around USD 1673.6 billion in 2023 and is estimated to reach USD 3090.44 billion by 2032, to register a CAGR of approximately 6.3% in terms of revenue during the forecast period 2024-2032.

The pc films report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global PC Films Market: Overview

The PC Films (Polycarbonate Films) market is experiencing steady growth, driven by increasing demand for high-performance, durable, and lightweight materials across various industries. Polycarbonate films offer exceptional optical clarity, impact resistance, heat resistance, and flexibility, making them ideal for applications in electronics, automotive, medical, packaging, and security industries. These films are widely used in applications such as display screens, control panels, ID cards, labels, automotive interior components, and medical packaging.

Market expansion is fueled by the rising adoption of polycarbonate films in consumer electronics, where they are used for protective films on touchscreens, membrane switches, and flexible printed circuits. The automotive industry is another key driver, with PC films being used in instrument panels, head-up displays, and lightweight interior components to enhance durability and aesthetic appeal. Additionally, the growing focus on sustainable and recyclable materials has led to increased research and development in eco-friendly PC film alternatives.

Key Highlights

- The pc films market is anticipated to grow at a CAGR of 6.3% during the forecast period.

- The global pc films market was estimated to be worth approximately USD 1673.6 billion in 2023 and is projected to reach a value of USD 3090.44 billion by 2032.

- The growth of the pc films market is being driven by the increasing demand for high-performance, versatile materials across various industries.

- Based on the product, the optical pc films segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the electrical and electronics segment is projected to swipe the largest market share.

- By region, North America is expected to dominate the global market during the forecast period.

PC Films Market: Dynamics

Key Drivers

- Versatile Applications: PC films find use in diverse industries, including electronics, automotive, medical, and packaging. This broad applicability is a major driver. Think of everything from smartphone screens to car dashboards.

- Excellent Optical Properties: PC films offer high clarity, light transmission, and gloss, making them suitable for applications requiring visual appeal and optical performance. This is key for displays and lenses.

- High Impact Resistance: PC films exhibit excellent impact resistance and toughness, making them ideal for protective applications and durable goods. This is why they're used in safety glasses and automotive parts.

- Heat Resistance and Dimensional Stability: PC films have good heat resistance and dimensional stability, allowing them to be used in applications exposed to temperature variations. This is important for electronic devices.

- Lightweighting: Compared to glass, PC films are lighter, contributing to weight reduction in various products, especially important in transportation and portable electronics.

Restraints

- Cost: PC films can be more expensive than some other plastic films, which can be a barrier for price-sensitive applications.

- Scratch Susceptibility: PC films are prone to scratching, which can limit their use in some applications without protective coatings.

- Chemical Sensitivity: Certain chemicals can damage or degrade PC films, requiring careful selection of cleaning agents and limiting their use in some environments.

- Processing Challenges: Processing PC films can sometimes be more complex than other plastics, requiring specialized equipment and expertise.

Opportunities

- Development of Advanced Coatings: Research and development of new coatings, such as anti-scratch coatings, anti-glare coatings, UV-resistant coatings, and conductive coatings, can enhance the performance and functionality of PC films, expanding their applications.

- Focus on Sustainable Materials: Growing demand for sustainable materials presents an opportunity for bio-based or recycled PC films, appealing to environmentally conscious consumers and businesses.

- Expanding into New Applications: Exploring new and emerging applications for PC films, such as in flexible electronics, wearable devices, and advanced medical devices.

- Customization and Formulation: Offering customized PC film solutions, including different thicknesses, colors, textures, and properties, to meet specific customer requirements.

Challenges

- Maintaining Product Quality and Consistency: Ensuring consistent quality and properties across different batches of PC films is crucial for maintaining customer satisfaction and meeting industry standards.

- Improving Scratch Resistance: Enhancing the scratch resistance of PC films remains a key challenge for expanding their use in certain applications.

- Competing with Other Materials: PC films face competition from other materials, such as glass, acrylic, and other plastic films, requiring manufacturers to continuously innovate and offer competitive pricing.

- Meeting Evolving Regulatory Requirements: Complying with evolving safety and environmental regulations related to the production and use of PC films.

PC Films Market: Report Scope

| Report Attributes | Report Details |

|---|---|

| Report Name | PC Films Market |

| Market Size in 2023 | USD 1673.6 Million |

| Market Forecast in 2032 | USD 3090.44 Million |

| Growth Rate | CAGR of 6.3% |

| Number of Pages | 177 |

| Key Companies Covered | Covestro, GE Plastics, U.S. Plastic, Mitsubishi Gas Chemical, Teijin Chemicals, OMAY, Rowland Technologies, Plastronics, SABIC, Wiman |

| Segments Covered | By Product Type, By Application, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

PC Films Market: Segmentation Insights

The global pc films market is divided by product, application, and region.

Segmentation Insights by Product

Based on product, the global pc films market is divided into optical pc films, flame retardant pc films, and weatherable pc films.

The Optical PC Films segment dominates the PC films market, driven by its extensive use in consumer electronics, automotive displays, and high-performance optical applications. These films offer superior light transmission, anti-glare properties, and impact resistance, making them essential in the production of LCD panels, touchscreen devices, and instrument clusters. As the demand for high-definition displays and durable optical components continues to rise, this segment is expected to witness significant growth.

