Silicon Carbide Coating Market Size, Share, and Trends Analysis Report

CAGR :

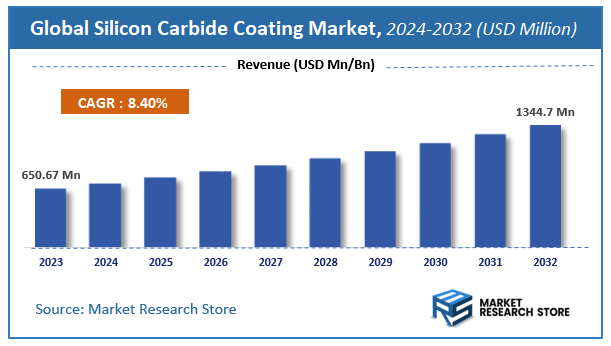

| Market Size 2023 (Base Year) | USD 650.67 Million |

| Market Size 2032 (Forecast Year) | USD 1344.7 Million |

| CAGR | 8.4% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Silicon Carbide Coating Market Insights

According to Market Research Store, the global silicon carbide coating market size was valued at around USD 650.67 million in 2023 and is estimated to reach USD 1344.7 million by 2032, to register a CAGR of approximately 8.4% in terms of revenue during the forecast period 2024-2032.

The silicon carbide coating report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

.Global Silicon Carbide Coating Market: Overview

Silicon carbide (SiC) coating is a high-performance protective layer made from silicon and carbon atoms, applied to various substrates to enhance their resistance to extreme temperatures, wear, corrosion, and chemical degradation. This ceramic coating is known for its exceptional hardness, thermal stability, and chemical inertness, making it ideal for use in demanding industrial environments such as aerospace, semiconductors, energy, automotive, and chemical processing. Silicon carbide coatings are commonly applied through chemical vapor deposition (CVD), physical vapor deposition (PVD), or thermal spraying techniques, and are used to coat components such as heat exchangers, mechanical seals, wafer carriers, and furnace parts.

Key Highlights

- The silicon carbide coating market is anticipated to grow at a CAGR of 8.4% during the forecast period.

- The global silicon carbide coating market was estimated to be worth approximately USD 650.67 million in 2023 and is projected to reach a value of USD 1344.7 million by 2032.

- The growth of the silicon carbide coating market is being driven by rising demand from industries requiring high durability and thermal performance materials.

- Based on the product type, the polycrystalline silicon carbide segment is growing at a high rate and is projected to dominate the market.

- On the basis of application, the aerospace segment is projected to swipe the largest market share.

- In terms of end-user, the mining & metallurgy segment is expected to dominate the market.

- Based on the functionality, the corrosion resistance segment is expected to dominate the market.

- In terms of form, the powder coating segment is expected to dominate the market.

- By region, Asia Pacific is expected to dominate the global market during the forecast period.

Silicon Carbide Coating Market: Dynamics

Key Growth Drivers:

- Superior Material Properties of Silicon Carbide: Silicon carbide coatings offer high hardness, excellent thermal conductivity, corrosion resistance, and superior wear resistance, making them ideal for demanding industrial applications.

- Rising Demand from the Semiconductor Industry: The growth of the semiconductor sector—especially with the expansion of 5G, electric vehicles, and power electronics—is fueling demand for high-purity and thermally stable coatings like silicon carbide.

- Increasing Adoption in Aerospace and Defense: The aerospace industry increasingly relies on silicon carbide coatings for their high-temperature stability and durability, especially in engine components and heat shields.

- Growing Popularity in Energy and Power Generation: Silicon carbide coatings are being used in nuclear and conventional power plants due to their resistance to radiation and extreme environments, promoting their adoption in this sector.

- Environmental Regulations Promoting Durable Coatings: Stringent environmental and safety regulations are pushing industries toward longer-lasting and environmentally friendly coating solutions, boosting demand for silicon carbide coatings.

Restraints:

- High Cost of Production and Raw Materials: The manufacturing of silicon carbide coatings involves complex processes and expensive raw materials, which increases the overall cost and limits adoption in cost-sensitive applications.

