Smart Meter Wireless Module Market Size, Share, and Trends Analysis Report

CAGR :

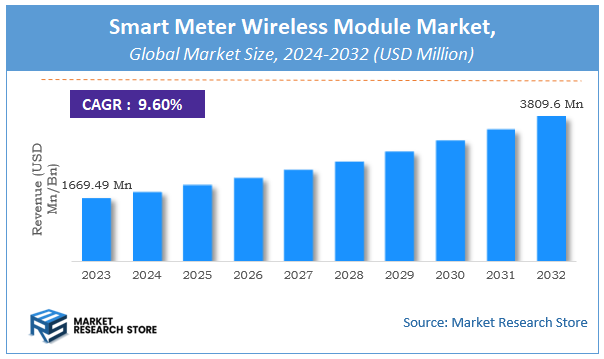

| Market Size 2023 (Base Year) | USD 1669.49 Million |

| Market Size 2032 (Forecast Year) | USD 3809.6 Million |

| CAGR | 9.6% |

| Forecast Period | 2024 - 2032 |

| Historical Period | 2018 - 2023 |

Smart Meter Wireless Module Market Insights

According to Market Research Store, the global smart meter wireless module market size was valued at around USD 1669.49 million in 2023 and is estimated to reach USD 3809.6 million by 2032, to register a CAGR of approximately 9.6% in terms of revenue during the forecast period 2024-2032.

The smart meter wireless module report provides a comprehensive analysis of the market, including its size, share, growth trends, revenue details, and other crucial information regarding the target market. It also covers the drivers, restraints, opportunities, and challenges till 2032.

To Get more Insights, Request a Free Sample

Global Smart Meter Wireless Module Market: Overview

A Smart Meter Wireless Module is a communication component integrated into smart meters that enables real-time wireless transmission of energy usage data to utilities and consumers. These modules typically use wireless communication technologies such as RF (radio frequency), Zigbee, Wi-Fi, or cellular networks (like NB-IoT or LTE-M) to facilitate two-way communication between the smart meter and the utility's central system. This allows for accurate and timely monitoring, remote meter reading, outage detection, and dynamic pricing, enhancing the overall efficiency of energy management and distribution systems.

Key Highlights

- The smart meter wireless module market is anticipated to grow at a CAGR of 9.6% during the forecast period.

- The global smart meter wireless module market was estimated to be worth approximately USD 1669.49 million in 2023 and is projected to reach a value of USD 3809.6 million by 2032.

- The growth of the smart meter wireless module market is being driven by increasing global demand for smart grid infrastructure and the transition toward digital energy management.

- Based on the component, the Communication Modules segment is growing at a high rate and is projected to dominate the market.

- On the basis of communication technology, the Cellular segment is projected to swipe the largest market share.

- In terms of application, the Utility segment is expected to dominate the market.

- Based on the end-user, the Energy Providers segment is expected to dominate the market.

- By region, North America is expected to dominate the global market during the forecast period.

Smart Meter Wireless Module Market: Dynamics

Key Growth Drivers:

- Government Smart Grid Initiatives: Numerous national programs and regulations are promoting the adoption of smart meters to improve energy efficiency, grid reliability, and data transparency. These initiatives are creating strong demand for wireless modules to support two-way communication.

- Rising Energy Consumption & Urbanization: Increasing energy demands in both developed and developing regions are pushing utilities to deploy smarter infrastructure, including wireless modules that enable real-time data monitoring and load management.

- Advancements in Wireless Communication Technologies: The evolution of wireless technologies such as NB-IoT, LoRaWAN, and 5G is enhancing the performance, range, and power efficiency of smart meter modules, encouraging broader adoption.

Restraints:

- High Initial Investment Costs: The upfront cost of deploying smart meters equipped with wireless modules can be high, especially for utilities in emerging economies, hindering large-scale rollouts.

- Data Privacy and Cybersecurity Concerns: As wireless modules transmit sensitive user data, concerns over data breaches and cyber threats act as a restraint, requiring secure network architectures and compliance measures.