The Flame Retardant PC Films segment plays a crucial role in applications requiring enhanced fire resistance, particularly in the electrical and electronics industries. These films are widely used for insulation, printed circuit boards (PCBs), and battery protection due to their ability to withstand high temperatures while maintaining mechanical integrity. The growing emphasis on fire safety regulations and stringent industry standards further fuels the adoption of flame-retardant PC films.

The Weatherable PC Films segment caters to outdoor applications where resistance to UV radiation, moisture, and harsh environmental conditions is critical. These films are commonly used in automotive exteriors, signage, and construction materials, where prolonged exposure to sunlight and weathering can degrade standard plastic materials. The increasing demand for durable and long-lasting materials in outdoor applications is expected to support steady growth in this segment.

Segmentation Insights by Application

On the basis of application, the global pc films market is bifurcated into electrical and electronics, automotive, construction, and others.

The Electrical and Electronics segment dominates the PC films market, primarily due to the increasing demand for high-performance materials in consumer electronics, display panels, and electrical insulation. Polycarbonate films are widely used in touchscreens, membrane switches, circuit boards, and flexible displays due to their excellent optical clarity, impact resistance, and heat stability. The rapid advancements in electronics, coupled with the growing adoption of smart devices, are expected to drive further demand for PC films in this segment.

The Automotive segment is witnessing significant growth as PC films are extensively utilized in vehicle interiors, instrument panels, and lighting applications. These films offer superior scratch resistance, anti-glare properties, and lightweight characteristics, making them ideal for modern automotive designs focused on durability and aesthetics. The increasing integration of digital displays and infotainment systems in vehicles further supports the expansion of this segment.

The Construction segment benefits from PC films' high impact strength, weather resistance, and durability, making them a preferred choice for applications such as protective glazing, signage, and interior decorations. The rising adoption of energy-efficient and shatter-resistant materials in modern architecture, along with stringent building safety regulations, continues to drive demand for PC films in the construction industry.

PC Films Market: Regional Insights

- North America is expected to dominates the global market

North America dominates the PC Films Market, driven by strong demand in electronics, automotive, and healthcare industries. The United States is the largest contributor, with widespread adoption of PC films in touchscreen displays, medical packaging, and high-durability automotive components. The increasing use of polycarbonate films in security applications, such as ID cards, passports, and smart cards, is a significant growth factor. Additionally, the growing demand for PC films in protective coatings for consumer electronics, including smartphones and tablets, is fueling market expansion. Canada is also experiencing growth, particularly in industrial applications where PC films are used for protective barriers and safety shields. The region’s strong focus on sustainable and recyclable materials is pushing innovation in eco-friendly PC film production.

Europe is another key market, supported by stringent environmental regulations, increasing adoption of high-performance display films, and rising demand in automotive and industrial applications. Germany, the UK, and France are major contributors. Germany, with its strong automotive sector, is witnessing increased use of PC films in interior panels, instrument clusters, and head-up displays (HUDs). France is seeing growing demand for security and anti-counterfeit films in banking and government sectors, while the UK’s electronics and medical industries are driving adoption of polycarbonate films in flexible screens and protective medical packaging. Europe’s emphasis on sustainable and lightweight materials is fostering the development of bio-based and recyclable PC films, further enhancing market growth.

Asia Pacific is the fastest-growing region in the PC Films Market, fueled by rapid industrialization, expanding electronics manufacturing, and increasing demand in the automotive and packaging sectors. China, Japan, South Korea, and India are major markets. China, the largest electronics producer, is driving demand for PC films in LCD displays, flexible screens, and protective films for electronic devices. The country’s booming automotive industry is also increasing the adoption of PC films in vehicle interiors and transparent glazing. Japan and South Korea, home to leading display technology manufacturers, are witnessing high demand for advanced optical-grade polycarbonate films in OLED and flexible display applications. India’s rising demand for high-durability packaging and protective films in healthcare and retail sectors is further fueling market growth. Additionally, increasing government regulations in Asia Pacific promoting sustainable packaging solutions are driving innovations in recyclable PC films.

Latin America is experiencing moderate growth, with Brazil and Mexico leading the market. The demand for PC films in the region is primarily driven by the expanding automotive industry, growing use of protective films in security applications, and increasing adoption in the electronics sector. Brazil’s automotive sector is incorporating more PC films in interior trims and instrument panels, while Mexico’s manufacturing sector is seeing increased demand for high-performance PC films in electronic components and industrial packaging. The growing middle class and rising demand for durable consumer electronics are also contributing to market expansion. However, economic instability and fluctuations in raw material prices may pose challenges to market growth in some Latin American countries.

The Middle East & Africa is witnessing steady market expansion, particularly in the UAE, Saudi Arabia, and South Africa. The region’s growing infrastructure and construction industry are driving demand for PC films in protective glazing and security applications. The increasing use of polycarbonate films in high-security documents, such as passports and national IDs, is another key growth factor. The Middle East’s luxury retail market is also contributing to demand for PC films in premium packaging and branding applications. However, limited local production capacities and dependency on imports may impact market dynamics in some parts of the region.

PC Films Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the pc films market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global pc films market include:

- Covestro

- GE Plastics

- Mitsubishi Gas Chemical

- OMAY

- Plastronics

- Rowland Technologies

- SABIC

- Teijin Chemicals

- U.S. Plastic

- Wiman

The global pc films market is segmented as follows:

By Product

- Optical PC Films

- Flame Retardant PC Films

- Weatherable PC Films

- Others

By Application

- Electrical and Electronics

- Automotive

- Construction

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

PC Films

Request Sample

PC Films