- Technical Complexity in Application: Applying silicon carbide coatings requires specialized equipment and expertise, making it challenging for smaller manufacturers or industries with limited technical capabilities.

- Limited Availability of Skilled Workforce: A shortage of skilled professionals with experience in handling and applying advanced coatings can slow down market penetration, especially in emerging regions.

Opportunities:

- Emerging Applications in Electric Vehicles (EVs): As EV adoption grows, so does the demand for thermally stable, corrosion-resistant coatings in battery systems and power electronics, creating new opportunities for silicon carbide coatings.

- Advancements in Coating Technologies: Innovations in chemical vapor deposition (CVD), physical vapor deposition (PVD), and other coating technologies are making silicon carbide coatings more efficient and cost-effective.

- Expansion into Developing Markets: Rapid industrialization and infrastructure development in Asia-Pacific, Latin America, and the Middle East offer untapped growth potential for the market.

- Integration with Additive Manufacturing: Combining silicon carbide coatings with 3D-printed parts can unlock novel engineering applications, especially in aerospace, automotive, and medical sectors.

Challenges:

- Intense Market Competition from Alternative Coatings: Competing coating materials such as tungsten carbide, alumina, and diamond-like carbon (DLC) offer similar benefits at lower costs, challenging silicon carbide's market share.

- Environmental and Safety Concerns in Manufacturing: Handling silicon carbide powders and chemicals during the coating process requires strict safety protocols and can raise regulatory hurdles in certain regions.

- Economic Slowdowns Affecting Capital-Intensive Industries: Fluctuations in the global economy can reduce investments in key end-use sectors like aerospace and semiconductors, indirectly impacting demand for silicon carbide coatings.

- Difficulty in Achieving Uniform Coating on Complex Surfaces: Achieving consistent silicon carbide coating thickness and adherence on geometrically complex parts remains a technical barrier in high-precision industries.

Silicon Carbide Coating Market: Report Scope

This report thoroughly analyzes the Silicon Carbide Coating Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Silicon Carbide Coating Market |

| Market Size in 2023 | USD 650.67 Million |

| Market Forecast in 2032 | USD 1344.7 Million |

| Growth Rate | CAGR of 8.4% |

| Number of Pages | 174 |

| Key Companies Covered | Fiven, Xycarb Ceramics, CoorsTek, SGL Group, Mersen Group, Nevada Thermal Spray Technologies, Seram Coatings, Toyo Tanso, Nippon Carbon, Morgan Advanced Materials, Bay Carbon, Silicon Valley Microelectronics, Aperture Optical Sciences, OptoSiC, Nanoshel LLC |

| Segments Covered | By Product Type, By Application, By End-User, By Functionality, By Form, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Silicon Carbide Coating Market: Segmentation Insights

The global silicon carbide coating market is divided by product type, application, end-user, functionality, form, and region.

Segmentation Insights by Product Type

Based on product type, the global silicon carbide coating market is divided into single crystal silicon carbide, polycrystalline silicon carbide, and amorphous silicon carbide.

In the silicon carbide coating market, polycrystalline silicon carbide is the most dominant product type segment. This dominance is primarily due to its excellent combination of thermal stability, mechanical strength, and cost-effectiveness. Polycrystalline silicon carbide is widely used in industrial applications such as aerospace components, nuclear reactors, and chemical processing equipment, where durability and high-temperature resistance are critical. Its microstructure, composed of multiple small crystals, offers robustness and wear resistance, making it suitable for a wide range of harsh operating environments.

Following polycrystalline, the single crystal silicon carbide segment holds a significant but smaller share. Single crystal silicon carbide, often referred to as SiC substrates, is especially valued in electronics and semiconductor industries for its superior electrical properties and high thermal conductivity. It is commonly used in power electronics, optoelectronics, and high-frequency devices. However, its high manufacturing cost and technical complexity limit its broader adoption compared to polycrystalline types, thus contributing to its smaller market share.