Opportunities:

- Integration with IoT and Smart Home Ecosystems: The growing trend of connected homes and the Internet of Things (IoT) offers significant opportunities for wireless modules to act as critical nodes in broader home energy management systems.

- Expansion in Emerging Markets: Countries in Asia-Pacific, Latin America, and Africa are investing in grid modernization and smart city projects, presenting untapped potential for wireless module vendors.

Challenges:

- Infrastructure and Technical Limitations in Rural Areas: In less developed or remote areas, the lack of robust communication infrastructure can limit the effectiveness and deployment of wireless modules.

- Interoperability and Standardization Issues: Varying communication standards and lack of universal protocols across regions and utilities can lead to integration challenges, slowing down widespread adoption.

Smart Meter Wireless Module Market: Report Scope

This report thoroughly analyzes the Smart Meter Wireless Module Market, exploring its historical trends, current state, and future projections. The market estimates presented result from a robust research methodology, incorporating primary research, secondary sources, and expert opinions. These estimates are influenced by the prevailing market dynamics as well as key economic, social, and political factors. Furthermore, the report considers the impact of regulations, government expenditures, and advancements in research and development on the market. Both positive and negative shifts are evaluated to ensure a comprehensive and accurate market outlook.

| Report Attributes | Report Details |

|---|---|

| Report Name | Smart Meter Wireless Module Market |

| Market Size in 2023 | USD 1669.49 Million |

| Market Forecast in 2032 | USD 3809.6 Million |

| Growth Rate | CAGR of 9.6% |

| Number of Pages | 175 |

| Key Companies Covered | Sierra Wireless, Gemalto (Thales Group), Quectel, Telit, Huawei, Sunsea Group, LG Innotek, U-blox, Fibocom wireless Inc., Neoway, Laird Connectivity, LoRa Alliance |

| Segments Covered | By Component, By Communication Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2023 |

| Historical Year | 2018 to 2023 |

| Forecast Year | 2024 to 2032 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. Request For Customization |

Smart Meter Wireless Module Market: Segmentation Insights

The global smart meter wireless module market is divided by component, communication technology, application, end-user, and region.

Based on component, the global smart meter wireless module market is divided into microcontrollers, RF modules, power management ICs, communication modules, and others. Communication Modules represent the most dominant segment. These modules are essential for enabling two-way data transmission between smart meters and utility providers. As the core component facilitating real-time communication via technologies such as RF, Zigbee, LoRa, NB-IoT, or LTE-M, their importance has grown alongside the expansion of smart grid projects and demand for remote monitoring and control. Utilities rely heavily on robust communication infrastructure to ensure accurate billing, timely outage detection, and improved load balancing, making this segment crucial in the wireless module ecosystem.

On the basis of communication technology, the global smart meter wireless module market is bifurcated into cellular, Wi-Fi, LoRa, zigbee, and bluetooth. The cellular technology stands out as the most dominant communication segment. Its ability to provide wide-area coverage, high data transmission rates, and real-time connectivity makes it ideal for smart metering applications, particularly in urban and suburban areas. Technologies such as NB-IoT and LTE-M are gaining momentum due to their low power consumption and strong signal penetration, enabling efficient remote monitoring and management of smart meters. Cellular networks are highly scalable and easily integrate with utility backend systems, making them the preferred choice for large-scale deployments.

Based on application, the global smart meter wireless module market is divided into residential, commercial, industrial, utility, and smart cities. Utility applications hold the dominant position. Utilities deploy wireless modules at scale to enable real-time data collection, remote meter reading, outage management, and accurate billing. These modules play a crucial role in modernizing grid infrastructure and optimizing energy distribution. Given the size and scope of utility networks, along with regulatory mandates for smart metering in many regions, this segment continues to drive the highest demand and investment.