The amorphous silicon carbide segment is the least dominant among the three. While it has unique benefits such as corrosion resistance and ease of deposition in thin-film applications, it lacks the structural strength and high-temperature capabilities of the crystalline forms. Amorphous silicon carbide is typically used in specific applications such as protective coatings, MEMS devices, and biomedical implants. However, its niche use cases and lower mechanical performance restrict its dominance in the overall silicon carbide coating market.

Segmentation Insights by Application

On the basis of application, the global silicon carbide coating market is bifurcated into aerospace, automotive, electronics & semiconductors, defense, and industrial machinery.

In the silicon carbide coating market, the aerospace segment stands as the most dominant application area. This dominance is driven by the industry's demand for lightweight, durable, and heat-resistant materials. Silicon carbide coatings are extensively used in turbine engines, spacecraft, and high-temperature structural components due to their exceptional thermal stability, corrosion resistance, and ability to withstand extreme environments. The stringent performance requirements in aerospace applications strongly favor the adoption of advanced materials like silicon carbide.

The automotive sector follows closely, leveraging silicon carbide coatings for improving engine components, exhaust systems, and electric vehicle powertrains. As the industry shifts toward electric and hybrid vehicles, the need for thermal management and high-performance materials increases, boosting the use of SiC coatings. These coatings contribute to enhancing fuel efficiency, reducing emissions, and extending component lifespan, making them valuable for modern automotive engineering.

Next in line is the electronics & semiconductors segment, where silicon carbide coatings are used for protective layers in devices that operate under high voltage, high frequency, and high temperature. With the growing demand for energy-efficient and compact electronic components, SiC's superior electrical and thermal properties make it ideal for substrates and insulative coatings. However, the high cost of processing and material limitations confine its use to specific high-performance devices, limiting its overall market share.

The defense segment utilizes silicon carbide coatings in applications requiring ballistic protection, thermal shielding, and structural reinforcement. Although this market benefits from steady government funding and R&D, its scale is smaller compared to aerospace and automotive. Still, the defense sector values SiC coatings for their ability to enhance the durability and functionality of critical equipment.

The industrial machinery segment is the least dominant in the silicon carbide coating market. While SiC coatings are applied to improve wear and corrosion resistance in pumps, valves, and cutting tools, the cost sensitivity and less demanding performance requirements in general industrial applications make cheaper alternatives more appealing. Consequently, silicon carbide coatings are primarily reserved for high-end or specialized equipment in this sector.

Segmentation Insights by End-User

Based on end-user, the global silicon carbide coating market is divided into mining & metallurgy, pulp & paper, oil & gas, energy, and healthcare & medical devices.

In the silicon carbide coating market, the mining & metallurgy sector is the most dominant end-user segment. This is due to the extreme operating conditions inherent in these industries, including high temperatures, abrasive materials, and corrosive environments. Silicon carbide coatings offer excellent hardness, thermal stability, and chemical resistance, making them ideal for protecting equipment such as smelting components, heat exchangers, and processing machinery. Their use significantly improves equipment lifespan and reduces maintenance costs, driving strong demand in this sector.

The oil & gas industry is the next major end-user, relying on silicon carbide coatings to protect components exposed to harsh conditions such as downhole drilling, fluid handling, and chemical processing. These coatings enhance the performance of valves, pumps, and seals, especially in environments involving high pressures, temperatures, and corrosive substances. The need for operational reliability and reduced downtime makes SiC coatings valuable in this capital-intensive industry.

Following oil & gas, the energy sector—particularly renewable and nuclear energy—utilizes silicon carbide coatings in systems that demand high efficiency and resistance to heat and wear. Applications include protective layers on solar panels, fuel cells, and components in nuclear reactors. While growing in significance, the adoption of SiC coatings in this sector is still maturing, and thus its overall market share is smaller compared to mining and oil & gas.

The pulp & paper industry also uses silicon carbide coatings, but on a more limited scale. Coatings are applied to enhance the wear resistance and longevity of rollers, blades, and other components exposed to chemical and mechanical wear. While the industry benefits from such protective measures, the lower operating temperatures and less aggressive environments compared to other sectors reduce the urgency for advanced coatings, leading to moderate market penetration.

Lastly, the healthcare & medical devices segment is the least dominant. Silicon carbide coatings are used in specialized medical tools and implants due to their biocompatibility, hardness, and corrosion resistance. However, the volume of use is relatively low, and stringent regulatory requirements and high production costs restrict broader application. This keeps the healthcare segment a niche but promising area for SiC coatings in the long term.

Segmentation Insights by Functionality

On the basis of functionality, the global silicon carbide coating market is bifurcated into corrosion resistance, thermal barrier, abrasion resistance, electrical conductivity, and wear resistance.

In the silicon carbide coating market, corrosion resistance is the most dominant functionality segment. Silicon carbide’s exceptional chemical inertness makes it a preferred choice for applications in highly corrosive environments, such as those found in chemical processing, mining, and oil & gas industries. Its ability to form a protective layer that resists degradation from acids, alkalis, and other harsh chemicals drives its widespread use across several end-use sectors where equipment longevity and reduced maintenance are critical.

Following this, thermal barrier functionality holds a prominent position. Silicon carbide coatings are highly effective at withstanding extreme temperatures, making them ideal for aerospace, energy, and automotive applications. These coatings protect structural and engine components from thermal fatigue and heat damage, improving efficiency and reliability in high-temperature environments. The growing adoption of high-performance engines and energy systems continues to push the demand for SiC-based thermal barrier coatings.

Abrasion resistance is another significant functionality, especially in industries where mechanical wear is a major concern. Silicon carbide coatings are extremely hard and durable, providing superior protection to components subjected to repeated friction and impact. This makes them suitable for parts in industrial machinery, pulp & paper, and mining applications, where equipment is regularly exposed to harsh operating conditions.

Wear resistance, closely related to abrasion resistance, also plays an important role. While abrasion resistance deals with surface degradation due to friction, wear resistance encompasses a broader scope of material loss from mechanical action. SiC coatings extend the operational life of components like bearings, shafts, and valves, particularly in high-load or high-cycle applications. However, its overlap with abrasion resistance slightly reduces its standalone market visibility.

Lastly, electrical conductivity is the least dominant functionality in the market. While silicon carbide possesses semiconductor properties and can be used for conductive coatings in electronics and power devices, this use is specialized and limited compared to other functional benefits. Its applications are mostly confined to niche areas like power modules, sensors, and high-frequency devices, restricting its overall contribution to the broader SiC coating market.

Segmentation Insights by Form

On the basis of form, the global silicon carbide coating market is bifurcated into powder coating, liquid coating, paste coating, film coating, and composite coating.

In the silicon carbide coating market, powder coating is the most dominant form. Powder coatings offer excellent adhesion, uniform thickness, and durability, making them ideal for high-performance applications in industries such as aerospace, automotive, and heavy machinery. Their ability to form dense, wear- and corrosion-resistant layers on complex surfaces contributes significantly to their widespread use. Additionally, powder coatings are environmentally friendly due to the absence of solvents, further enhancing their appeal across various industrial sectors.

Liquid coating follows as a strong contender. Liquid silicon carbide coatings are easier to apply in certain manufacturing setups and offer versatility in terms of thickness and surface finish. They are widely used in sectors where precise control of coating characteristics is needed, such as in electronics and chemical processing equipment. However, the presence of solvents and longer curing times can pose environmental and efficiency concerns, which slightly hinder their dominance compared to powder forms.

Film coating ranks next in popularity. Thin-film SiC coatings are especially valued in semiconductor, optics, and MEMS (Micro-Electro-Mechanical Systems) applications due to their ability to provide surface protection without significantly altering the substrate’s physical properties. Although highly specialized and precise, the limited scope of applications and high processing costs restrict their widespread use.