In terms of end-user, the global smart meter wireless module market is bifurcated into energy providers, telecom operators, water supply companies, gas supply companies, and others. Energy Providers are the most dominant end-users. They are the primary drivers of smart metering initiatives, deploying wireless modules to improve grid management, ensure accurate billing, reduce losses, and enable demand-response strategies. As electricity remains the most widely consumed utility, energy providers lead in adopting wireless communication solutions to support real-time data transmission and infrastructure modernization across both residential and commercial sectors.

Smart Meter Wireless Module Market: Regional Insights

- North America is expected to dominates the global market

North America is the most dominant region in the smart meter wireless module market, driven by widespread deployment of smart grid infrastructure across the United States and Canada. The region has been at the forefront of adopting advanced metering solutions due to strong regulatory mandates, well-established utility networks, and significant investments in grid modernization. Utilities in this region are increasingly integrating wireless modules into electricity, gas, and water meters to optimize operations, reduce energy theft, and offer consumers better control over energy consumption. Additionally, the presence of key technology providers and government support for clean energy initiatives further bolster market growth in this region.

Europe follows North America in terms of market share, fueled by EU-wide directives for smart metering and a growing emphasis on sustainability and energy efficiency. Countries like the UK, Germany, France, and Italy have implemented large-scale smart meter rollout programs, creating strong demand for wireless communication modules. The market here is supported by a well-structured energy policy framework, technological advancement, and active participation of utilities in digitization. Integration of IoT and cloud-based platforms for energy monitoring and management is becoming more common, promoting the uptake of wireless modules in smart meters across both urban and rural settings.

Asia Pacific represents a rapidly growing market, propelled by urbanization, increasing energy demand, and strong government initiatives in countries such as China, India, Japan, and South Korea. Governments are focusing on reducing transmission losses and improving energy efficiency, prompting significant investments in smart grid projects. China leads the region with large-scale deployments and domestic manufacturing support, while India is emerging as a key player with government-led initiatives under programs like the Smart Meter National Programme (SMNP). The growing telecom infrastructure and digitalization are aiding wireless module adoption across utilities in this region.

Latin America is experiencing gradual growth in the smart meter wireless module market, with countries like Brazil, Mexico, and Argentina making steady progress toward modernizing their energy infrastructure. Though deployments are limited compared to developed regions, rising electricity demand, grid reliability concerns, and utility-led pilot programs are setting the foundation for future expansion. Economic challenges and regulatory uncertainties may slow the pace, but ongoing smart city projects and foreign investments are expected to improve adoption over time.

Middle East and Africa (MEA) represent the least dominant region in the market, but also hold untapped potential. Countries like the UAE, Saudi Arabia, and South Africa are beginning to adopt smart metering systems as part of broader energy diversification and digital transformation agendas. However, limited infrastructure, financial constraints, and slower regulatory alignment present challenges. Despite these hurdles, increasing energy needs, efforts to reduce losses, and regional modernization programs are expected to gradually support market development in the coming years.

Smart Meter Wireless Module Market: Competitive Landscape

The report provides an in-depth analysis of companies operating in the smart meter wireless module market, including their geographic presence, business strategies, product offerings, market share, and recent developments. This analysis helps to understand market competition.

Some of the major players in the global smart meter wireless module market include:

- Sierra Wireless

- Gemalto (Thales Group)

- Quectel

- Telit

- Huawei

- Sunsea Group

- LG Innotek

- U-blox

- Fibocom wireless Inc.

- Neoway

- Laird Connectivity

- LoRa Alliance

The global smart meter wireless module market is segmented as follows:

By Component

- Microcontrollers

- RF Modules

- Power Management ICs

- Communication Modules

- Others

By Communication Technology

- Cellular

- Wi-Fi

- LoRa

- Zigbee

- Bluetooth

By Application

- Residential

- Commercial

- Industrial

- Utility

- Smart Cities

By End-User

- Energy Providers

- Telecom Operators

- Water Supply Companies

- Gas Supply Companies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Rest of Latin America

- The Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East Africa

Frequently Asked Questions

Table Of Content

Inquiry For Buying

Smart Meter Wireless Module

Request Sample

Smart Meter Wireless Module