Composite coating is an emerging segment, gaining traction for combining the benefits of silicon carbide with other materials (such as metals or polymers) to enhance multifunctionality. These coatings are increasingly used in advanced engineering applications that demand hybrid properties like improved thermal conductivity along with wear or corrosion resistance. While promising, composite coatings are still under development for broader industrial use, which places them behind more established forms.

Paste coating is the least dominant form in the market. It is primarily used for small-scale or custom applications where high-precision deposition isn’t required. Paste coatings are suitable for touch-up work, small components, or as part of layered manufacturing processes. However, limitations in uniformity, durability, and scalability make this form less favorable for large-scale industrial deployment.

Silicon Carbide Coating Market: Regional Insights

- Asia Pacific is expected to dominates the global market

Asia Pacific is the most dominant region in the global silicon carbide coating market. This dominance is primarily driven by the strong presence of the electronics, automotive, and semiconductor industries in countries such as China, Japan, South Korea, and Taiwan. The region benefits from large-scale production facilities, high demand for electric vehicles, and increasing investments in renewable energy infrastructure. Government support for industrial innovation and local manufacturing has further accelerated the adoption of advanced materials like silicon carbide coatings, particularly in applications requiring high thermal resistance and mechanical durability.

North America ranks as the second most dominant region, supported by advanced aerospace, defense, and energy sectors. The United States, in particular, plays a key role in driving demand for silicon carbide coatings used in jet engines, gas turbines, and power electronics. The rise of electric mobility, coupled with increasing focus on high-performance, energy-efficient technologies, has boosted the region’s interest in SiC coatings. Additionally, ongoing research and innovation from both industry and academia contribute to the region’s technological edge.

Europe follows closely, driven by a strong emphasis on sustainable development and stringent industrial standards. Countries like Germany, France, and the UK lead in the use of silicon carbide coatings across automotive, energy, and aerospace sectors. The region’s well-developed infrastructure and dedication to clean energy and lightweight material technologies fuel the integration of SiC coatings in high-performance systems. Collaborations between research institutions and manufacturers further enhance product development and application diversity.

Middle East and Africa (MEA) show moderate growth potential in the silicon carbide coating market. Demand in this region is primarily influenced by the oil & gas, energy, and industrial processing sectors. Countries such as Saudi Arabia and the UAE are adopting SiC coatings for use in extreme-temperature environments where wear and corrosion resistance are critical. Although the region lags behind in overall industrial adoption compared to others, strategic investments in infrastructure modernization and technology are gradually expanding market opportunities.

Latin America is the least dominant region in the global silicon carbide coating market. The market here is relatively underdeveloped due to limited industrial capacity and lower investments in high-performance materials. However, countries like Brazil and Mexico show some demand, mainly in the automotive, metal processing, and energy industries. Economic challenges and slower technological adoption have restricted growth, but there is potential for gradual progress as regional industries seek to modernize operations and improve efficiency.

Silicon Carbide Coating Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the silicon carbide coating market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global silicon carbide coating market include:

- Fiven

- Xycarb Ceramics

- CoorsTek

- SGL Group

- Mersen Group

- Nevada Thermal Spray Technologies

- Seram Coatings

- Toyo Tanso

- Nippon Carbon

- Morgan Advanced Materials

- Bay Carbon

- Silicon Valley Microelectronics

- Aperture Optical Sciences

- OptoSiC

- Nanoshel LLC

The global silicon carbide coating market is segmented as follows:

By Product Type

- Single Crystal Silicon Carbide

- Polycrystalline Silicon Carbide

- Amorphous Silicon Carbide

By Application

- Aerospace

- Automotive

- Electronics and Semiconductors

- Defense

- Industrial Machinery

By End-User

- Mining and Metallurgy

- Pulp and Paper

- Oil and Gas

- Energy

- Healthcare and Medical Devices

By Functionality

- Corrosion Resistance

- Thermal Barrier

- Abrasion Resistance

- Electrical Conductivity

- Wear Resistance

By Form

- Powder Coating

- Liquid Coating

- Paste Coating

- Film Coating

- Composite Coating

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Silicon Carbide Coating

Request Sample

Silicon Carbide Coating